Women, women, women. Aren’t you sick to death of hearing about women? Endless bleating about women’s tough lives, whining about women being badly done by, mistreated and deprived.

Our captured institutions are busy trotting out dubious research reports and cherry-picked statistics claiming that the women in our pampered country are missing out and in need of urgent funding to address their disadvantage.

Take a look at the recent boondoggle from the Australia Institute, claiming Australia’s tax concession system is stacked against women. The researchers’ analysis claimed four tax concessions: negative gearing, superannuation tax concessions, capital gain tax discount and refunding excess franking credits, costs the Federal Budget $60 billion per year; and for every dollar that goes to women, two dollars goes to men.

I’ll unpack their spurious arguments later, but this is just one more sally in the constant barrage of propaganda about women’s lack of financial security. You’ve all heard the arguments about women’s pitiful superannuation leaving them prone to nightmares about becoming bag ladies.

A spanner in the works

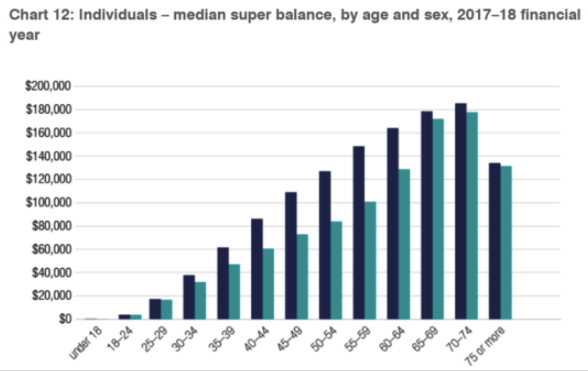

Well, I’ve got interesting news for you. Take a look at this neat little graph buried on the ATO website:

As women grow older the gender gap in super miraculously evens out, with men and women ending up pretty much level. This means that one way or another, older women end up with more of the men’s loot.

It’s highly unlikely that these older women are suddenly earning much more to account for their increase in super balances. Most of them must be losing their partners and ending up on their own. Many of these women outlive their men – the current gap in life expectancy is about five years and with most women partnering slightly older men, they enjoy the financial benefits for long after his passing. As named beneficiaries for the man’s super what was his is now hers.

One of my correspondents, a former senior public servant, informs me that Commonwealth defined benefit super schemes pay the beneficiary for life 67% of the pension the contributor was receiving. You can simultaneously collect three of these pensions if you choose your deceased spouses carefully – the limit of three apparently came in when the relevant authority noticed they had a woman who had lodged her third death of a spouse beneficiary claim!

Sometimes these older women turf the man out. Yes, it is mainly women making the decision to divorce even in these older age groups. Take a look at this article I wrote well over a decade ago about broke, older divorced men, which focussed mainly on once high-earning professional men whose marriages end with a late divorce. Usually, she gets the house and bulk of the assets, even if he manages to hang onto the super. But his finances never recover.

His money is their money but hers is hers alone

Many older men also transfer super to their partners. People aged over 60 can access a “condition of release” to take up to $300,000 out of super tax-free. Husbands often put it in the name of a partner with a lower super balance which can help with managing taxable balances, reducing tax on death benefits, and sometimes allowing access to Centrelink payments.

With older women still in relationships, those high levels of super showing up in the men’s bars on the graph are actually being shared with their partners. ABS data shows 36% of retired women relied on their partner’s income to meet their living costs at retirement (compared to 7% of retired men). It’s nonsense to suggest that older men live high on the hog due to tax concessions. There’s usually a grey-haired wife luxuriating right next to him on that fancy retirement cruise.

Right through their time together, partnered women are beneficiaries of men’s higher earnings – it’s long been the case that women control the purse strings in most marriages. That’s where the feminist argument is so duplicitous, carrying on about women’s lower super and lower earnings without taking into account the fact that most women’s economic security actually comes from living with higher-earning men.

Women have always sought out men who can provide that security (and low-income women often reject the dubious male prospects on offer, preferring more stable and lucrative government largess in the form of sole parent pensions). Most men’s economic security relies on them working full time for decades, often marking time in unfulfilling jobs.

It’s a devious sleight of hand to treat partnered women’s super as her sole means of financial security, claiming her low personal super is an indictment of our system.

I’ve always been amused at the irritation of feminist researchers when their studies reveal many women aren’t resentful of doing the bulk of family work. The researchers naturally bury the evidence showing men and women’s total work time, combining paid and unpaid work, is remarkably even. That’s why many women see themselves as getting a fair deal.

But the feminists are bent on making mischief. And the Australia Institute dutifully plays to their tune.

The Australia Institute’s lies, damned lies, and statistics

So, let’s unpack The Australia Institute’s claim that claiming Australia’s tax concession system is stacked against women by looking at some real facts:

The tax concessions the researchers have focussed on provide most benefit to higher-income earners. The reason men benefit most from these schemes is their gender earns most of the high incomes and pays most tax.

Higher-income earners pay a lot more tax. For instance, median annual income (before tax) is $48,000 and the tax on that is about $7,000. A person earning twice that, $96,000 pays about $23,000 tax – more than three times the tax, for twice the income.

Women earn less not due to discrimination – it’s illegal in our industrial relations system to pay a woman less than a man for doing the same job – but because they choose jobs that are less well paid, avoid high-paid, risky employment, and arguably are less good at negotiating salaries.

But the killer issue here is women work so many fewer hours in paid employment. Around 45% of working women are employed part-time, compared to less than 20% of working men. Women spend a far smaller hunk of their lives in the paid workforce, let alone working full-time, and retire significantly earlier. ABS Age at Retirement data shows a quarter of all women have retired from the workforce by the age of 45, compared with only 7.5% of men. Clearly, women’s shorter history of paid full-time employment is not just due to child-care responsibilities.

Super expert Noel Whittacker points out for every dollar in super, women still earn less than men because they often can’t be bothered keeping track of the multiple super accounts acquired through their various part-time earnings and they are also more risk-averse, keeping their super in more conservative options throughout their lives. The difference in earnings can be huge, he explains, using the following example:

“Two people start work at age 20 on $35,000 a year. Let’s assume their salary grows at 4% per annum and employer contributions remain at 9.5%. The first person is extremely conservative, so their fund earns only 4% per annum. At age 65 their superannuation balance is $750,000. The second person adopts a more growth-orientated asset allocation and as a result their fund earns 8% per annum. At age 65 their superannuation is worth $2 million.”

Men earnings pay for women’s benefits.

Funny that we never hear about all these anomalies in the “poor me” script now part of the narrative about women’s finances. But even more taboo is any discussion of the fact that men’s earnings are paying for women’s benefits.

On average, as a group, women pay considerably less tax and receive substantially more benefits. Have a look at this Centrelink payment data – showing that in almost every category there are more female recipients than male. For instance, there are 23% more female aged pensioners than male.

That’s where significant amounts of the tax paid by these high earning men ends up – providing benefits for women. Social security and welfare represent about 35% of Australian Government expenditure (around $192 billion in 2019-20), with the aged pension alone representing about 10% of expenditure (around $50 billion).

Personal income tax paid represents 47.2% of Australian Government revenue and about one in every five dollars of income tax paid is going toward the cost of the aged pension.

The feminists might want to think more carefully about where this debate could lead them. But provided they maintain their stranglehold on mainstream media, there’s not much chance of these inconvenient truths emerging.