What is the appropriate act to mark the fiftieth anniversary of Value Added Tax in the UK? Are we celebrating? Surely not. Are we mourning? If only. But we should at least pause and reflect on the central role that VAT has played in our recent economic history.

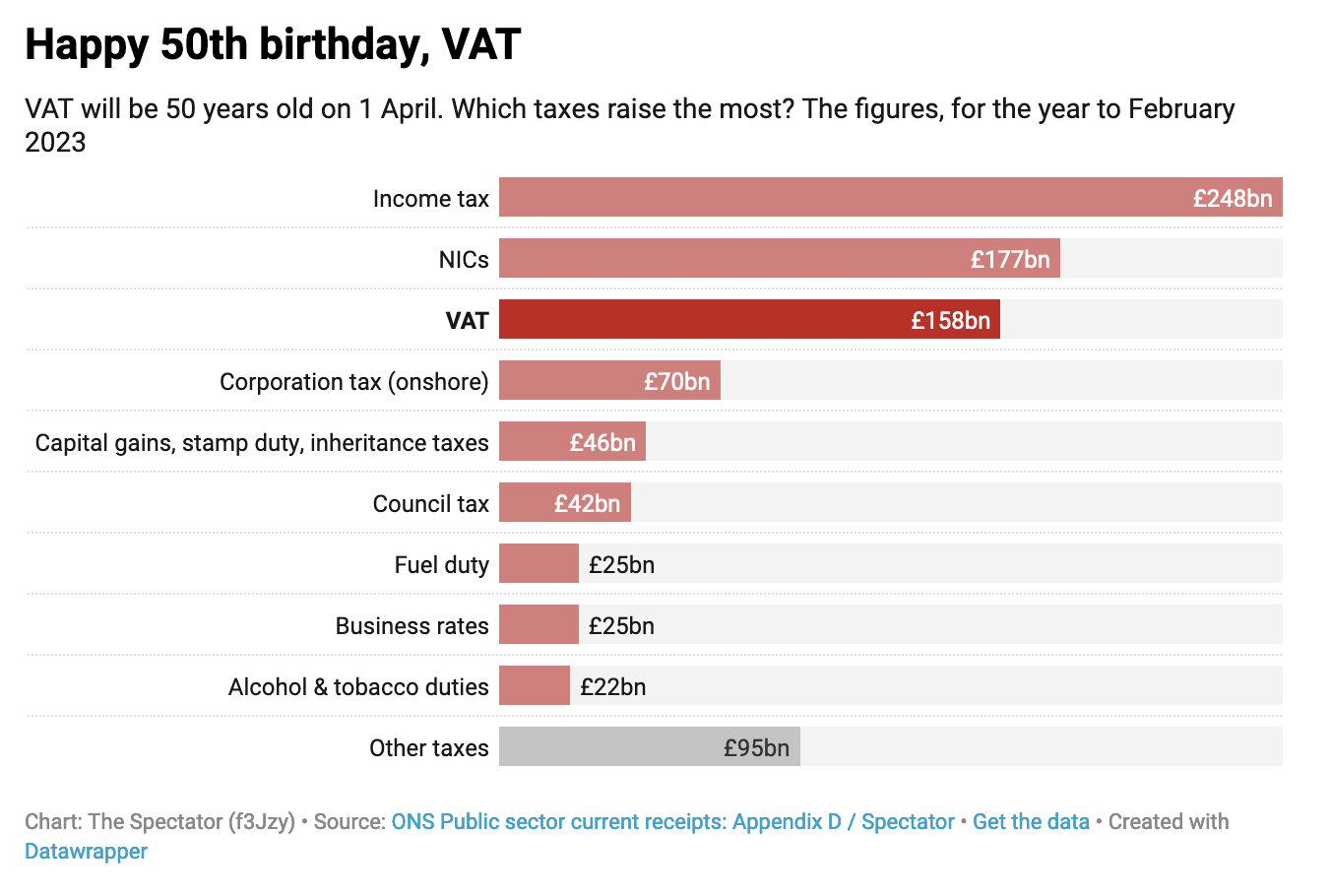

The third largest source of tax revenue, forecast to deliver over £160 billion to the Exchequer this year, VAT has always been a cash-cow, but never without complaint. Most of the debates surrounding its introduction in 1973 focused simply on who and what should remain outside its claws.

If you want an indication of what a different world this was, just look at Anthony Barber’s explanation to the Commons of the risks that the zero rate for children’s clothing could be misused.

‘Unfortunately’, he began, using language surely racily provocative even back then, ‘it is no part of my responsibility as Chancellor to add to the many advantages already enjoyed by slim and nubile young women.’ But, he went on, a more restrictive relief would be difficult to design, in a situation where ‘so the Customs experts tell me, the waist measurement of the current Miss World is that of an average young girl of 12.’

And therein lies the complexity of what should have been a simple tax. Instead of each business in the supply chain passing on their VAT costs and the end consumer footing the final bill, there are a wide range of goods, services and organisations to which that process does not apply.

There are zero rates on goods like children’s clothing, inherited from the old purchase tax that came before 1973; and reduced rates applied to other goods, every one of those reliefs a bitterly contested legal battlefield over what qualifies and what does not.

