What if you prayed relentlessly – ‘God, please design the perfect money for us humans on Earth…’

The ‘perfect money’, you tell God, needs to have the following attributes:

- Durability: It should be chemically inert, hence almost indestructible – it should not rust, tarnish, or decay, so it can be passed on from generation to generation, for centuries, even millennia.

- Scarcity: It should be difficult to mine or produce, so it cannot be produced ad infinitum like paper money. The total amount of it should be permanently limited.

- Divisibility (via malleability): It should be able to be melted, divided into small units, and fashioned into coins or bars without loss of material value.

- Fungibility: In melted form, one ounce of it should be equivalent to any other ounce of it, ensuring consistent quality regardless of form.

- Portability: It should have a high value-to-weight ratio, allowing significant wealth to be stored in a small, easily transported form.

- Aesthetic value: It should be shiny so it can have ornamental value in crowns, necklaces, wedding bands and rings, watches, earrings, etc.

- Widespread utility: It should also have uses as an electricity conductor in modern industry – laptops, smartphones, GPS units, aviation, satellites, aerospace, spacecraft, jet engines – and in medicine and dentistry like diagnostic tools, fillings, and crowns. Further, it should be able to reflect heat so it can be used in the thin-film coating of glass in skyscrapers.

- Known to everyone: The result of this widespread utility and high-end use will make it known to everyone when humans start using it – from a ten-year-old child to Wall Street CEOs, from villagers in India to businessmen in Hong Kong, from Filipino maids to top actresses in Hollywood.

Oh, wait…God has answered your prayers already. Or you may prefer to say Mother Nature has, if you are not a theist. Gold has all those eight properties listed above. No wonder once gold became known, it has been in use for an estimated 5,000 years.

But is gold the ‘best sound money there is’?

Money is a unit of account, a store of value, and thus a medium of exchange.

Why do some things become money? Economist Ludwig von Mises was the first to deduce that before something becomes money spontaneously in society, it must already be in use and be regarded as valuable. Gold became money long before any kings or governments recognised it as such. In the free market, it easily beat other precious metals, seashells, copper, and bags of wheat or corn. It was crowned the ‘best money there is’ by the market, not by some bureaucrat.

The total supply of gold is limited. About 220,000 metric tonnes of gold have been mined, which leaves about 55,000, or 25 per cent of total supply in the Earth’s crust, available for further mining. But exploration has costs, as do refining and purifying. Remote mines of less pure gold do not become economic unless the price of gold in the currency in use rises substantially. This is why the almost-indestructible supply of gold does not rise too fast; it never has. That makes the best money ‘sound’ money as well.

During the century from 1814 to 1914, the UK was on a gold standard (the US on a bimetallic gold and silver standard till 1900). That means the supply of money by government was tied to the gold reserves it had. And, during this time, the purchasing power of the pound sterling and the US dollar stayed constant. A basket of goods in 1914 cost the same in commodity-backed currency as in 1814. This is despite huge shocks to the system like the American Civil War (1861-65). A hundred years of no inflation meant outstanding economic growth. It’s an inflationary economy that aids grifters and hustlers. For a little while, Australia, too, benefited from being on the gold standard (since we were using British currency), but we came off the gold standard in 1929.

How did inflation come to be regarded as a necessary evil? It’s the biggest scientific scam of all time, running for almost a hundred years now, eclipsing even the climate racket.

Only confused public servants or politicians who care naught for the people love inflation. It’s never announced as a tax, but a tax it nevertheless is. It surreptitiously hurts the middle-income and lower-income classes. The gold standard had disciplined governments into balancing their budgets or backing the debt with gold reserves. Without that backing, the state could spend merrily with fiat money, meaning money created at will, and deficits could be monetised for the inflation tax that was levied without Parliament’s knowledge, let alone oversight or approval. What fun.

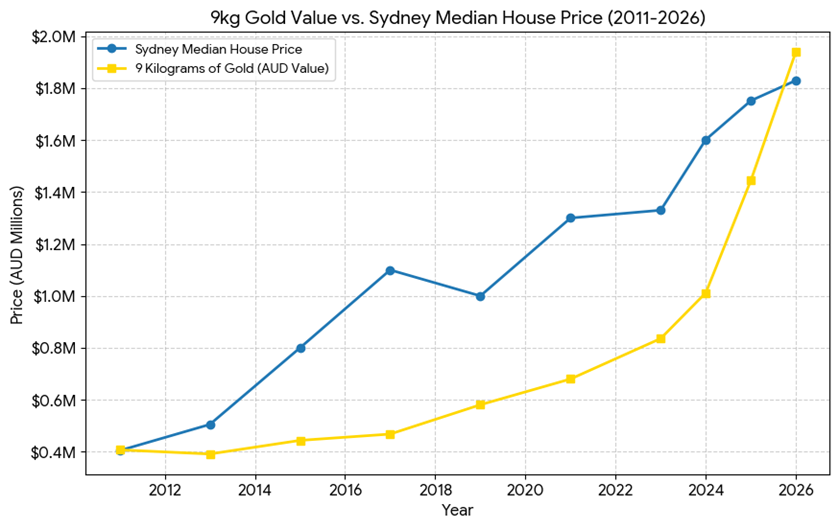

Here is a graph that may surprise you:

Graph provided by author.

