This afternoon the Bank of England’s governor Andrew Bailey appeared, as he has done many times before, in front of the Treasury Select Committee to answer questions about its recent decision-making. Yet the tone of the Committee was radically different to other sessions. Its chair Mel Stride opened by asking Bailey if he and the Monetary Policy Committee – made up of nine members who vote to set interest rates – had been ‘asleep at the wheel’ as prices soared throughout the country. It was arguably one of the easier questions put to him during today’s session: from then on, Bailey and the MPC members who joined him were pit against each other. They were asked to explain when they realised the inflation tiger had escaped – and what they had individually done to put it back in its cage.

Bailey had nowhere to hide during this session: he was sat between other MPC members who moved faster than he did to increase interest rates and roll back money printing. This included Michael Saunders, the outgoing committee member, who pointed out that he had been pushing for a more hawkish policy even as recently as the latest vote, when he was outvoted in his bid to increase interest rates by an additional 0.25 per cent. Saunders did not want to completely throw the governor under the bus, arguing that hiking interest rates last year wouldn’t have made a meaningful difference to short-term inflation spikes. But this isn’t much of a defence for Saunders.

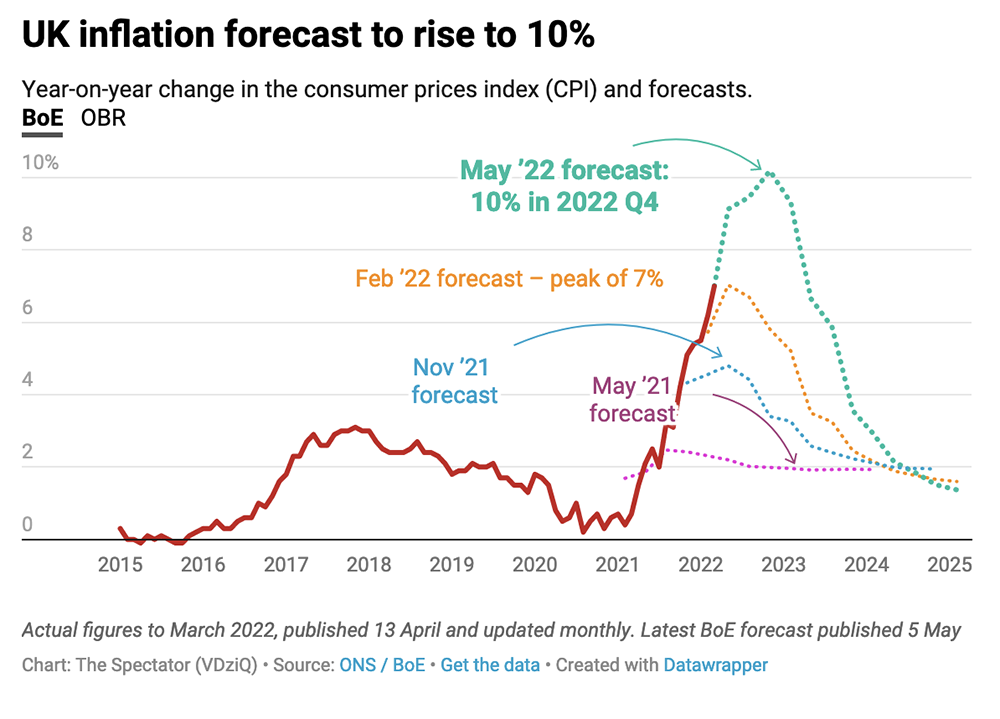

The line of reasoning used throughout the session by the governor was that the price hikes Britain is experiencing are largely unavoidable. ‘80 per cent’ of these rises are due to international phenomena that are out of domestic control, we were told; these can’t be curbed by monetary action from the Bank, was the message. According to Bailey today, those factors were largely down to Russia’s war in Ukraine, which he believes largely explains why inflation in Britain is on track to hit double digits by the end of the year.

‘We can’t predict things like war,’ he said towards the beginning of the session, and emphasised this surprise factor throughout. ‘Prices started to spike up last November really, with the build-up of troops…but then they really ramped up around the invasion in February.’

No one disputes that Russia’s war has contributed to rising energy costs and increases to the headline inflation rate overall. But Bailey’s overall narrative isn’t supported by the data.

