The idea that we face a certain recession has been drummed into our heads for months. The Bank of England recently produced a graph showing recession lasting into 2024. Just yesterday, the International Monetary Fund repeated its assertion that Britain faces an especially gloomy 2023, with recession inevitable – while simultaneously upsetting the House of Commons Treasury select committee by refusing to testify before it.

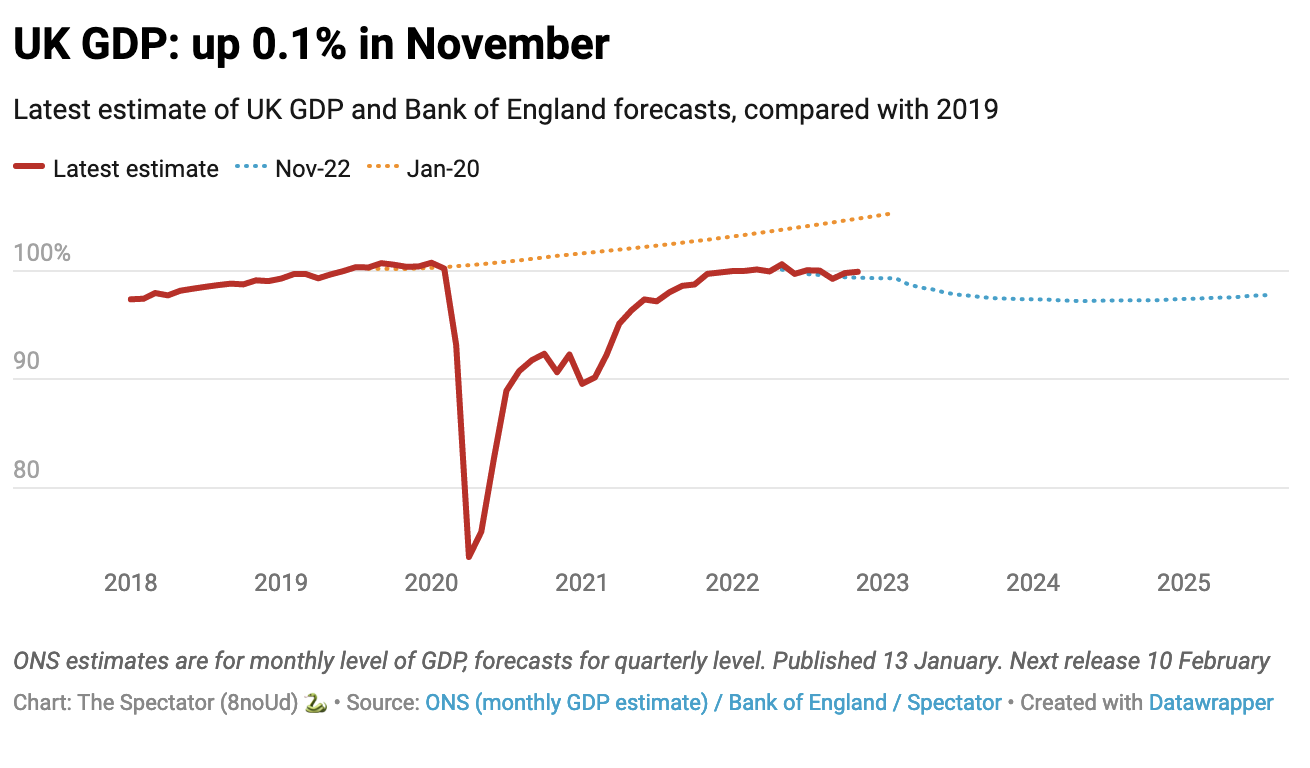

But could the unthinkable happen? Could Britain now avoid recession altogether? The Office of National Statistics’ (ONS) first estimate for economic growth for November shows that GDP grew by 0.1 per cent – unexciting, but still remarkable given that many economists were expecting negative growth by now.

A recession is defined as two consecutive quarters of negative growth. We have already had one of those – the third quarter of 2022. But for the fourth quarter to also come out negative, the economy will have had to have shrunk quite markedly in December. October showed growth of 0.5 per cent (which had a lot to do with the economy rebounding after a September with an unexpected bank holiday for the Queen’s funeral). Given that high street stores have been producing surprisingly upbeat reports for trading in December, this currently looks unlikely.

Could the unthinkable happen? Could Britain now avoid recession altogether?

Today’s figures must, however, be read with caution. They are just a first estimate: the ONS often revises them at a later date. In the second quarter of 2022, for example, there was a very significant change, with the ONS’s revised estimate rising from minus 0.2 per cent to plus 0.1 per cent. Moreover, the economy remains smaller that it was in January 2020 on the eve of the pandemic. Last May, GDP just about crept above pre-pandemic levels, but it was not to last: the economy is now 0.9 per cent smaller than it was then. The productive sector remains in recession, with output falling by 0.2 per cent in November. Moreover, when you take into account population growth of 0.3 to 0.4 per cent per year, the fall since 2020 equates to marked fall in output per head.

Yet there are reasons to look up. Energy prices are now falling sharply. Last August, one consultancy estimated that average household bills would rise to £7700 late this year. (The government’s Energy Price Guarantee later limited the tariff for gas and electricity to a level at which the average household would pay no more than £2,500 a year for the next 18 months).

But forecasts are looking more moderate by the day. Just last week, Investec estimated that average bills would fall to £2,640 by July. This week it has revised them further down to £2,478. Remarkably, this would be below the level of the Energy Price Guarantee. A policy which once threatened to cost the government over £100 billion may, by the middle of the year, be costing it nothing at all.

The good news for households is that the Energy Price Guarantee does not fix bills at £2,500 a year – should the energy price cap fall below £2,500 a year, consumers will benefit. With falling energy prices, we ought to soon see a sliding Consumer Prices Index, though we will have to wait until next week for December’s figures.