The government had been facing two economic challenges this week, ahead of the by-elections in Kingswood and Wellingborough: the publication of the latest inflation figures and the economic growth figures for the last quarter of 2023. It has just about survived the first challenge.

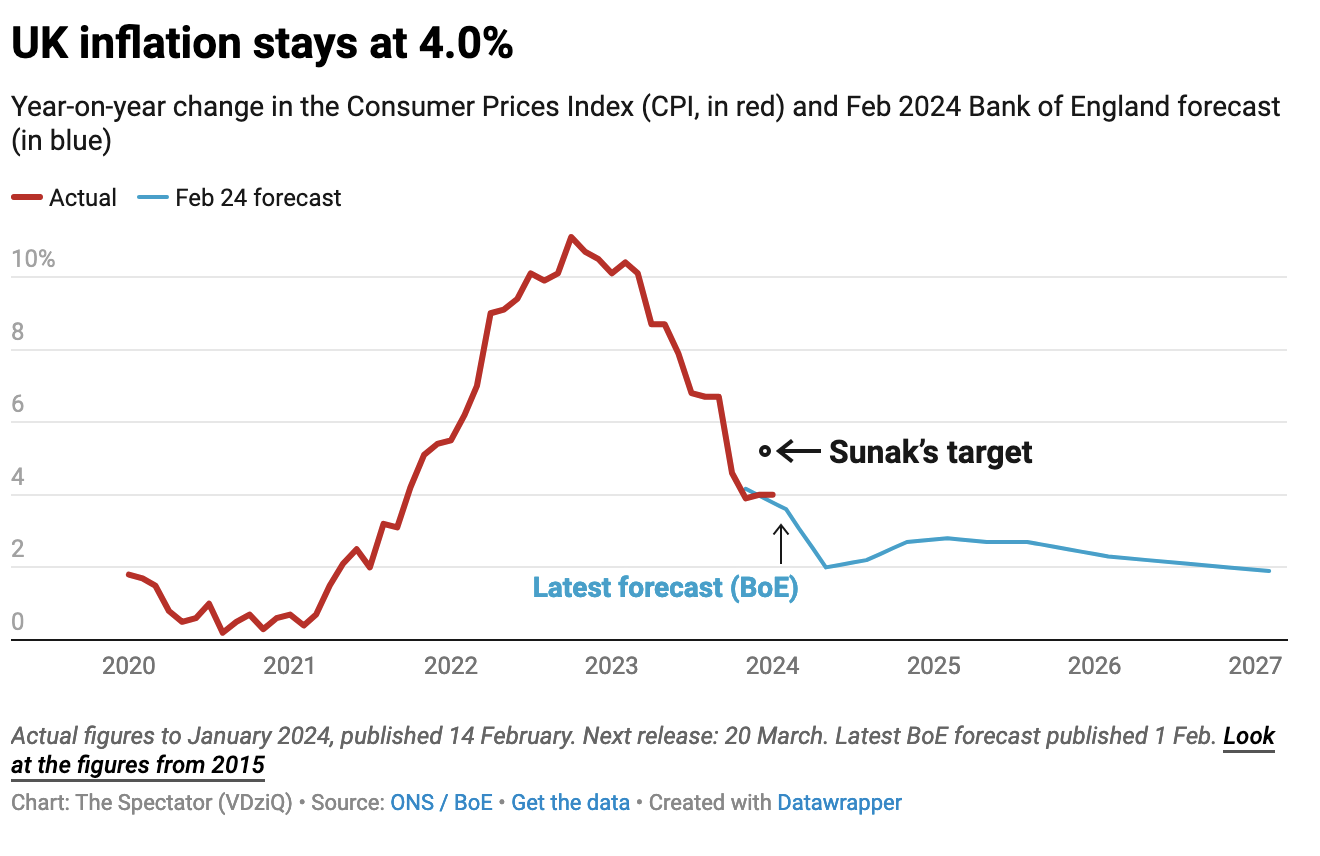

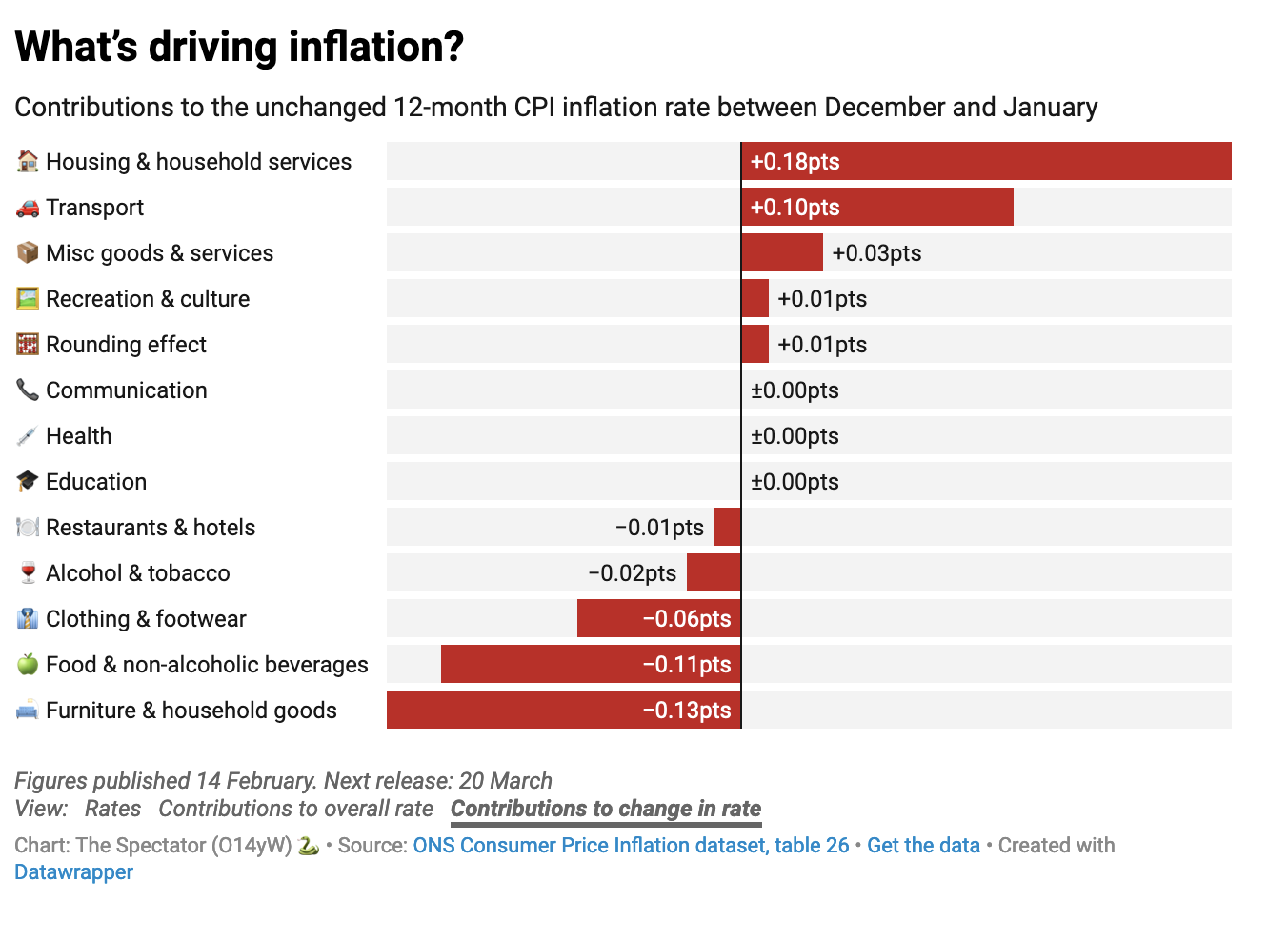

This morning’s update from the Office for National Statistics shows the inflation rate sticking at 4 per cent on the year in January, unchanged from December. This is still double the Bank of England’s inflation target, but it is better than expected news, as economists were predicting an uptick to 4.2 per cent. A combination of factors – including the January sales for home goods and furniture and another slowdown in food prices to 7 per cent on the year – managed to balance out energy price increases.

Moreover, worries about trade disruption in the Red Sea having a knock-on effect on prices seem to have softened, as rerouting shipments has not yet had a significant impact on the data. It’s a testament to what was learned during the Covid years – and the better ability to handle supply chain shake-ups when they occur – that prices have remained relatively stable.

The government will be benefiting this morning from low expectations. Over in the United States this week, inflation came in at almost one percentage point lower than the UK – 3.1 per cent on the year to January – but expectations had been for the rate to fall below 3 per cent, leading to slight panic and a narrative that inflation in America was hotter than expected. Contrast that to the UK, where a higher inflation rate now has the optimists asking again if the Bank of England will push forward its plans to cut rates.

