It’s the question that puzzles pundits and experts alike, with billion-dollar hedge funds, mum and dad investors and everyone between having a say and a stake in the answer: is Australia heading towards a recession?

Last Wednesday, Investors witnessed the worst trading day of 2019 and perhaps the most prescient indicator of an imminent recession, so it appears that the real question is actually when and not if.

The orange line represents the S&P 500, while the Christmas coloured line is Australia’s ASX 200. Although the dips are most severe in the United States market, it’s difficult not to notice the tight correlation between them.

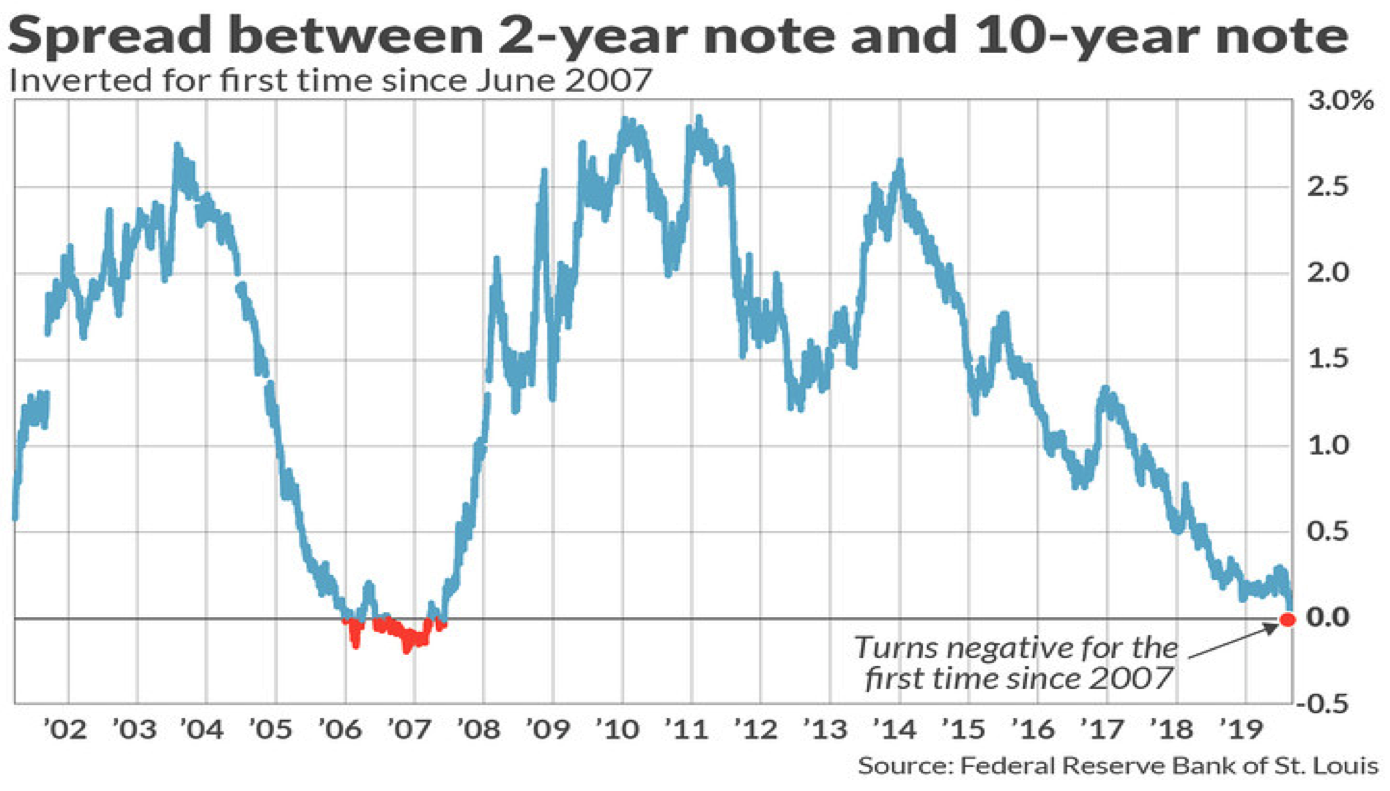

The stock market has its own Book of Revelations, and the Horseman of the Apocalypse is the yield differential between the 10 Year and the 2 Year US Treasury Bond. Treasury Bonds are investments you can buy from the government which give you a return in the form of coupon payments, which are like interest repayments on a mortgage. The government receives your cash upfront, and over the lifetime of the bond, you get your money back plus interest. So, the return (yield) on the 10-year bond is supposed to always be larger than its two-year equivalent, because investors demand a higher rate of return on an investment that ties up their money for longer. The interest rate differential between the two is known as the ‘spread.’

