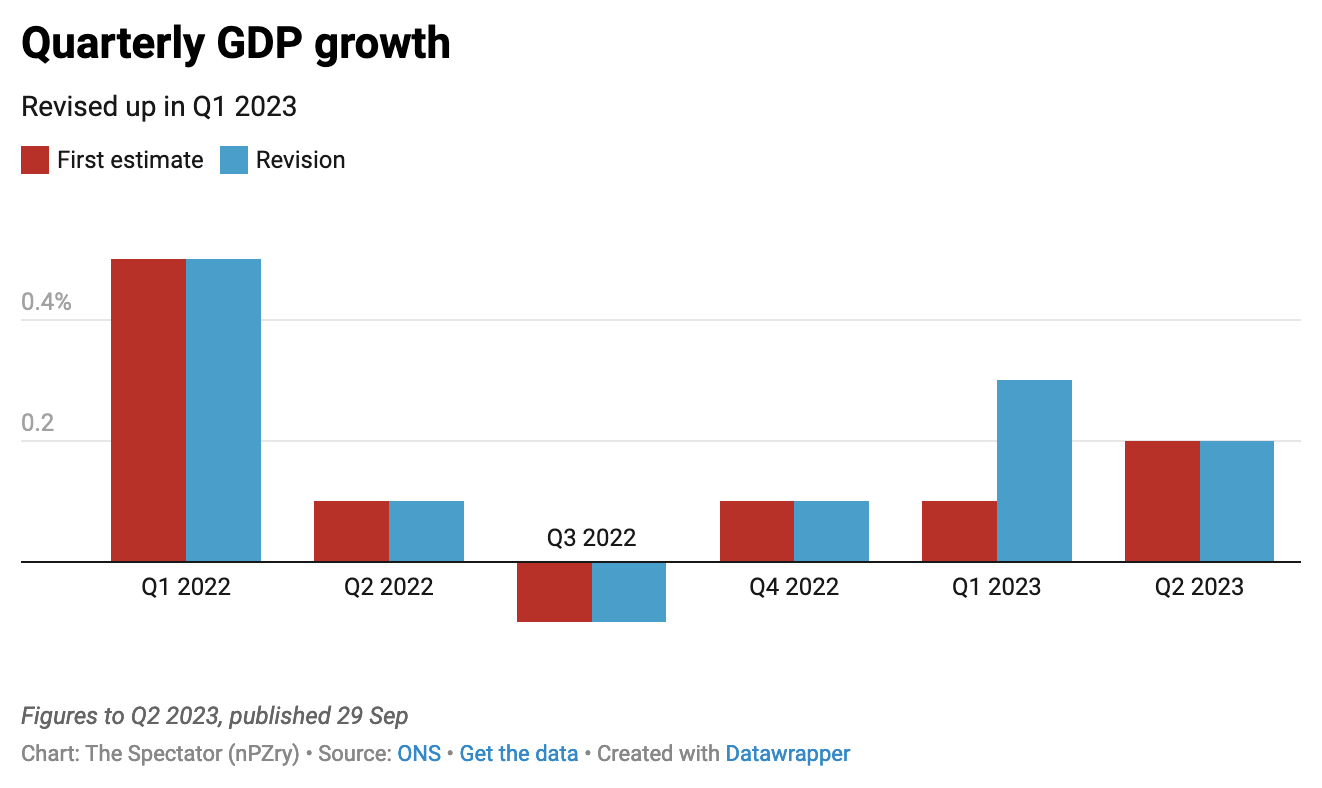

The Office for National Statistics has released the UK’s quarterly national accounts this morning, which show growth in the second quarter of the year remains unrevised at 0.2 per cent. Meanwhile growth in the first quarter has been revised slightly upwards, from 0.1 per cent to 0.3 per cent. This means the economy is now 1.8 per cent larger than it was before the pandemic hit.

This is another upward revision of growth figures, though much smaller compared to the update at the start of the month, which revealed the economy was not in fact still below its pre-pandemic levels, but had actually recovered by the time the Omicron variant hit in 2021.

This morning’s update will be considered good news: it now appears that the UK has rebounded faster from Covid than both France and Germany (today’s revision just edges France’s 1.7 per cent growth). The update also pushes away immediate fears of recession.

But this revision doesn’t change the overall picture of slow and limited growth. Capital Economics is still predicting hard times ahead – including a recession – as the growth stimulated in the first half of the year will be hard to repeat in the second (pointing to businesses bringing forward investment in 2023 due to the expiry of the super deduction allowance on 31 March).

Regardless of whether criteria for recession is ever technically met, economic indicators suggest the impact of fast-rising interest rates is starting to be felt across the economy – not least in the service industries. The last inflation update saw the annual rate for services slow from 7.4 per cent on the year in July to 6.8 per cent in August, while core inflation (which excludes food and energy), also slowed from 6.9 per cent on the year in July to 6.2 per cent in August. These are all signs that rates are finally taking some demand out of the economy.

