At the time of Rachel Reeves’s big-spending first Budget in 2024, the Office for Budget Responsibility (OBR) came under criticism from the left for its apparently overly pessimistic estimates of how much government spending increases economic output.

Earlier this week, the OBR published its annual Forecast Evaluation Report, which looked at estimates of these ‘fiscal multipliers’ over the short term. Bigger multipliers mean a larger economy – and a larger economy means more tax revenues. That’s why people say spending can pay for itself. The OBR has a range of multipliers it uses as starting points for different types of spending, dialling them up and down according to its judgements on the state of the economy (is there spare capacity to fill?) and the policy in question.

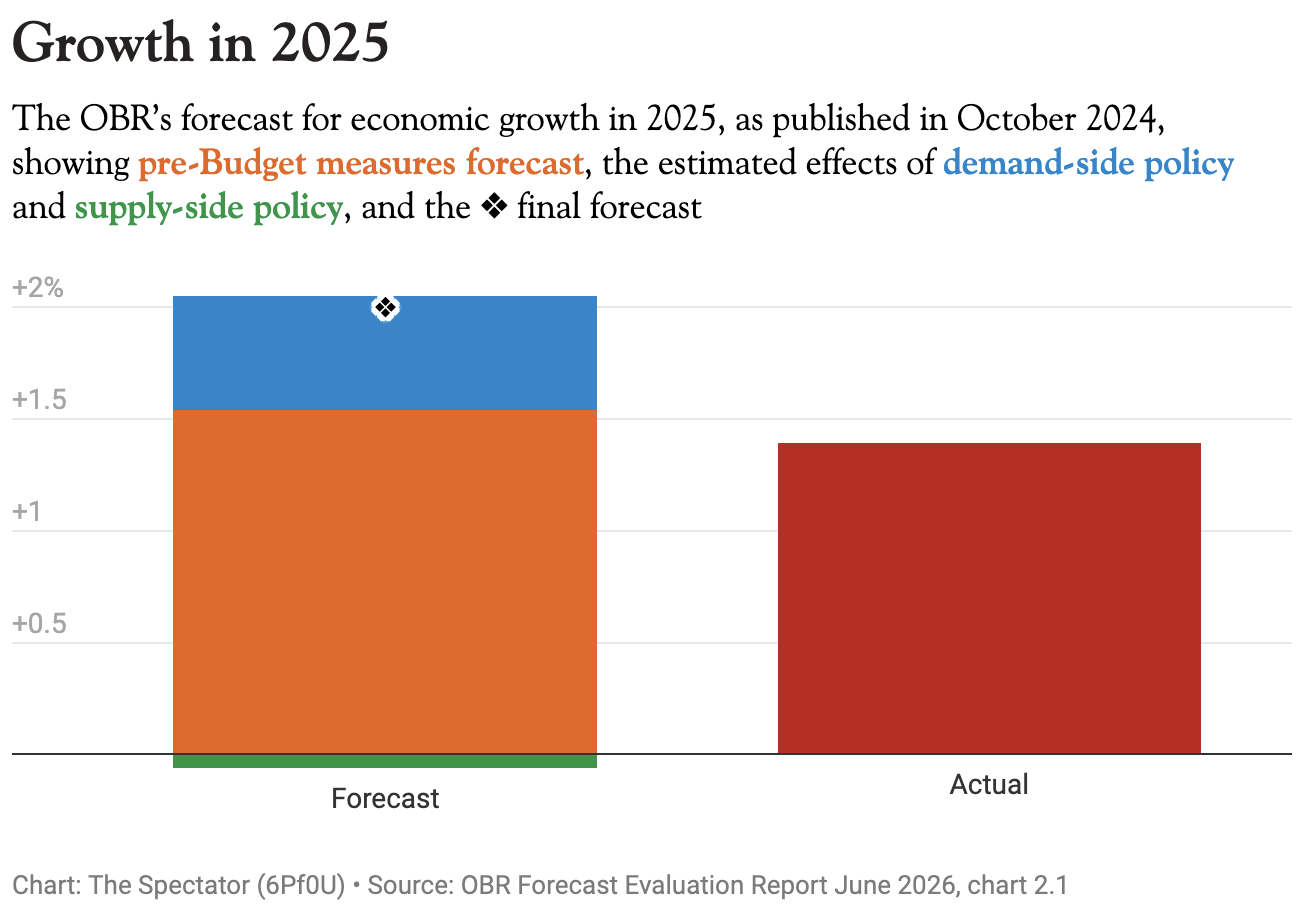

In the 2024 Budget, Reeves hiked spending by £60 billion and raised taxes by £25 billion in 2025-26. At the time, the OBR judged that the economy was close to capacity so more spending had limited scope to increase its size – but said the extra 1.2 per cent of GDP in borrowing would lift demand and GDP by 0.6 per cent in 2025-26, with the effect trailing off by 2030.

As the OBR observes, it’s hard to say definitively why GDP grew less than it expected

But in the end, the economy only grew by about as much as the forecast before accounting for policies announced in the Budget. As the OBR observes, it’s hard to say definitively why GDP grew less than it expected. Anticipation of Donald Trump’s tariffs could have pulled growth forward to 2024 as businesses stockpiled, which would mean slower growth in 2025. Anticipation of Labour’s spending spree might have caused a boost earlier too. And of course the OBR’s judgement of the effects of the Budget may have been wide of the mark.

The OBR says that:

Based on the outturn for 2025, it does, however, seem unlikely that the multipliers we used to assess the impact of the October 2024 policy package were too low and so underestimated the initial impact of the fiscal loosening on growth… This preliminary analysis, therefore, does not support the argument that we underestimated the short-run demand effect of the October 2024 fiscal loosening.

These short-term multipliers aren’t the full story – the OBR also comes up with estimates for the medium- and long-term effects of policies on the capacity of the economy. But they do say that, in the short term, it looks like the government can’t simply spend its way to growth.