When the spread goes into negative territory, as it did on Wednesday for the first time since 2007, the relationship has ‘inverted,’ meaning that investors are moving well away from ‘riskier’ assets, like shorter-term bonds (such as two year bonds), and into longer-term ‘safer’ assets like 10 year treasuries. Longer-term bonds typically have a much lower default probability than their shorter-term counterparts.

The inverted yield curve is so enthralling important because it has successfully predicted all of the last seven major recessions going back to 1969. The truth is, that whether you use the spread between the 10-year curve and the two-year or three-month bond, the inversion has never boded well.

In the short term, however, as JP Morgan’s Mark Kalanovic indicates, things aren’t all bad, and you might even be able to make a bit of money on the volatility:

Historically, equity markets tended to produce some of the strongest returns in the months and quarters following an inversion. Only after [around] 30 months does the S&P 500 return drop below average.

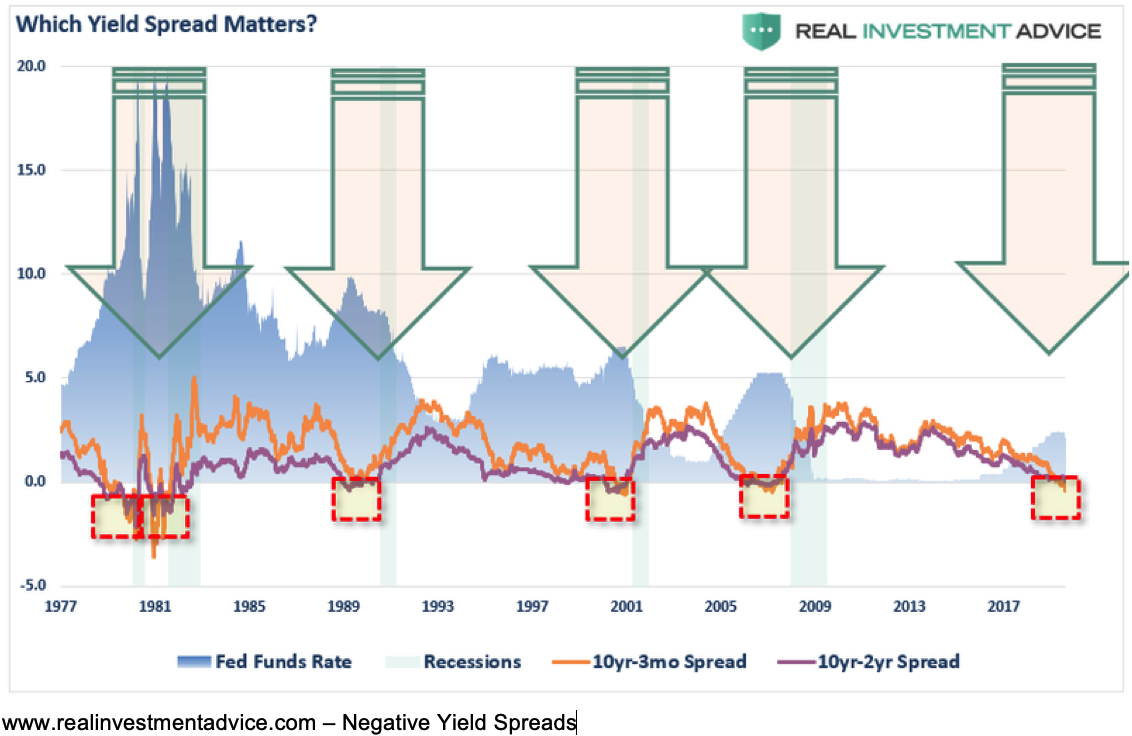

What investors and fund managers will now be looking at, is how rapidly the curve ‘un-inverts.’ It is the rapid positive growth of the spread, as we see most clearly in 1981 and in 2007 that calls forth the recession, whilst the inversion itself is typically the foreboding background music.

AMP Capital chief economist Dr Shane Oliver says the “The risk of recession in Australia is lower, probably 20 to 25 per cent,” whilst contending that the probability of a near term US recession is slightly higher, perhaps around 30 per cent or so. S&P this week upgraded odds of a US recession in the next 12 months to 30-35 per cent, up from 25-30 per cent last quarter.

Some commentators have pointed to economic data, suggesting that perhaps this time, the US economy is in much better shape than in previous yield-inversion contexts.

