Jeremy Hunt set out at the start of the weekend with one goal in mind: that when the gilt markets reopened on Monday, the cost of government borrowing would not surge further. Ideally, it would start to fall.

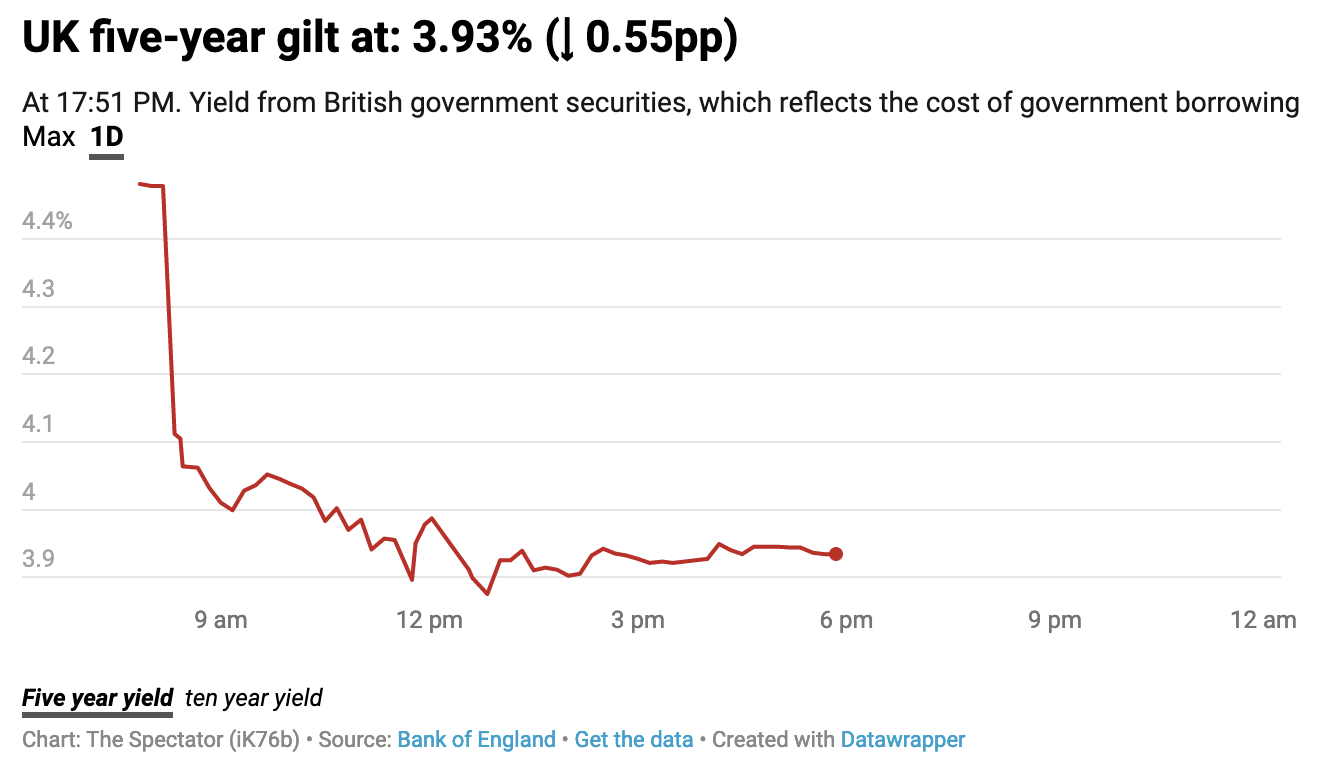

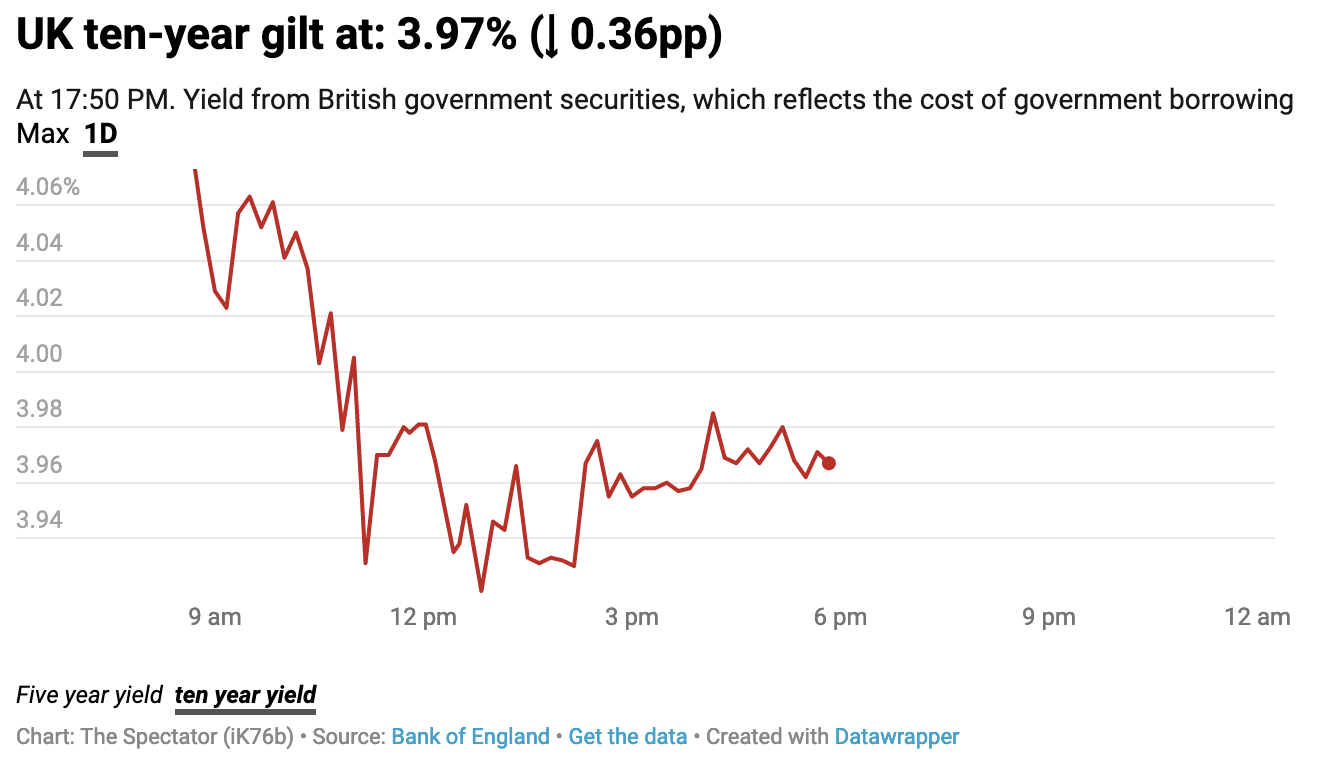

In this sense, it’s been a successful day for the new Chancellor. The Treasury’s early morning update that a major fiscal announcement was about to be announced saw gilt yields start to drop when markets opened at 8 a.m. After Hunt’s overhaul of the mini-Budget – including the surprising decision to suspend the 1p cut to the basic rate of tax ‘indefinitely’ – they fell even further. After starting the day at almost 4.5 per cent, the five-year gilt yield is ending the day just below 4 per cent. The ten-year gilt yield has fallen, slightly less, from 4.1 per cent to 4 per cent.

Market expectations for peak interest rates has also fallen too, now down to just over 5 per cent, compared to more than 6 per cent that came to be expected after the mini-Budget was announced. It’s a point the government will be keen to emphasise, in terms of the impact of future mortgage payments. And the pound rose against the dollar: starting the day at $1.12 and ending at just under $1.14. All these updates suggest markets are tentatively positive about what the Chancellor announced today; that the £32 billion worth of revenue he clawed back by undoing Liz Truss’s tax cuts have gone some way to convincing markets that this government is still interested in fiscal discipline.

