Inflation attracts metaphors. Especially popular is inflation as a genie, with attendant bottle in which it is either securely contained, or, worryingly, from which it has escaped. The Australian Financial Review reassured its readers in July 2021 that the ‘Inflation genie is not out of the bottle’, but in May the following year a clearly spooked Sydney Morning Herald warned that the RBA was ‘starting its chase of the inflation genie’. The Financial Review subsequently conceded that the genie had indeed left its bottle home and counselled that circus skills would be required to manage the wily spirit: ‘Inflation genie presents a juggling act,’ it reported, in July 2022. Now, one expects a rising tide to lift all boats, but Australia’s Future Fund is apparently less than buoyant. According to The Australian in May this year, it has been punished by a ‘rising tide of inflation’. And central bankers refer to ‘breakout inflation’ as if to an escaped man-eater, when it persistently exceeds their target range.

The language used by journalists, economists, and politicians to describe inflation tells us much about how it is widely understood. Inflation, it would seem, is a force of nature, or supernatural, even an Act of God, and it has something of the wild beast about it, hitherto safely enclosed, but now on the loose and a danger to all. But inflation is none of these things; it is entirely man-made; in essence simple to comprehend and therefore to control, at least in theory.

Inflation used to be defined as ‘too much money or credit’, in other words, an increase in the money supply in excess of the requirements of the economy. This, the classical definition, was one that dictionaries favoured as late as the 1970s. More recently, inflation has been redefined as ‘rising consumer prices’. The difference in the two definitions is fundamental because the current conception conveniently ignores what the classical view identified as inflation’s ultimate (as distinct from its proximate) causes. Ignoring its cause emboldens our rulers to create ever more inflation. Governments and central banks like the Reserve Bank of Australia don’t fight inflation. On the contrary, they create it.

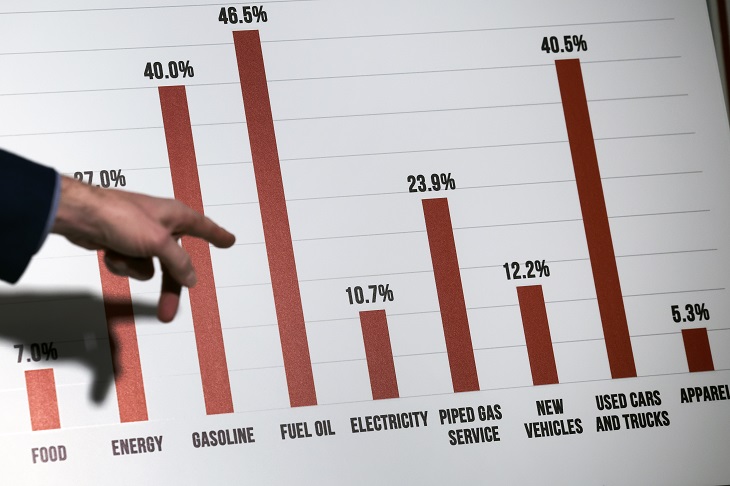

If we accept, for the sake of argument, the current, almost universally accepted definition of inflation as rising consumer prices as measured by the Consumer Price Index (CPI), its recent, or ‘proximate’, causes aren’t hard to identify: labour shortages, pent-up demand, and supply chain issues due to the pandemic, and the war in Ukraine, are amongst the more popular contemporary explanations. In an online article, What is inflation? What causes it? posted in June last year, the ABC attributed inflation to supply disruptions, wages growth, and growing global demand. ‘When demand outstrips supply,’ the article sagely reports, ‘issues start to emerge.’ Similar reasons for previous episodes of rapid CPI increases in the US such as that of the 1940s when the CPI rose over 19 per cent in one twelve-month period are put forward, for example by the American historian David Oshinsky: the ‘great inflation’ of that decade, he writes, was ‘triggered by supply chain shocks and compounded by the lifting of wage and price controls’. The distinguished economist, Alan Blinder, recently attributed the price inflation of the 60s, 70s, and 80s to food, energy, and deregulation. ‘These three shocks alone,’ Blinder says, ‘can account for all of the acceleration and deceleration of inflation in that period.’ These explanations all miss the forest for the trees, in other words, they fail to identify the ultimate source of rising prices.