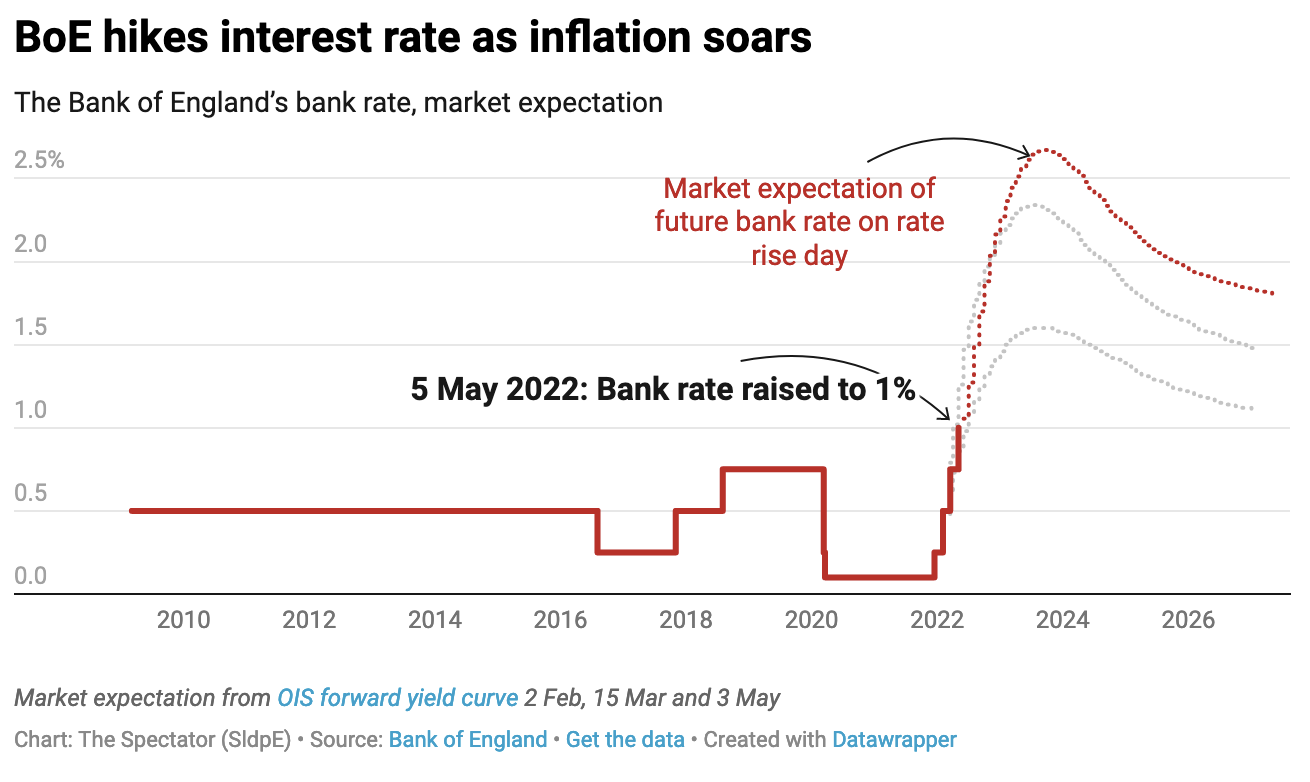

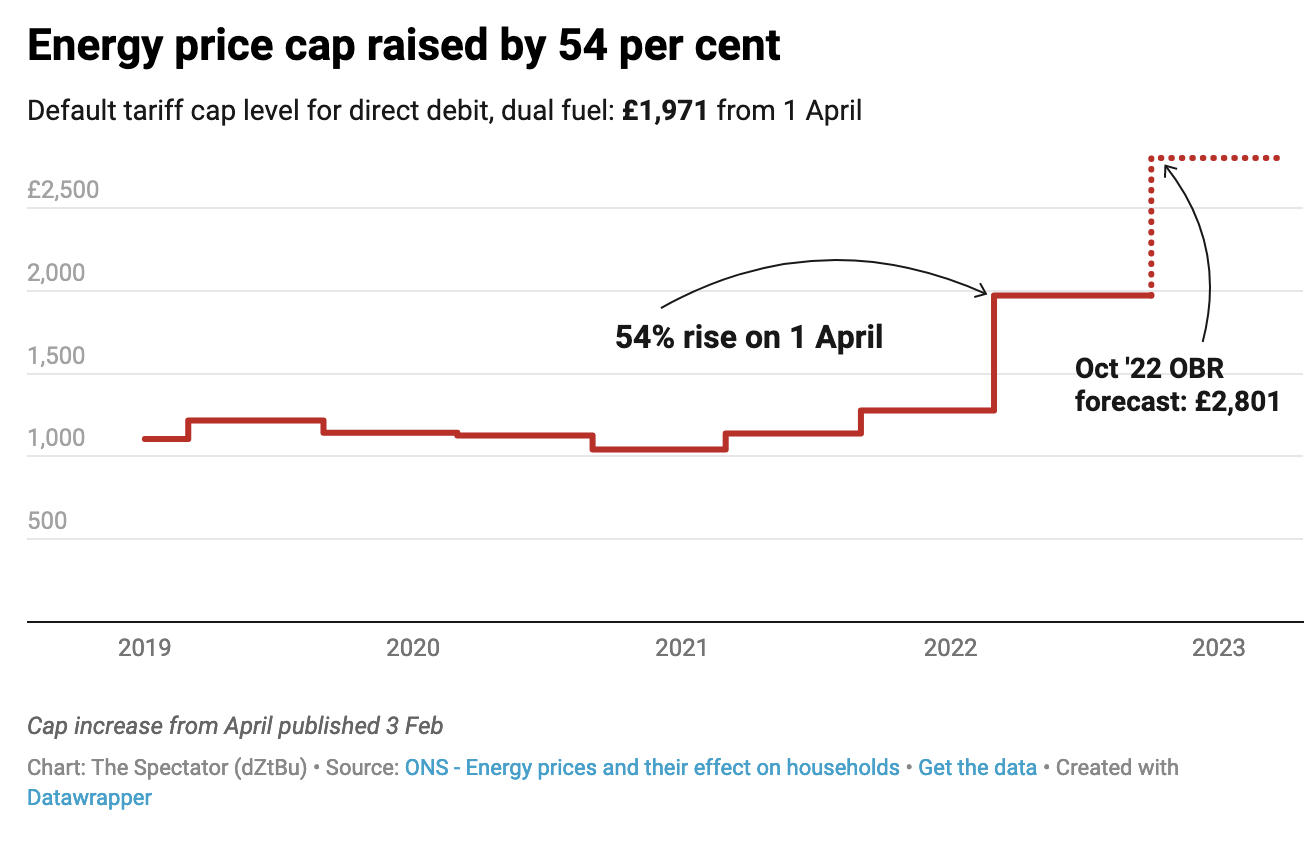

Inflation passed the Bank’s target of 2 per cent last May, and had hit over 3 per cent by the end of the summer. By November, the headline rate was 5.1 per cent, more than double the Bank’s target. By February, still weeks before Vladamir Putin ordered his troops across the border, Chancellor Rishi Sunak had published a £9 billion package to deal with Ofgem’s energy price cap hike, which increased the average household’s bill by a staggering 54 per cent.

Bailey is right to point out that inflation is causing international headaches, but much of that is a result of major supply chain issues created by the pandemic and subsequent lockdowns, which still have not been resolved. And while Bailey was made to look behind the curve by several current members of the MPC today, they are all made to look painfully slow by their former colleague Andy Haldane, who was warning (and voting) last summer that interest rate hikes were needed to tackle inflation while it was still in its infant stages. As hard as they may try, they cannot feign ignorance or hide behind the disruption caused by Russia: central bankers like Haldane, and politicians like Rishi Sunak, saw the many ingredients for an inflationary spike being mixed together. Yet their warnings fell on deaf ears.

