Has the Labour market cooled down enough for the Bank of England to change its mind on interest rates? Almost certainly not, based on the latest data from the Office for National Statistics, out this morning. The reintroduction of the Labour Force Survey data, which had to be suspended temporarily due to poor and limited feedback, has now been reinstated, showing fewer changes in the labour market than experts were hoping to see.

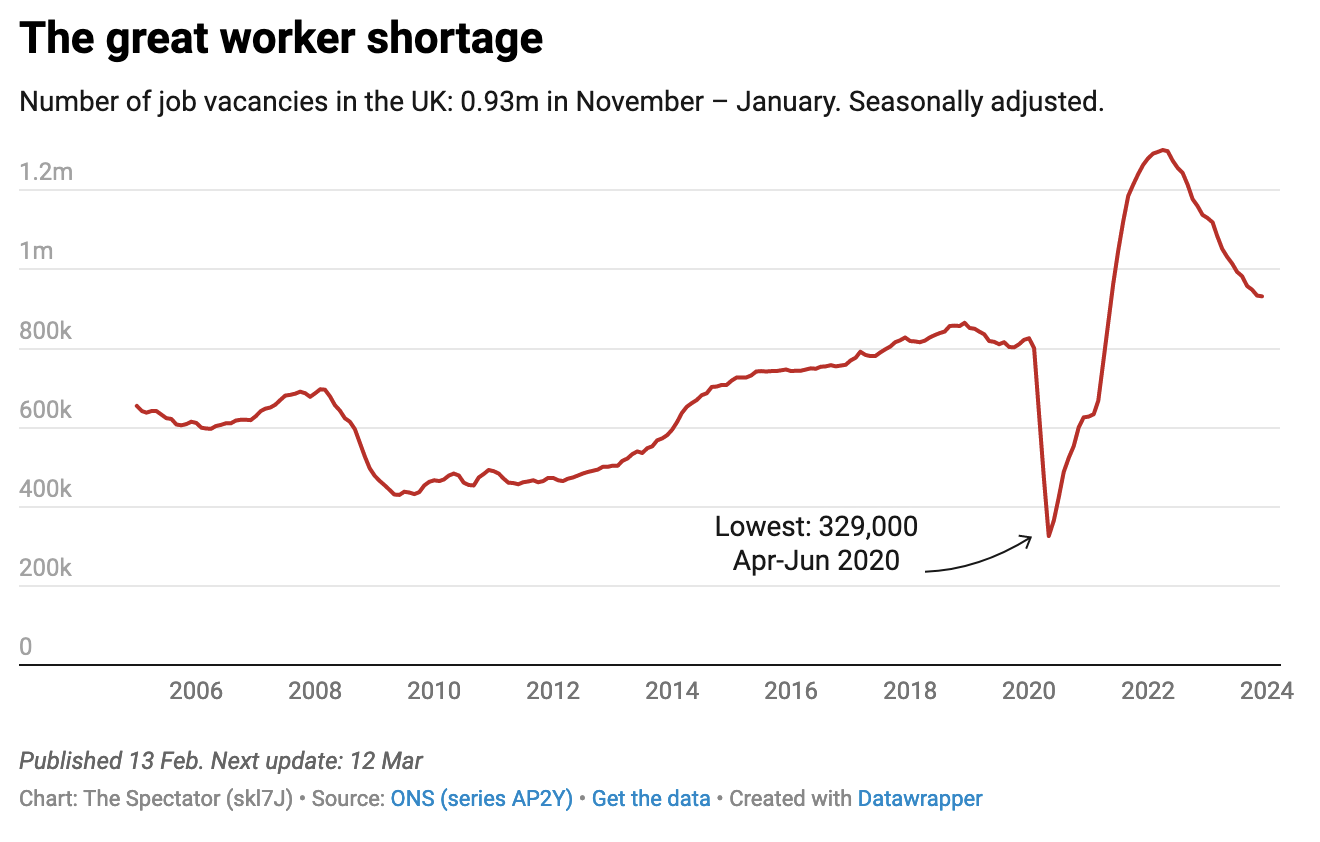

Job vacancies fell for the nineteenth consecutive time – but not by much. Vacancies were down to 932,000 on the quarter – a fall of 26,000, still well above pre-pandemic levels. Despite expectations that the unemployment rate would rise slightly, it fell again in the three months to December, from 3.9 per cent down to 3.8 per cent. These numbers are meant to be treated with ‘additional caution’ as the Labour Force Survey is still lacking critical data, but the evidence from the new reporting scheme continues to show signs of a tight labour market.