Even more complex, there are multiple entities who do not charge VAT on the services they provide, either because they are too small to register, because they are not considered to be ‘in business’, or because their supplies were ruled exempt from VAT under EU law.

That leaves a wide range of organisations – from banks and bookies to charities and childcare providers – paying VAT on the goods and services they buy, but unable to pass it on to an end consumer or claim it back from HMRC. Their resulting efforts to change their status and swerve those VAT costs have again kept the nation’s tax accountants in clover these past 50 years.

Despite being freed from the EU rules that constrained Gordon Brown, not one of the seven Chancellors since the 2016 referendum has sought to reshape the VAT system

Throughout the public service sector, from hospitals to Whitehall departments, special VAT refund schemes exist to avoid those costs, but even here, there is complexity and rancour. Tony Blair’s academy schools and Nicola Sturgeon’s Police Scotland both found themselves with unexpected VAT bills after being set up in ways that disqualified them from the existing refund schemes.

VAT has therefore been a constant source of frustration for scores of ministers over the years, including me, and equally so for the hundreds of MPs who have helped lead campaigns for the extension of VAT reliefs.

But for the Treasury, all that complexity has been worth the headache, for what has proved in the past five decades to be an extremely efficient and reliable means of taking money out of taxpayers’ pockets, and very occasionally putting it back.

Indeed, time and time again, teaching our King’s College, London class on the ‘Treasury and Economic History since 1945’, Professor Jon Davis, Lord Nick Macpherson and I find ourselves explaining to the assembled group of master’s students and Treasury civil servants how VAT has been at the heart of some of the most significant political and economic decisions of the past fifty years.

Between 1974 and 1976, Dennis Healey used the VAT system aggressively as a tool of economic policy, cutting the main rate from 10 per cent to 8 per cent to try and control inflation, and attempting to ration petrol use by taxing road fuel at a new higher rate, a basket into which he later added other perceived ‘luxuries’ such as white goods, electronics, jewellery and fur coats.

In his June 1979 Budget, Geoffrey Howe set the Thatcherite tone on taxation by slashing the basic and top rates of income tax, and hiking VAT from 8 per cent to 15 per cent to pay for it – just about consistent with Margaret Thatcher’s election promise not to double it. He also did away with Healey’s differential treatment of luxury goods, an experiment never since repeated.

In 1991, Norman Lamont used a VAT hike to escape the shackles of the poll tax, raising the standard rate from 15 per cent to 17.5 per cent to fill the hole left by scrapping the ‘community charge’, a crucial moment in establishing distance for John Major’s government from Margaret Thatcher’s.

Two years on, Lamont imposed VAT on home energy bills – a decision which surely hastened his sacking – with his successor Ken Clarke defeated in the Commons when he tried to push through the second phase of that increase in 1994, another heavy nail in the Tory coffin to go with those hammered in on Black Wednesday.

Gordon Brown cut VAT on energy bills to 5 per cent in 1997, the lowest rate permitted under EU law, and did likewise with a host of other items over the next decade, from children’s car seats to tampons (an announcement he could not quite bring himself to include in the Budget speech). Where a reduced rate was not allowed by Brussels, he introduced more VAT refund schemes, notably cutting the cost of church repairs and enshrining free entry to the nation’s museums and art galleries.

In 2008, Alistair Darling chose to cut the main VAT rate to 15 per cent for 12 months to inject support into an economy reeling from the global financial crisis, and two years later, George Osborne chose a permanent hike to 20 per cent to bank additional revenue at the start of his austerity drive.

Since then, VAT has remained largely untouched as a policy tool, not least after Osborne’s short-lived attempts to scrap the reliefs on pasties and caravans in his 2012 ‘Omnishambles Budget’. After that disaster, you sense that subsequent submissions to Treasury ministers for changes to the VAT system have been put straight into a box marked ‘Do not touch’.

Indeed, it is notable that – in contrast to Dennis Healey – there has been no interest in tinkering with VAT as a short-term response to the inflationary pressures of the past two years.

Even more surprisingly, despite being freed from the EU rules that constrained Gordon Brown, not one of the seven Chancellors since the 2016 referendum has sought to reshape the VAT system in any meaningful way to suit the needs and wishes of a post-Brexit Britain. After all, there are many options open to them that were never a possibility during my time at the Treasury.

Doubtless, Treasury civil servants will have papers ready on the shelf in case ministers decide to consider – for example – turning exemptions for some sectors into zero or reduced rates. Or allowing lower rates of VAT to be charged by smaller firms in struggling regions to add bite to the levelling-up agenda. Or finding a less complex and restrictive way to reduce the VAT burden on public services and charities. Perhaps they will start by simply asking how best to structure and administer VAT to support growth, promote fairness, and reduce bureaucracy, without having to worry whether the changes are permitted under single market rules.

In 2001, Lord Justice Sedley described the ‘world of VAT’ as ‘a kind of fiscal theme park’. To borrow that analogy, many of the most interesting attractions that have been roped off for the past 50 years are now available for ministers to ride. Who, I wonder, will be the first to climb aboard?