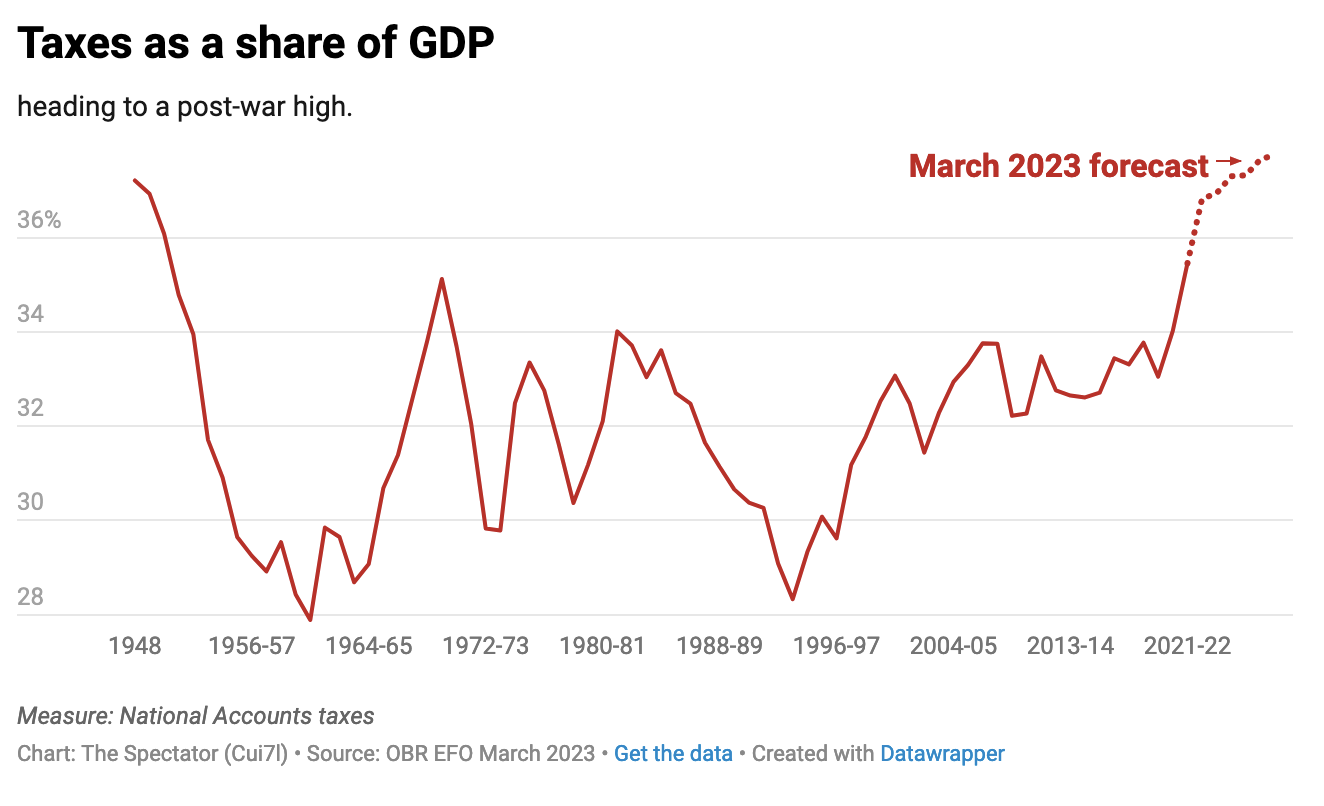

But that process includes a lot of pain, as costs rise for mortgage-holders and anyone with outstanding debt. It’s one of the many financial hits workers have had to withstand, in addition to wage rises falling well behind the rate of inflation for over a year and the tax burden getting even heavier.

Ahead of Conservative party conference, kicking off this Sunday, the Institute for Fiscal Studies is reminding the public just how much the Tories have added to that burden: ‘Over this parliament,’ its director Paul Johnson told BBC Radio 4 this morning, ‘it looks like taxes will rise by about 4 per cent of national income, that’s round about £100 billion.’

That the Tory party is taxing and spending at record levels is not new information. It was the tax hikes during Boris Johnson’s premiership that put the tax burden on track to reach a post-war high by the end of this parliament. Rishi Sunak’s government has since added to that burden; the latter out-taxing the former, and both taxing and spending at levels neither Tony Blair nor Gordon Brown would have dared attempt.

It’s not a reminder the Tories want shared going into their party conference, not least because they struggle to articulate how they might change course. Between lacklustre growth and many spending commitments, it’s near impossible right now to see where the Tories find the cash to meaningfully reduce that burden.