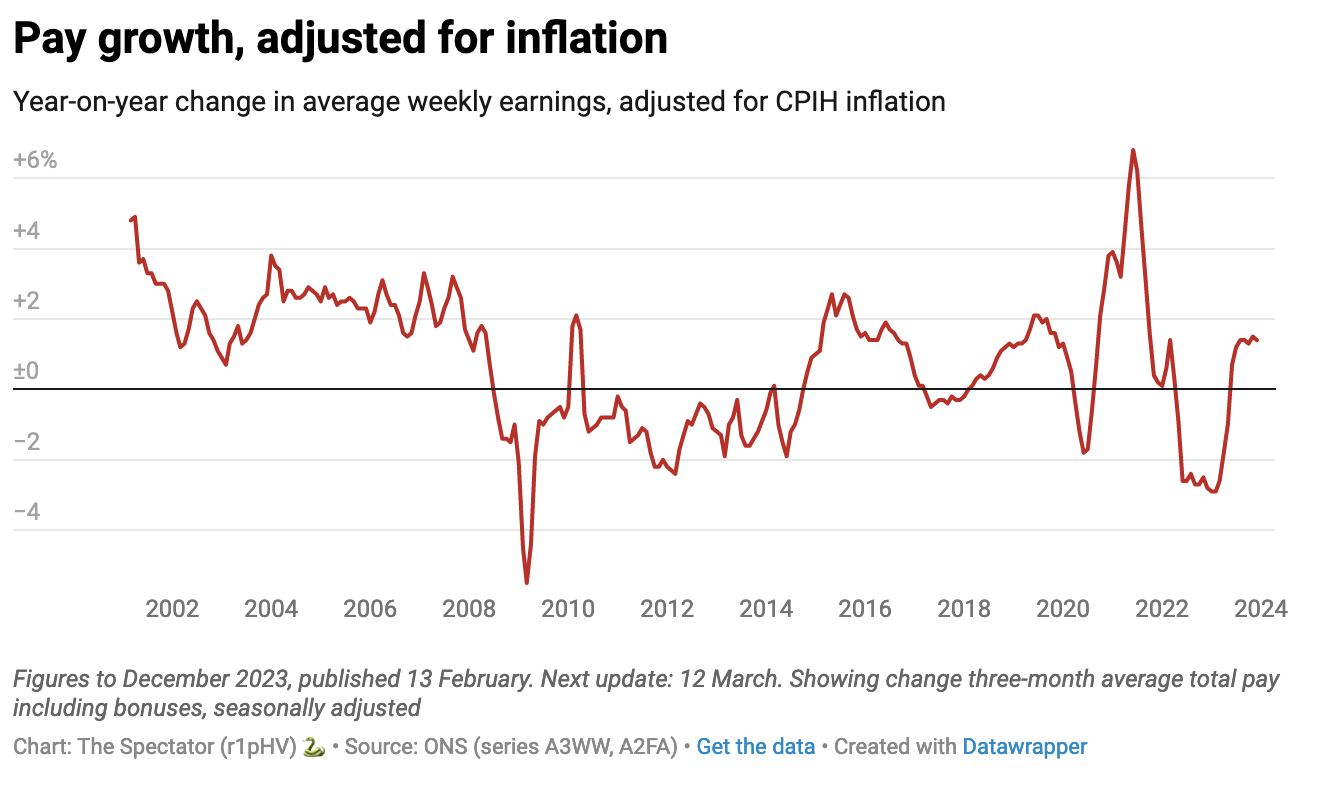

The most telling sign is wage growth, which has slowed, but not by as much as the Bank had predicted. Regular average earnings (excluding bonuses) fell from 6.6 per cent to 6.2 per cent, slightly above the Bank’s 6 per cent forecast. While wage growth fell behind the inflation rate for far longer than it outpaced it, the Bank still (controversially) considers this a key indicator of what’s driving price hikes in the UK.

Despite popular predictions that the inflation rate will fall substantially in April (when Ofgem lower the energy price cap and higher energy costs fall out of the data), it’s expected to be a rockier journey until then. All eyes are on tomorrow’s update, which could show the inflation rate drifting above 4 per cent before it comes back down again. The Bank is now estimating that a return to 2 per cent might only be fleeting, and strong wage data is going to keep its central bankers leaning in a hawkish direction, as they fear another round of domestic pressures fuelling inflation once again.