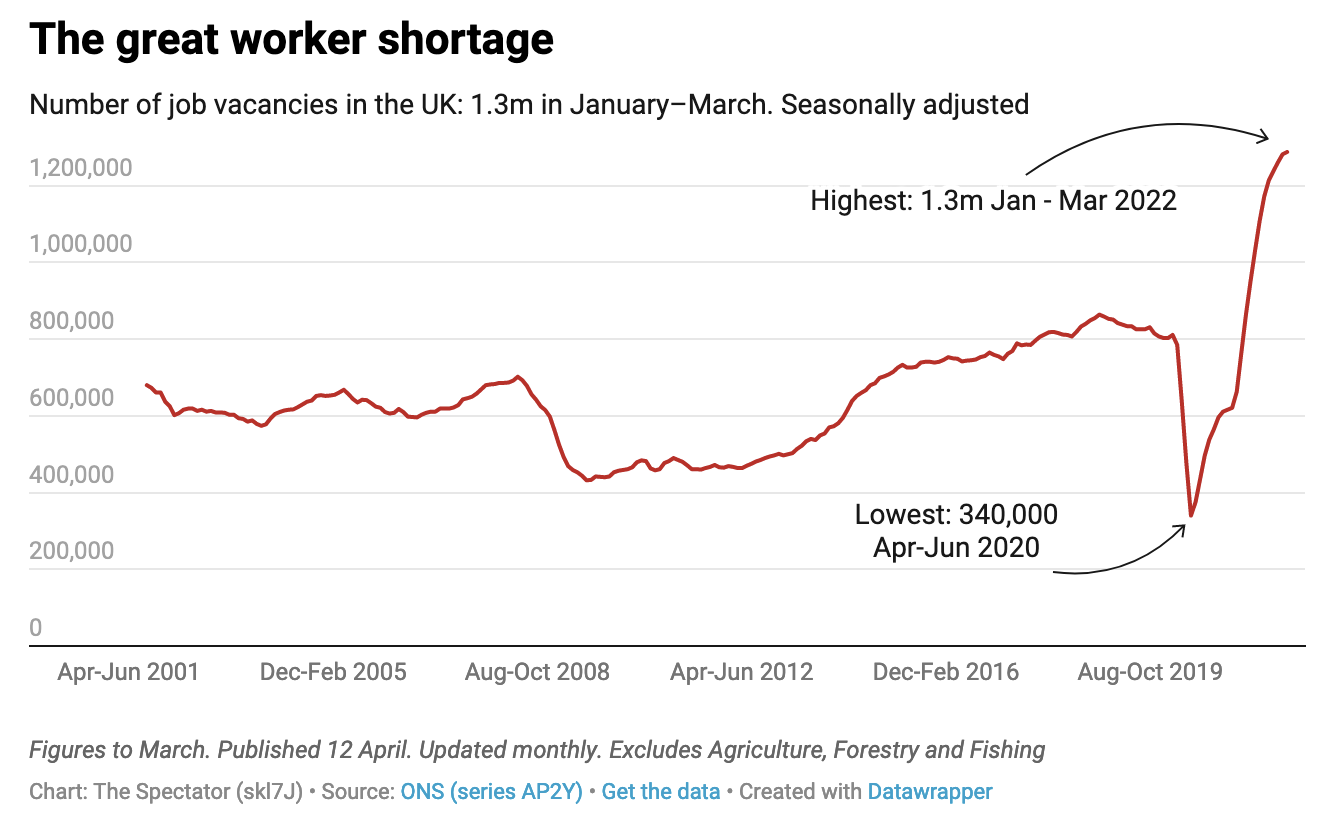

While Bailey was full of excuses, he had little to offer in the way of hopeful predictions for the medium-term. The BoE’s projections don’t see inflation falling back down to the Bank’s target until 2024; and still Bailey admitted that the ‘balance of risks is on the upside’, with both domestic and international factors at play. At home, the risk remains that the labour market ‘doesn’t cool down’, and that job vacancies continue to soar, leading to a wage spiral that fuels inflation. Bailey clarified that he never meant to suggest people shouldn’t get pay raises, but encouraged high earners to ‘reflect carefully’ about asking for more money and potentially contributing to wage inflation. There are also outstanding questions about what people will do with their pandemic savings, and whether there will be sustained demand that outstrips supply.

When it came to matters overseas, Bailey paid lip service to the supply chain disruption that continues to plague China. Figures out this morning show retail sales fell by 11 per cent in China (double what the consensus predicted), providing even more evidence that the country’s zero-Covid strategy continues to bite. Also mentioned were the risks of a major energy price shock, likely caused by Putin making a unilateral decision to cut off Russian gas to Europe.

But none of these were Bailey’s greatest concern. The governor told the Treasury Select Committee he really gets ‘apocalyptic’ about inflation when it comes to food prices, noting that world wheat prices have gone up by ‘just under 25 per cent’ since his last appearance at the select committee meeting, with so much of the world’s reserves stored up in Ukraine and difficult to transport.

It was a tough session for the Bank’s governor, but arguably much worse for any member of the public tuning in. Those who watched this session will realise that this inflation nightmare is far from over, and that Bailey is ready to place the blame for that just about anywhere other than on the Bank itself.