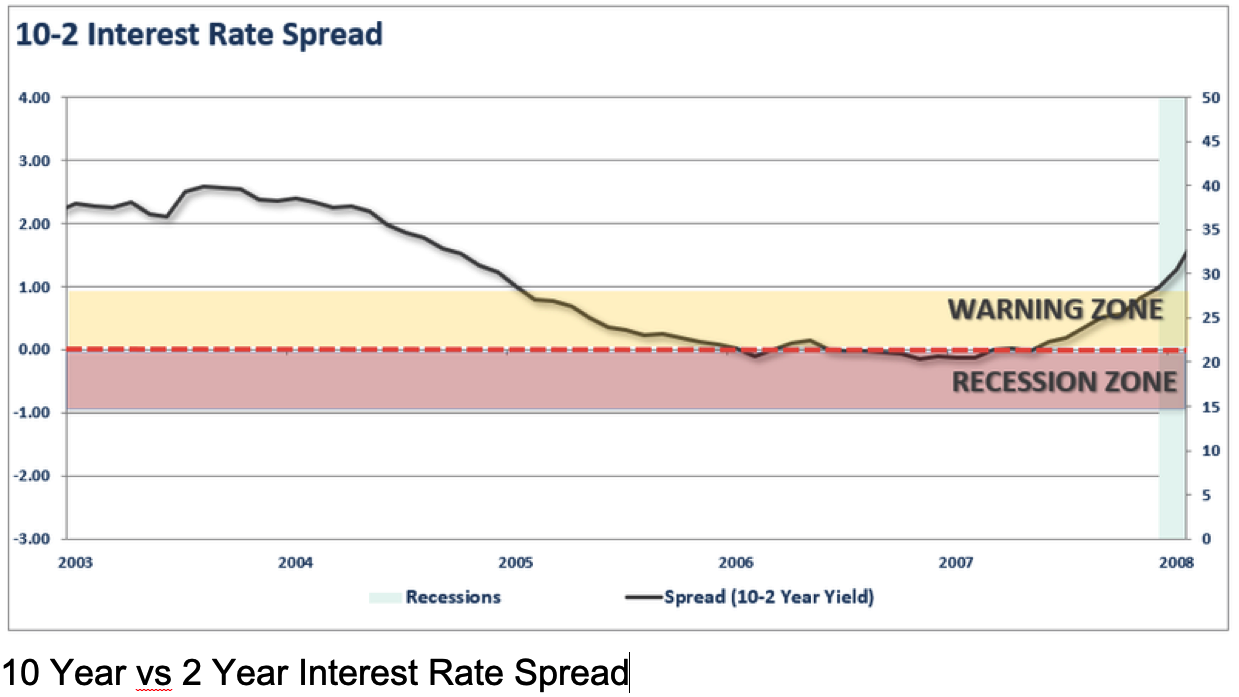

However, the onset in 2008 from the inversion was so rapid, it is difficult to regard any kind of complacency without suspicion.

When the recession hits the US, Australia will follow shortly afterwards. With such a heavy inter-market dependence and commodity prices far lower now than in 2008 and the depths of the GFC, Australia can’t rely on precious metals to prevent a contraction.

And the bad news keeps on coming, unfortunately, as we’ve all but run out of monetary options. RBA Governor Phillip Lowe has indirectly admitted what many ‘fringe’/Austrian economists have ruminated for some time, that central banks solve very little, and have almost no ability to prevent recessions. With the official cash rate sitting at one per cent, Lowe recently told the parliamentary economics committee “it’s possible we end up at the zero lower bound although I think it’s unlikely.” To be pontificating over introducing near-negative interest rates in a period of non-recession suggests to the critical observer that Lowe is not only flogging a dead horse but that the whip never worked in the first place.

And the bad news keeps on coming, unfortunately, as we’ve all but run out of monetary options. RBA Governor Phillip Lowe has indirectly admitted what many ‘fringe’/Austrian economists have ruminated for some time, that central banks solve very little, and have almost no ability to prevent recessions. With the official cash rate sitting at one per cent, Lowe recently told the parliamentary economics committee “it’s possible we end up at the zero lower bound although I think it’s unlikely.” To be pontificating over introducing near-negative interest rates in a period of non-recession suggests to the critical observer that Lowe is not only flogging a dead horse but that the whip never worked in the first place.

For the Austrians among us, there may be some kind of silver lining, as a contraction may bring about a renewed focus on the role and efficacy of the central banks. Murray Rothbard’s ‘Case Against the Fed’ is perhaps the best explanation of why Central Bank’s can’t solve underlying structural issues and, in fact, make everything a whole lot worse.

What’s absolutely apparent, irrespective of your opinion on Rothbard or central banks in general, is that an American plunge leads to an Australian dive, and if the yield curve is even slightly reliable, there will be no escaping the contraction this time. Watch for safe-haven assets like gold and bitcoin to surge in the next few months, as the capital tries to protect itself from the invariable contagion effect, that almost always follows the inversion.

Alexander Cameron is a recent Sydney University Graduate with a degree in Finance and Banking. You can see more of him and his two brothers at www.carnagehouseproductions.com.

Got something to add? Join the discussion and comment below.