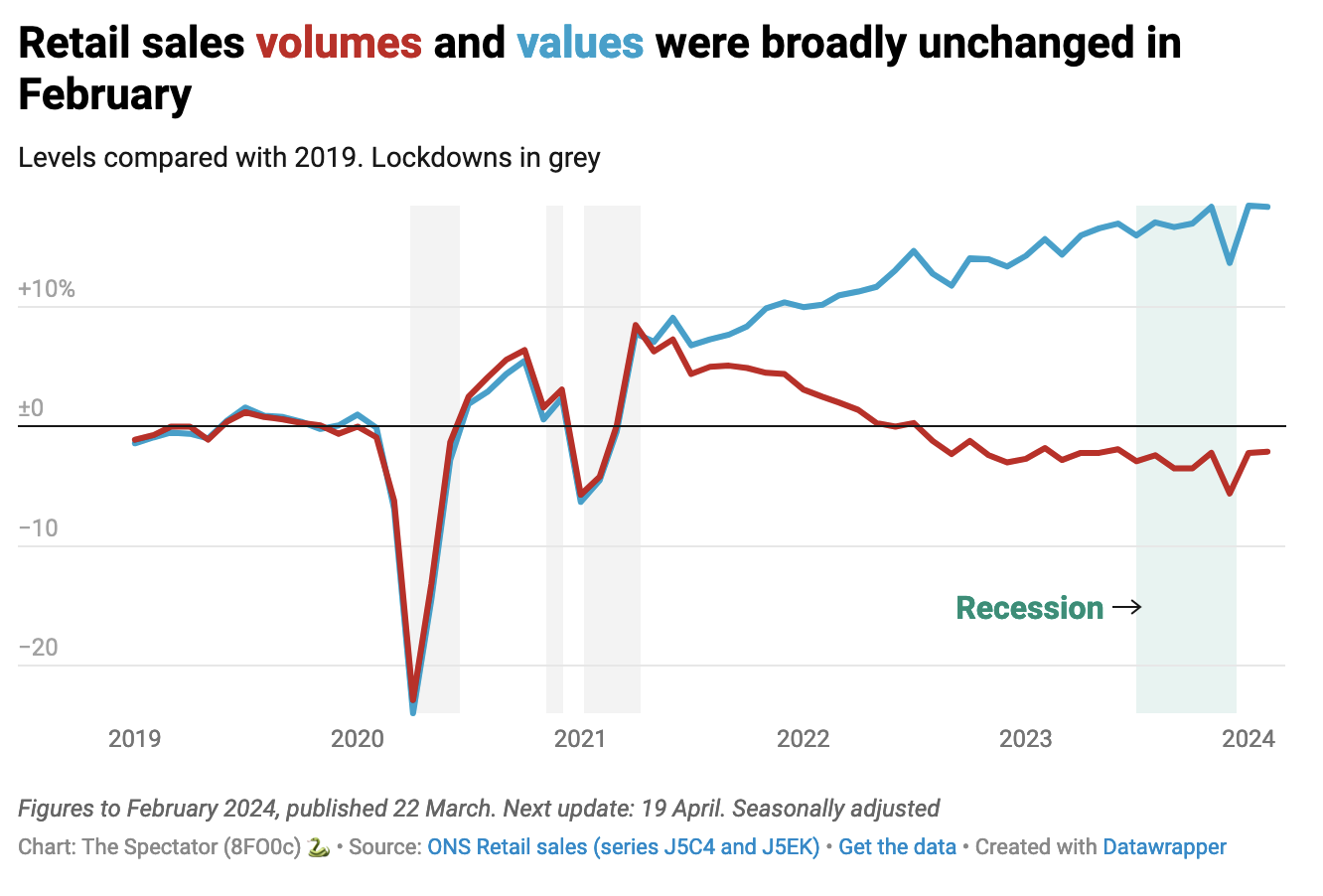

So, is the recession over? The Office for National Statistics’ (ONS) retail sales figures show that sales volumes were flat in February, when many expected them to fall. Moreover, the increase in sales volumes for January was revised upwards from 3.4 per cent to 3.6 per cent, coming on the back of a sharp fall in December (on seasonally-adjusted figures).

Clothing stores did better than most with sales volumes up 1.7 per cent in February. Household goods volumes were down 1 per cent – something which retailers apparently blamed on the poor weather – although it doesn’t make a lot of sense why we would feel happy going out in the rain to buy a new outfit but not a sofa or a bucket. The longer-term picture, however, is still one of mild recession: sales volumes in the three months to February were down 1 per cent on the same period a year earlier.

What is remarkable is how interest rates seem to be out of kilter with the economy. Normally, you might expect the Bank of England to lower rates during a recession in order to stimulate demand and then raise them again when economic activity picks up. This time around, the opposite applies. As demand seems to be picking up, the Bank is preparing to cut rates, with this decision perhaps coming as soon as June.

What is remarkable is how interest rates seem to be out of kilter with the economy

This rather underlines that the surge in inflation from late 2021 onwards was mostly a result of external factors, principally energy costs, rather than the result of an overheated economy. Retail prices were going up because input costs were rising, not because retailers and others sought to take advantage of strong demand in order to jack up prices and profits.

But if retail sales were to pick up substantially over the next few months, would the Bank of England be happy cutting rates in the late spring or early summer? The Monetary Policy Committee might start to interpret that as a sign of inflationary forces, and therefore be minded to hold rates a little longer. Stubbornly high earnings figures are what is keeping rates high for the moment. If the extra money flowing into consumers’ pockets starts to manifest itself in enhanced spending then that would emphasise the risk of cutting rates too early.

There is also the effect of Jeremy Hunt’s further 2p cut in National Insurance, introduced in the latest Budget, to sink in. Are people going to go out and spent that money (which would add to inflationary forces) or use it more to repair their battered finances, paying off debts and building up some savings (which might be a little more appreciated in Threadneedle Street)?

At the moment, no one can say we are exactly in boom conditions. Indeed, retail sales volumes are still lower than they were at the same time in 2019. That is a half-decade of reversal in sales. As far as retailers are concerned, Britain is not emerging from a brief recession which lasted two quarters – it is still stuck in a long-term recession