Can we dare to ask, ‘Has the median house price in Sydney stayed the same over the last 15 years?’ It may be economic heresy to say so, but if gold was still the medium of exchange, house prices have stayed about the same.

The US Constitution

The US Constitution (ratified in 1789) denied the government the right to print money without a commodity backing. Article I, Section 10 of the US Constitution prohibited states from making anything but gold and silver coin a legal tender in payment of debts. However, during the Civil War, the US government issued ‘greenbacks’ – paper debts without the backing of gold or silver. In 1870, this action was regarded as unconstitutional. But in 1871, two cases (Knox v. Lee and Parker v. Davis), reversed the precedent and ruled that paper currency was legal tender – and fiat currency was born. In 1933, President Roosevelt ordered that citizens’ gold be confiscated at US$35 an ounce. In 1975, holding gold became legal again in the US, at which time the market was at US$185 an ounce! Until 1971, only other sovereign nations could (and did) demand gold at $35 an ounce by exchanging US sovereign bonds for gold, but by then fiat had hugely diluted the value of the currency, and President Nixon decided to close this gold window. 1971 was the nail in the coffin for gold, but fiat money had already ruled the world since 1929.

The (US) dollar originally meant 24.1 grams of pure silver. The pound also was, and still is, a unit of weight. But ‘pound sterling’ meant a pound of ‘sterling’, meaning 92.5 per cent pure silver. A foot is still 12 inches. And a metre is still 100 centimetres. These conversion metrics need to be permanent. But currencies are now so divorced from their original meaning, being fixed units of weight of a metal, that no one connects the two anymore. In 1900, the US Gold Standard Act made gold the exclusive monetary standard at US$20.67 per troy ounce. Today it’s 237 times that, like one metre getting redefined as 23,700 centimetres.

Is Bitcoin Digital Gold?

Bitcoin’s algorithm is undoubtedly a clever ruse at mimicking gold. It has outdone gold for the first five of those eight properties we noted above. The eighth is a function of the top seven, and Bitcoin’s labyrinthine complexity – a tortuous algorithm, desk warriors ‘mining’ while sitting at their desks, a thing that’s not a coin, not something you can feel, touch, or see, with massive swings in its purchasing ability – makes it a favourite pastime and investment among the alienated IT crowd that celebrates distrust. Not merely justifiable distrust of central banks controlling the money supply levers, but all distrust.

But one can’t have a civilisation if everyone distrusts everyone else. You can’t be your own doctor, plumber, farmer, carpenter, masseuse, and dentist. The modern economy thrives on specialisation and is intricately interconnected – perhaps 99 per cent of humanity didn’t know where the Strait of Hormuz was until a few weeks ago, but now 99 per cent do.

Bitcoin fails the aesthetic test (number six), but, for a few, mathematics has an innate beauty. To some eyes, Satoshi Nakamoto’s Bitcoin algorithm is a Picasso or a Rembrandt. Isaac Newton may agree, but an illiterate granny in Africa who proudly bequeaths her jewellery to her daughter will shake her head. A genuine medium of exchange needs to be understood by everyone, like dollars are today. Only then can it be used to pay billions for a corporate takeover, a few hundred for a TV at Harvey Norman, or as a fiver to a barista for a shot of caffeine.

But Bitcoin’s biggest shortcoming is not property eight, it is number seven. Seven is the raison d’être of all good money. It’s the reason why, when rapacious investment banks short gold in the hope of creating a panic, they do not succeed. How come? Well, there are buyers of gold waiting. Jewellers make up 46 per cent of all demand, and bullion makers make up another 23 per cent. They are only too happy to build up their inventory, if gold drops a lot relative to the US dollar. And, of course, the rest of the demand comes from all those industrial uses and central banks, who, too, are happy to buy low and arrest the fall.

But Bitcoin? Without a use, a utility, it’s just a greater-fool mechanism. In contrast to gold, most of Bitcoin’s sundry buyers are in it only for a speculative gain – not for them the virtue of setting a new monetary standard, not for them the value of a gold necklace, not for them the beauty of mathematics encrypted in software.

