Is the Bank of England about to cut interest rates? Today’s labour market statistics might just give them the room to do so. The latest data, released by the Office for National Statistics (ONS) this morning, shows that the number of payrolled employees is up, the unemployment rate is up, vacancies are down and pay growth is slowing. But is it enough?

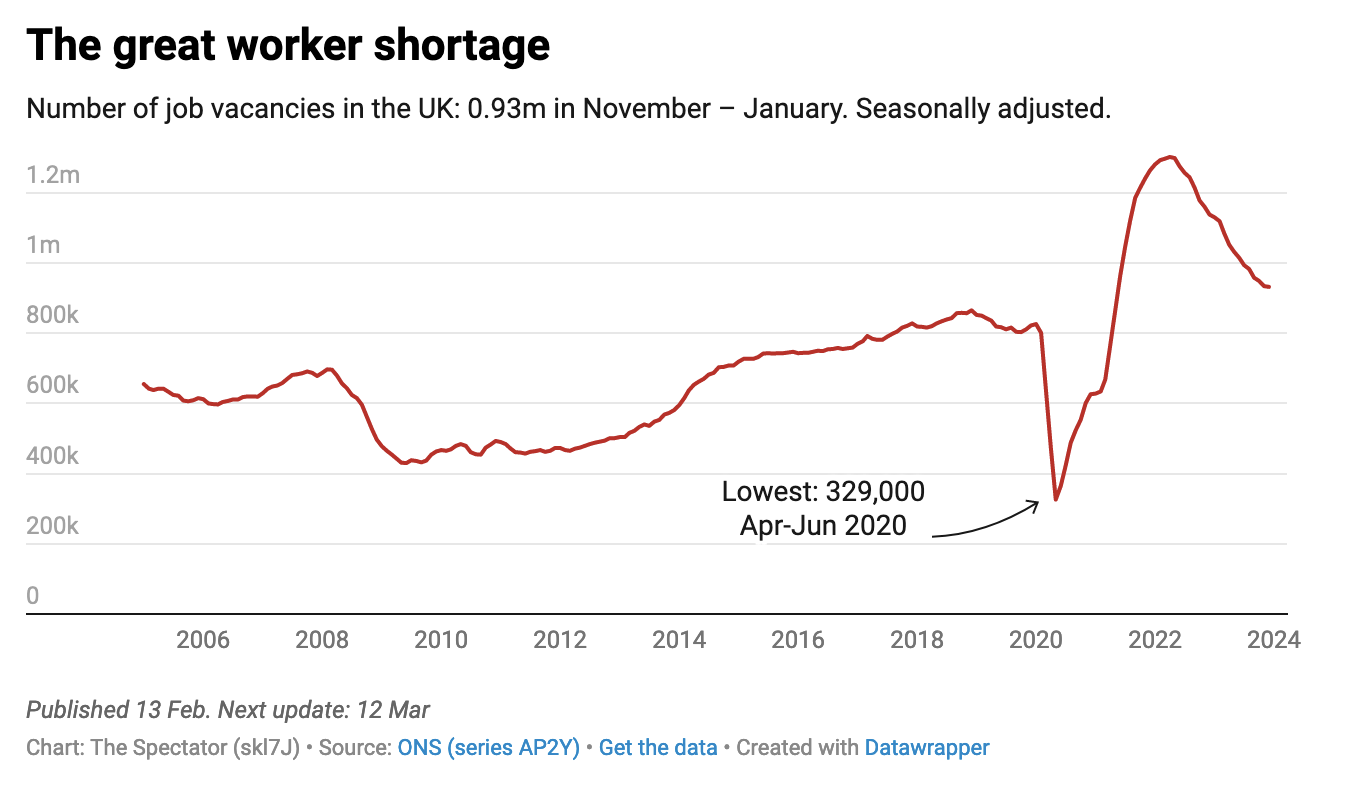

Job vacancies fell for the 20th consecutive time between December and February – and by twice as in last month’s release. Vacancies were down to 908,000 on the quarter, a decrease of 43,000 – though they remain far higher than pre-lockdown levels. More data released yesterday by the Reed recruitment agency supports this too: job adverts are at their lowest level in more than three years. Falling recruitment is a clear sign that the heat is coming out of the jobs market.

Against expectation, the unemployment rate rose on the year to 3.9 per cent – another sign Bank of England rate setters will be looking for. Though there are some 85,000 more British adults in employment than before the first lockdown, it’s quite a different story when we look at inactivity. The number of those not in work or looking for it stands some 700,000 higher than it did pre-lockdown. And that’s 44,000 up on the previous three months – the equivalent of all the inhabitants of Greenock, Salisbury or Llanelli packing it in a single quarter.

