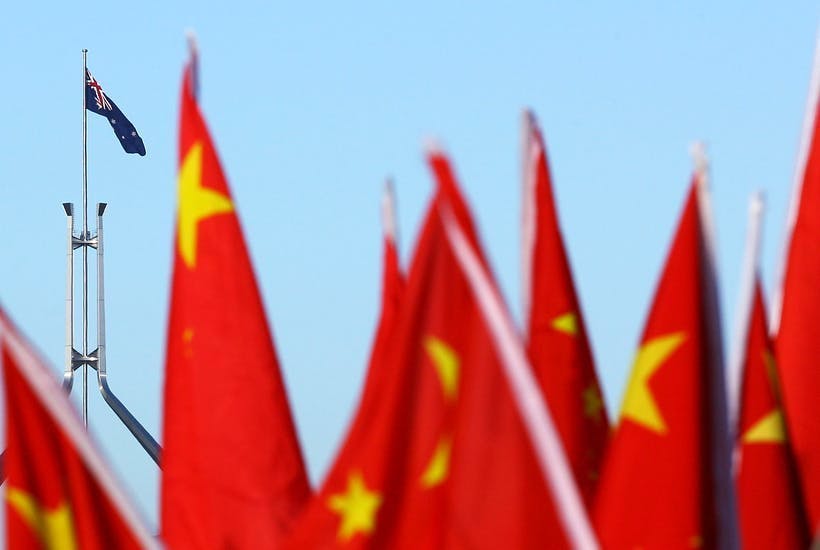

The events might come from a Hollywood script. School bully (China), annoyed over being left out of games (lucrative overseas contracts) and about comments passed in the schoolyard, decides to make an example of the weedy kid in the corner (Australia) in front of the other schoolkids.

But after flailing the weedy kid with trade restrictions the gigantic bully unexpectedly reels back with a bloody nose.

Meanwhile, the other kids in the schoolyard (the rest of the world) who have previously paid little attention to the weedy kid as a remote, uninteresting teacher’s pet with few internal problems, express quiet sympathy for Australia.

The schoolyard scrap continues, and Chinese trade restriction blows have caused painful dislocation in sectors such as thermal coal, beef, wine and lobster fishing. But after decades of economic reform emphasising free markets combined with immense resources wealth, the weedy kid’s economy has proved strong enough to absorb these blows, and even have them rebound on the attacker.

In this, the weedy kid has received unlooked-for help from strong markets in iron ore, gold, copper and wheat, with wheat prices being aided by Russia’s efforts to fight domestic inflation. Coronavirus, the pandemic which China unleashed, has also proved an ally in disrupting major suppliers in those areas.

As has been widely discussed, China decided to make an example of Australia, in front of the rest of the school for a host of offences. These include the Morrison government pushing for an independent inquiry into the origins of the Coronavirus, as well as raising concerns about the future of Hong Kong and Chinese intentions in the South China sea. The federal government has also passed legislation giving it the power to reverse deals made between the Chinese government and state governments and local bodies, with the chief target being Victoria’s decision to sign up to Beijing’s much-vaunted Belt and Road initiative.

In addition, Chinese government organisations are being blocked from investing in any area where there may be security concerns. In mid-January, in one of a long list of exclusions, Federal Treasurer Josh Frydenberg blocked a $300 million takeover of building contractor Probuild by China State Construction Engineering Corporation. CSCEC is owned by the Chinese state and Probuild has been involved in contracts such as building the Victorian police headquarters and the Melbourne offices of biotech company CSL, which is producing Covid-19 vaccines.

In making such rulings, the federal government is following the lead of the US, UK and Canada, to name a few, but faced with such evident distrust the bully needed to make an example of somebody. The resulting campaign of blocking certain imported commodities on various pretexts –- claiming that timber from Queensland is infested, that Australian wine is being dumped on Chinese markets (although it is mostly at the premium end of the market) and so on –- all while blaming Australia for making such a fuss –- is unprecedented. But Chinese market power has limits.

One telling omission from the list of commodities being blocked is iron ore, a market in which Australia accounts for 53 per cent of all international trade and where other suppliers have been dogged by misfortune. Big producer Vale in Brazil has not recovered from a mine disaster in early 2019 and has been affected by absenteeism due to the Coronavirus pandemic.

Tough border restrictions in Western Australia, which produces most of Australia’s iron ore, have badly knocked around its tourism industry. But the restrictions also mean the state’s production of iron ore and gold –- which has also been doing well -– has been untouched by the Covid epidemic. As the Chinese steel industry imports 63 per cent of all sea trade in iron ore, it has little choice but to deal with Australia, at a price. Industry disruptions have resulted in iron ore prices spiking from around $US80 a tonne early in 2020 to $US160 a tonne by the end of the year.

Faced with that enormous increase, in late December the China Iron and Steel Association declared that the “iron ore pricing mechanism had failed” and it would crack down on possible, but unspecified, violation of laws and regulations. But CISA stopped short of imposing any sales restrictions on Australian iron ore.

The resulting revenue windfall is expected to do wonders for a federal budget ravaged by efforts to keep businesses afloat during the Covid pandemic.

Australia also dominates the market for metallurgical or coking coal, another major ingredient in steel production. China can get some of that coal from other sources including its own mines and adjacent Mongolia, but much of its smelting equipment is designed specifically to use the higher quality Australia coal. Thermal coal for electricity production can also be found elsewhere but China uses so much of the stuff (all while being praised by green activists) that, to judge from media stories, ordinary Chinese have been made to do without heating in winter and forced to walk many flights of steps at work as there has been no coal for the power plants.

In other rounds of the fight, China slapped huge tariffs on Australian barley and blocked Australia’s $3.7 billion a year trade in copper concentrate. Copper miners easily found customers elsewhere at a time of strong demand, while buyers in the Middle East and brewers in Mexico snapped up the barley that would have gone to China. Prices for both wheat and barley have been helped in a year that promises a record wheat harvest by Russia which has imposed an export tax on grain from its Black Sea region, in an effort to control domestic inflation.

Australia has been fortunate in that demand from China fuelled a resources boom and decades of uninterrupted growth. Now we are facing the consequences of that growth with one customer accounting for a third of our exports. But an incidental benefit of President Xi Jinping’s campaign is that the pain inflicted on certain industries will force those industries to develop markets in other.

An independent market measure of how Australia is faring in this trade tussle is the exchange rate for the dollar. All during the dispute both the trade weighted index (expressed as an exchange rate) and the US dollar exchange rate have been edging upwards as part of a long-standing trend. In contrast, the Chinese Yuan (traded international as the Renminbi) has shown little overall change against the US dollar but has been falling slightly against the Australian dollar. At the beginning of December one Yuan was worth around A21 cents. At the end of January a Yuan was worth A20 cents.

In other words, the international investment community has Australia ahead on points in this schoolyard trade tussle.

Mark Lawson is a former senior writer for the Australian Financial Review.