It’s expected that by the time the Monetary Policy Committee meets again next month, inflation will have slowed once more, with February’s data expected to see inflation drop below 4 per cent again. The consensus, including from the Bank, is that inflation will return to 2 per cent in April, when Ofgem cuts the energy price cap significantly (Capital Economics is predicting a 10 per cent cut to utility bills) and the higher costs fall out of the data. But the Bank has made clear it’s looking for a ‘sustainable’ return to the inflation target, and with its own forecasts showing another uptick in inflation towards the end of the year (albeit nothing compared to what we’ve experienced the past two years), the MPC will remain cautious. Inflation sticking at 4 per cent in January is unlikely to sway the MPC that this alone allows for an early rate cut – especially not after yesterday’s labour market update, which continues to show wages outpacing inflation.

If there’s any data that’s going to put pressure on the Bank to cut rates early, it’s likely to be tomorrow’s news about economic growth. The second hurdle the government has to overcome this week may prove much tricker, as we are set to discover whether the UK entered a technical recession last year. After the growth figures from the third quarter of last year showed a 0.1 per cent contraction, the figures for the fourth quarter will tip the UK over to the right or wrong side of the line.

If the technical definition is met, it will be a very shallow and likely a short recession – but that will not be the takeaway for the by-elections, or indeed for the looming general election.

Even with inflation still not back to target, Rishi Sunak made good on his promise to ‘halve inflation’ by the end of last year. But even if he avoids a recession, his pledge to ‘grow the economy’ has certainly not come to fruition in the same way. Rather than being able to boast about any meaningful growth, ministers are crossing their fingers that tomorrow’s update will be positive. The data is at the margin – but the implications are huge.