If Bitcoin begins to worry the central banks and governments, they may seek to deter its customers by undoing its anonymity, creating a panic by shorting the asset, or publicly declaring it the abode of criminals. Without a prior utility, Bitcoin is not money – it fails Mises’s money test. And that’s why the shorts may succeed. A panic sets in, and the price keeps falling; Bitcoin’s floor is a zero price. Then the central banks not only make money from the shorts but kill off this valueless upstart who dared to dream of replacing fiat currencies one day.

Other Cryptocurrencies

Bitcoin faces competition from several other cryptocurrencies, too – there are now 11,000 of them! Some, but not all, also have a maximum limit on their output. Bitcoin’s is 21 million coins of which just over 20 million have been ‘mined’ by ‘Keynesian’ work.

What’s Keynesian work? Get a hundred people to dig a large hole for 50 hours a week. Pay them $100 an hour. Then, in the second week, pay them all the same rate for another 50 hours to fill up the hole. GDP is up by $1 million.

But what real work has been done? What value has been added?

The answer: Nil. Nada. Zip. It’s just ‘Keynesian work’. Bitcoin’s miners solve cryptographic puzzles and consume electricity when they are ‘mining’. They are rewarded with Bitcoins.

Dear reader, you can solve crosswords, too, but don’t charge me for your intellectual stimulation.

Most cryptos are like hot-air balloons: the promoters make a buck – they sell when the balloon is high, but you and I can get caught in the inevitable crash. But all cryptos (save those mimicking an existing fiat currency) fail comprehensively at properties six to eight. Especially at the critical seven – they have no fundamental value, all buying is being done in the hope of a greater fool in the future.

My contention must be clear now: Gold is God’s money, Bitcoin is fool’s gold.

Digital Gold

It’s possible to trade with gold in minute quantities when you have bank accounts in milligrams of gold (1 milligram of gold today is worth 21 Australian cents). There are also gold products like Tether Gold and Pax Gold which set gold accounts on a blockchain – Bitcoin’s supposed nirvana of all things anti-government. Perth Mint is a private organisation, and its receipts are trusted worldwide for integrity in bullion quality and safe storage. All these allow you to ‘digitise’ gold and make it fast, highly divisible, and easy to transfer if that’s your preference.

The vast majority of merchants worldwide do not accept Bitcoin per se, so Bitcoin users lose plenty of fees in getting their Bitcoin changed into dollars or euros at the point of payment. Some other cryptos are reportedly faster and cheaper. Meanwhile, new payment systems for fiat currencies, like Venmo, are offering mostly fee-free transactions.

Visa, Mastercard, PayPal, and banks have centralised ledgers with multiple firewalls that elicit easier insurance protection from hacking. However, one-third of all Bitcoin exchanges may have been hacked into, making insurers wary.

Credit card transactions occur at the rate of over 25,000 per second worldwide – not something Bitcoin’s decentralised ledger can ever do. In comparison, one Bitcoin transfer takes 10 minutes or more in the ‘decentralised’ ledgers.

Financial technology for fiat currencies keeps getting better. A new upstart finds it impossible to displace the established currency (known as the network effect) unless that currency suffers hyperinflation, and then, any replacement will do.

Can Australia Get Back on the Gold Standard?

The trick is to use the best of this financial technology, currently wedded only to dollars and such, while switching to sound money. Which means getting the Australian dollar back on a sound footing. Politically, it requires three steps:

- Continuously produce federal budget surpluses till all sovereign debt (bar cash and coin) is retired; thereafter produce only surpluses, which can never be used except in case of defensive war. Abolish the existence of monetary and fiscal policy and outlaw budget deficits via a constitutional amendment – Parliament is summarily dissolved if there is a deficit.

- Treat banks as corporations, making banks subject to the same insolvency standards and laws as all other corporations are. This will make banks wary of having large at-call balances not matched by enough highly liquid assets. Banks may need to issue a lot more equity and have long-term bonds listed on a stock exchange. Instead of at-call bank savings accounts, some customers would prefer higher-interest, tradeable bank bonds.

- Have the demand for cash balances met by gold-backed cash notes issued by the RBA (the function could later be transferred to a private entity like the Perth Mint). Bank transfers would not be gold backed unless a bank chose to be that way. The RBA already stores $17 billion worth of gold at the Bank of England. Circulating cash and notes, which are a federal liability, are around $100 billion today. The gap of $83 billion is not insurmountable given the amount of gold traded every year worldwide.

Politically, these three steps are not an easy hill to climb on a quiet afternoon. They’re rugged mountains, and it will require a tough trek over many a day.

But the avid Bitcoin dream – inciting a society, ignorant of the fiat-money racket, to spontaneously evolve a new money, specifically Bitcoin (overcoming the vast network effect) – is far more improbable – think Mount Everest with a half-depleted oxygen tank. Good luck.