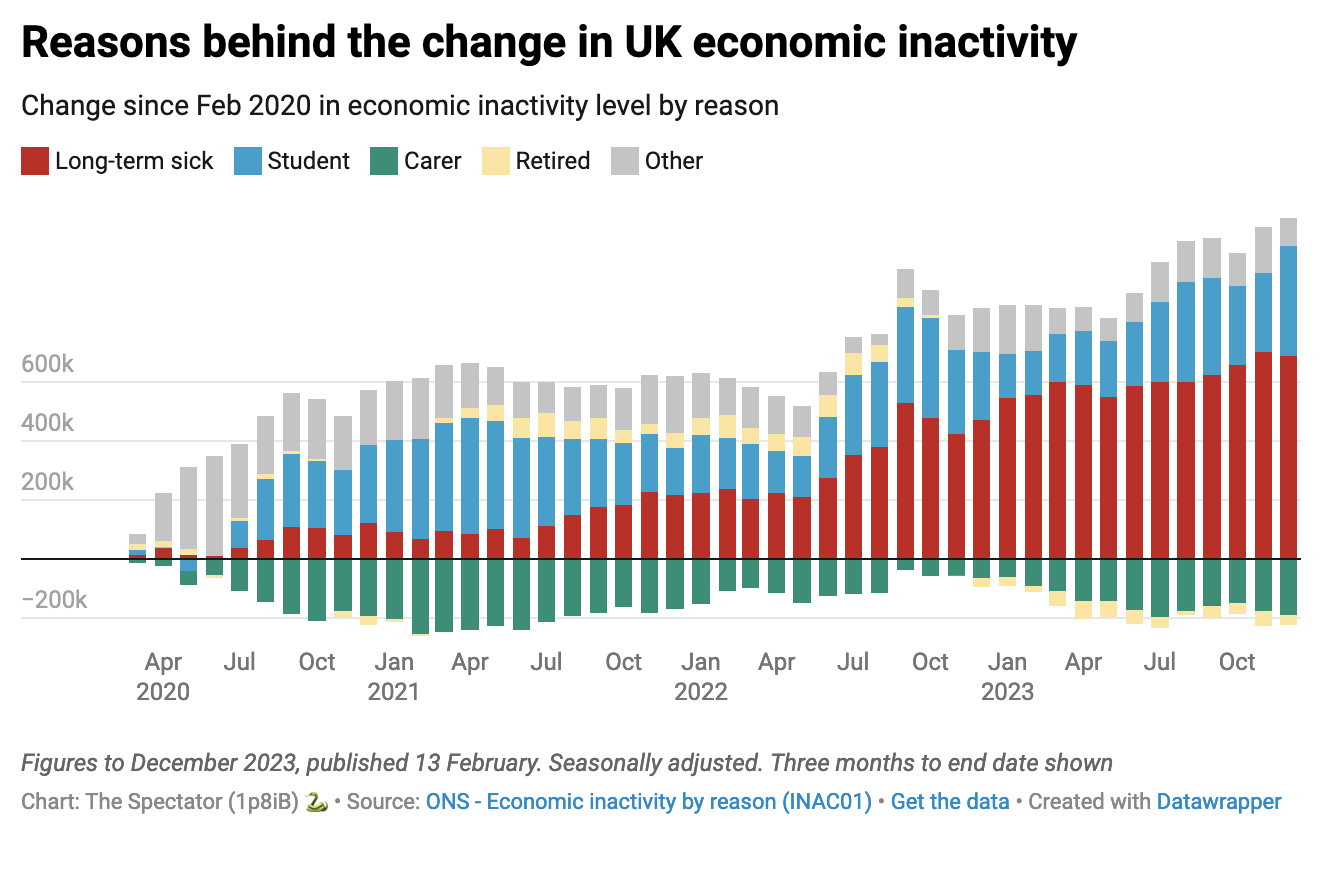

Meanwhile the economic inactivity rate for working-age people remained ‘largely unchanged’ at 21.9 per cent. This is a higher estimate than what was expected last year, driven by the historically high numbers of people on long-term sick leave. As Michael Simmons reported last week when the revised data was published, changes to the Labour Force Survey actually saw the estimates increase by a staggering 200,000, taking the total to 2.8 million. The ongoing combination of mass job vacancies and workers dealing with long-term conditions helps explain why, this morning, we also see foreign-born workers in the UK making up nearly 21 per cent of the UK’s workforce in the last quarter of 2023 – a rise from 18.1 per cent in the first quarter of 2020, when Britain formally left the European Union.