The drivers behind economic inactivity have changed though. In the first years following the pandemic, the departures from the workforce came from early retirement and sickness, with the 50 to 64 year old group making up the lion’s share. In today’s figures, however, the rise is most stark in the 16 to 34 year old group, whilst most older age groups have seen falls.

Liz McKeown, the ONS’s director of economic statistics, said: ‘If we look over the last year we’ve seen that increases in inactivity have been concentrated in the younger age groups, particularly in that 16 to 24 year-old age group. We’ve seen that increase by 248,000 over a year. We’ve also seen employment going down for young people. While the number of people has gone up overall, that isn’t true for the 16 to 24 age group.’ This is quite the worrying trend.

Meanwhile, there are more signs of a cooling jobs market in the redundancies data. They show layoffs up with the redundancy rate more than doubling on the quarter. Taken together with falling vacancies, it’s a sure sign that employers are hunkering down for a recession. Again, something the rate setters of Threadneedle Street will want to see before bringing rates back down.

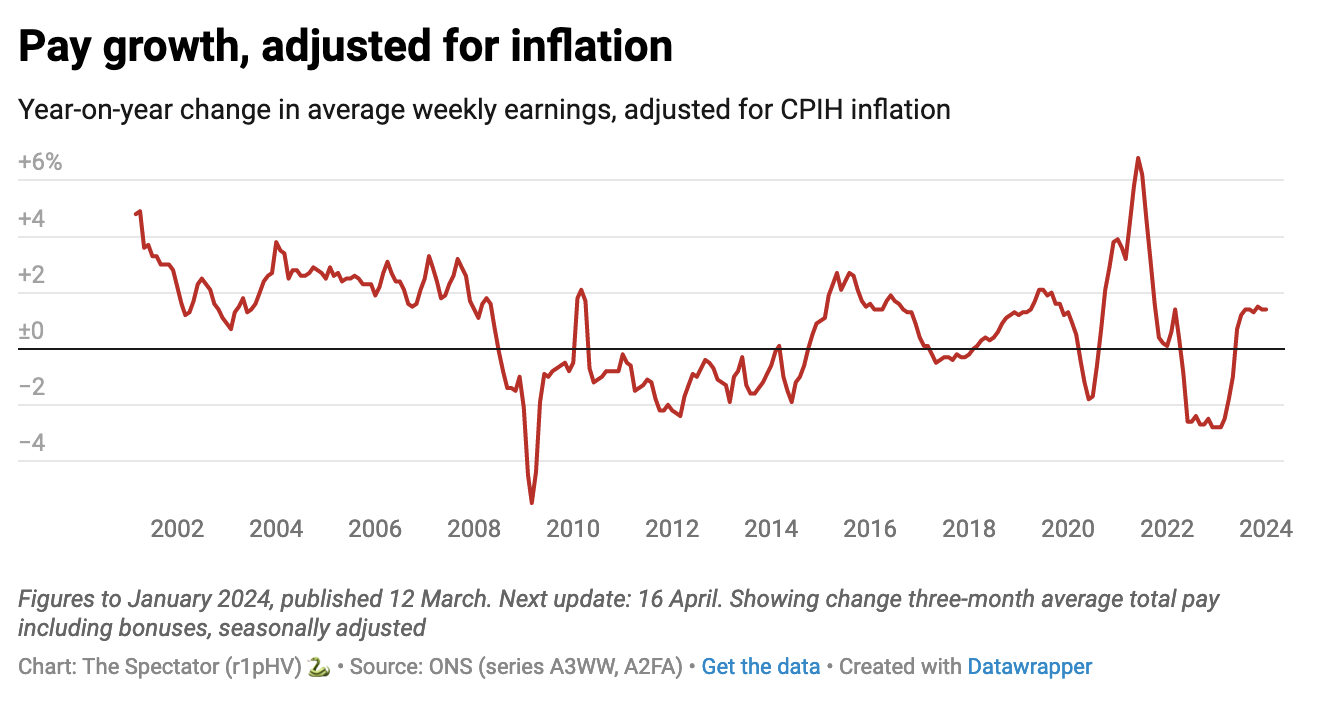

Perhaps the most important release though, and one that will have pleased the Bank, is the slowing of wage growth. Whilst working Britons have now seen 16 consecutive months of average pay rises above 6 per cent – on the year that’s 1.8 per cent wage growth in real terms – today’s figures showed a slowdown in pay rises. The Bank has said they want to see this continuing to be sure that the inflationary pressures on the economy are easing off.

So, most of today’s labour force data is headed in the right direction for the Bank to cut rates. But don’t get your hopes up. Whilst markets and pundits alike expect them to be cut this year from the 5.25 per cent they sit at now, it’s not going to be anything drastic. The latest market expectation has rates above 3.5 per cent well into the next three years. For that to change we’re going to have to see something more fundamental happen to the UK’s jobs market and really do something about enduring sickness and the young shying away from work.