But as I noted this morning, before Hunt’s announcements, it’s a long road back to credibility. Once a government loses economic confidence, it’s extremely difficult to get it back – and the cost of doing so can be sky-high. One of those costs has come not just in money, but in language. Today in the House of Commons, there was broad concession from both Penny Mordaunt (who stood in for Truss to answer Labour’s urgent question) and Hunt that the government’s recent actions had been a major mistake: ceding all sorts of political ground to their opponents.

Furthermore, Hunt has not just U-turned on Truss’s policies to try to get the markets back on side; he has had to give up core economic principles that the Conservate party usually grips tightly. In his media statement this morning, Hunt insisted that he agreed with the principle that taxpayers should keep more of their own money, but under these circumstances, it is ‘not right to borrow’ to fund even a cut to the basic rate. Yet in the Commons this afternoon, he praised the fact that he has ‘shown Conservatives can raise taxes’, with Truss looking expressionless next to him, having curated an entire leadership campaign and government-defining mini-Budget around slashing tax instead.

Fear remains among Truss fans and critics alike that the mistakes of the past few weeks will usher in permanently higher borrowing costs and interest rates. Would they have risen so quickly, or to such heights, if the mini-Budget had been introduced in a more market-friendly way? But before that fear can be fully grappled with, we must wait and see if today’s updates have really calmed the markets. The calm could just be a small hiatus from the ongoing economic storm.<//>