According to the now-forgotten classical definition, and in Milton Friedman’s famous words, ‘Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.’ What causes inflation? Friedman stated, ‘There is one and only one basic cause: too high a rate of growth in the quantity of money.’

In a monetary regime of the kind that has existed since the first world war, the central bank is the primary creator of money (prior to the advent of the Reserve Bank of Australia in 1959, the Commonwealth Bank acted in this role). Consequently, it is the ultimate manufacturer of inflation. Those who need proof of this should acquaint themselves with the loss of the purchasing power of a dollar over the last 100 years, a time of enormous productivity growth in which, had the money supply not been hugely increased beyond that required, prices should have fallen, not risen. According to the RBA’s online inflation calculator, (you can check yourself), a basket of goods and services for which you paid $100 in 1966 would have set you back $1,384 in 2021. That is inflation and our central bank is responsible for it.

Rather than inflation as a force of nature, a mythical spirit, or an escaped carnivore, a bonfire makes a much more apposite metaphor: central banks, by vastly increasing the supply of money stack up the bundles of twigs in great number, but it is governments that strike the match, while the commercial banks eagerly pour on accelerate. Contemporary economic commentators overwhelmingly exonerate central banks and their monetary ‘stimulus’ as the primary manufacturers of inflation. They also largely – but not completely – excuse governments’ fiscal ‘stimulus’.

As the classical conception of inflation explains, central banks, government treasuries, and the private banking sector cooperate to create and then fan inflation. The central bank creates money and credits some portion of it to the treasury and another portion to private banks; the treasury, in turn spends the money and the banks lend it – and, in the process, demand rises relative to supply so lifting the CPI. Simon White (Inflation: A Play in Three Acts, Bloomberg Markets Live, August 11, 2022) puts it well: ‘Runaway inflation (like today’s) is almost always preceded by large government borrowing financed by the central bank.’

It’s important to note that the relationship between inflation’s cause and its economic consequences are complex. Hence the correspondence between profligate monetary and fiscal policy on the one hand and a rising CPI on the other is neither immediate nor automatic. To cite just two of many phenomena that have muddied the waters: periods of rapid technological advancement, if they reduce costs of production, can mitigate CPI’s rise; so can the entry into global markets of large quantities of raw materials and labour (which occurred in the wake of the Soviet Union’s collapse and China’s rise).

These two factors help to explain the CPI’s subdued pace (relative to the inflationary policies of those years) from the early-1990s to the global pandemic. While prices for consumer goods did not take off in those years, the excessive liquidity sloshing around the financial markets led directly to price inflation in the US real estate market, and when that bubble burst the world was plunged into the global financial crisis. The response of governments and central banks to the GFC? And how did they react to the coronavirus pandemic? They panicked – and unleashed an even bigger increase in the money supply and public sector spending!

What inflation isn’t is ‘too many dollars chasing too few goods’. It’s simply ‘too many dollars’; dollars created by central banks and subsequently spent and lent by governments and conventional banks. What the dollars chase is unpredictable. During the 30 or so years before the pandemic, they chased things like shares and houses. On Wall Street, such episodes are called ‘bull markets’. When, on the other hand, the surplus dollars chase consumer goods and services, as they did in the 1970s and again today, it’s called ‘inflation’. By the current definition – which today’s economics mainstream champions – central banks don’t create inflation: they combat it. According to the classical definition that today’s orthodoxy has forgotten, central and commercial banks seldom fight inflation. Quite the contrary: most of the time they are creating it. Like arsonists who join the bushfire brigade, central banks have created the very problem they purportedly seek to combat.

Chris Leithner’s most recent book is The Bourgeois Manifesto: the Robinson Crusoe ethic and the distemper of our times. He is the Managing Director of a Brisbane-based investment company.

Getty Images