Increased government spending on infrastructure has been proposed yet again to revive the economy from the government-imposed recession. The latest call for the states to spend another $40 billion has come from Reserve Bank Governor Philip Lowe and is supported by Prime Minister Scott Morrison.

However, there are good reasons to be sceptical about the macroeconomic benefits of ramping up government spending on infrastructure on this scale, especially if it has not been subjected to rigorous cost-benefit analysis on a project-by-project basis.

The key rationale for advocating more infrastructure spending is that it will create jobs and hence reduce the unacceptably high level of unemployment; an unquestionably worthy ideal.

But economic recovery and unemployment reduction will depend on a revival of private sector activity, not government spending; because the private sector — services industries especially — has overwhelmingly borne the brunt of the economic impact of the COVID19 crisis (the CVC).

Productive public infrastructure no doubt plays a pivotal role in the economy because it influences both aggregate demand and supply, increasing demand through investment while adding to capacity via a larger capital stock.

Yet increasing infrastructure spending without regard to its productivity is growth-limiting if it manifests as ‘roads and bridges to nowhere’ that fail on cost-benefit grounds.

Japan provides a case study on how over-reliance on infrastructure spending funded by world-beating gross public debt around 250 per cent of its GDP, rather than undertaking worthy fiscal consolidation, including tax reform, as well as domestic structural reform, retards economic growth.

Spending big on infrastructure to create employment is a straight replay of Keynes’ 1930s advocacy of increased spending on ‘public works’ during the Great Depression. But the industrial structure of advanced economies and their workforces have greatly changed since then.

Today’s labour force is more specialized than the workforce of the 1930s would have been. Back then, labour was more homogenous and hence more substitutable across industries. It would have been easier for displaced farm or factory workers, for instance, to be re-deployed to other manual work on labour-intensive projects — and there was greater incentive to do so as there was no equivalent to today’s JobSeeker.

In contrast, the Australian economy — like all advanced economies — is now far more services-oriented; and currently-unemployed baristas or beauticians, for instance, are unlikely to be keen to switch (nor need they) to now more capital- intensive projects with their shovels at the ready.

Unproductive construction spending on projects in the non-tradable sector of the economy would also draw capital and labour away from tradable industries, worsening the economy’s international competitiveness.

Infrastructure spending cannot be readily deployed. Inevitable lags occur, given delays in choosing the most viable projects, combining production inputs and gaining the necessary planning approvals. Once projects are completed, where do workers go next? What jobs, for instance, did GFC pink batt installers find after that program finished?

Standard textbook theory, backed by empirical evidence, also tells us that in an open economy increasing direct government spending to ‘stimulate’ demand proves counterproductive as a means of increasing national income and employment.

This is because higher budget deficits at federal and state level induce capital inflow, drive up the exchange rate, as we have seen since March, and hence will subsequently crowd out net exports. This occurred following the ill-advised fiscal response to the GFC when the dollar reached $US1.10 — crippling manufacturing.

Other things being equal, large budget deficits also imply a return to ‘bad’ current account deficits, consistent with the ‘twin deficits’ hypothesis.

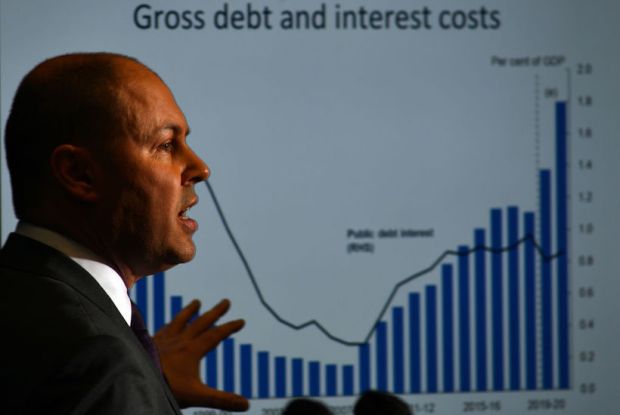

Government debt will continue to escalate in the absence of substantial budget repair on track to exceed $1 trillion in a few years.

If public debt reflects funding of productive public investment in infrastructure and human capital, it can enhance economic growth. However, the global fiscal response to the CVC was overwhelmingly unproductive as it has not been matched by new assets on the government balance sheet.

In the case of the $750 (times two) cash splash bonuses, the federal government literally borrowed from abroad to fund household consumption.

It is true that interest rate payable on public debt to fund new infrastructure are at rock bottom, but given the massive surge in public and private sector borrowing globally, they must surely rise in coming years when the ballooning public debt has to be refinanced.

Credit rating downgrades at either federal or state levels, or both, would further push up interest rates on foreign public debt, and cannot be ruled out in coming years.

Continuing to ramp up ‘stimulus’ elements in any future fiscal packages to encourage aggregate demand will worsen federal and state budget deficits. This runs the risk of severely hampering future economic performance due to further real exchange rate appreciation.

There will also be a significant drain on national income due to public debt interest paid abroad; likely to easily exceed $15 billion per annum in coming years and continuing to grow.

As a corollary, when budget deficits are wound back via cuts to unproductive spending, business confidence should improve, which in turn bolsters private investment and productivity.

Instead of focusing on government spending to boost aggregate demand, structural reform measures aimed at the supply side of the economy would be more effective in hastening economic recovery. This should most notably target deregulation of business red and green tape, industrial relations reform, lower company tax and/or increased investment allowances.

Tony Makin is professor of economics at Griffith University, a former IMF economist, and an author of the Centre for Independent Studies papers Lower Company Tax to Resuscitate the Economy and A Fiscal Vaccine for COVID-19, and the book, The Limits of Fiscal Policy.