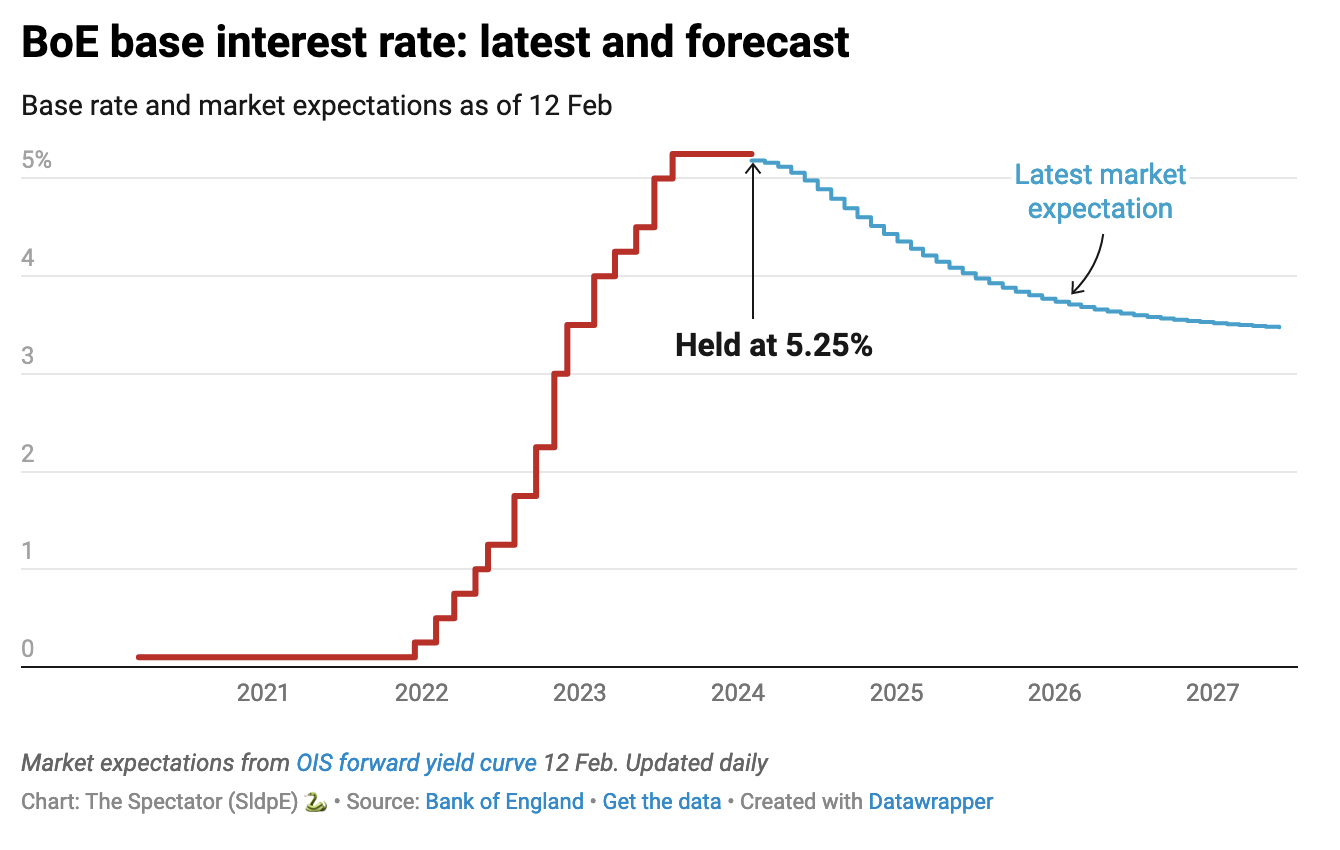

Most of today’s labour market data is headed in the direction the Bank needs to cut rates – but not nearly as quickly as many would like. Markets continue to expect some kind of reduction from where rates sit now – at 5.25 per cent – this year, but nothing spectacular. For as long as vacancies remain high and wage growth remains relatively strong, the Bank is likely to stick to its line that rates need to ‘remain restrictive for sufficiently long’ before a meaningful cut is made.