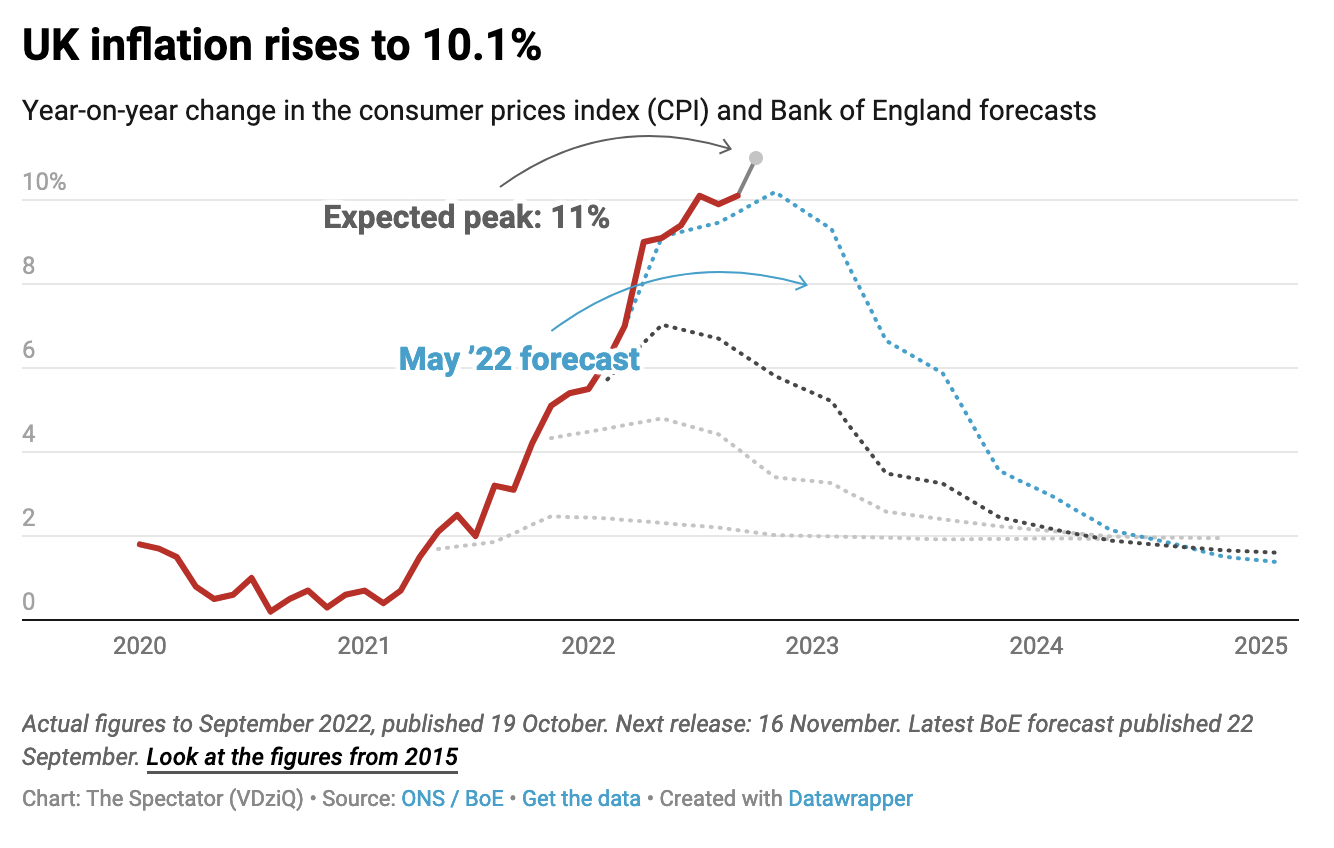

In all the recent economic chaos, it’s been easy to overlook one of the most important factors contributing to the cost-of-living crisis: inflation. But this morning’s update from the Office for National Statistics brings it back into focus, as CPI inflation rose back into double digits in September: now at 10.1 per cent on the year, compared to 9.9 per cent in August.

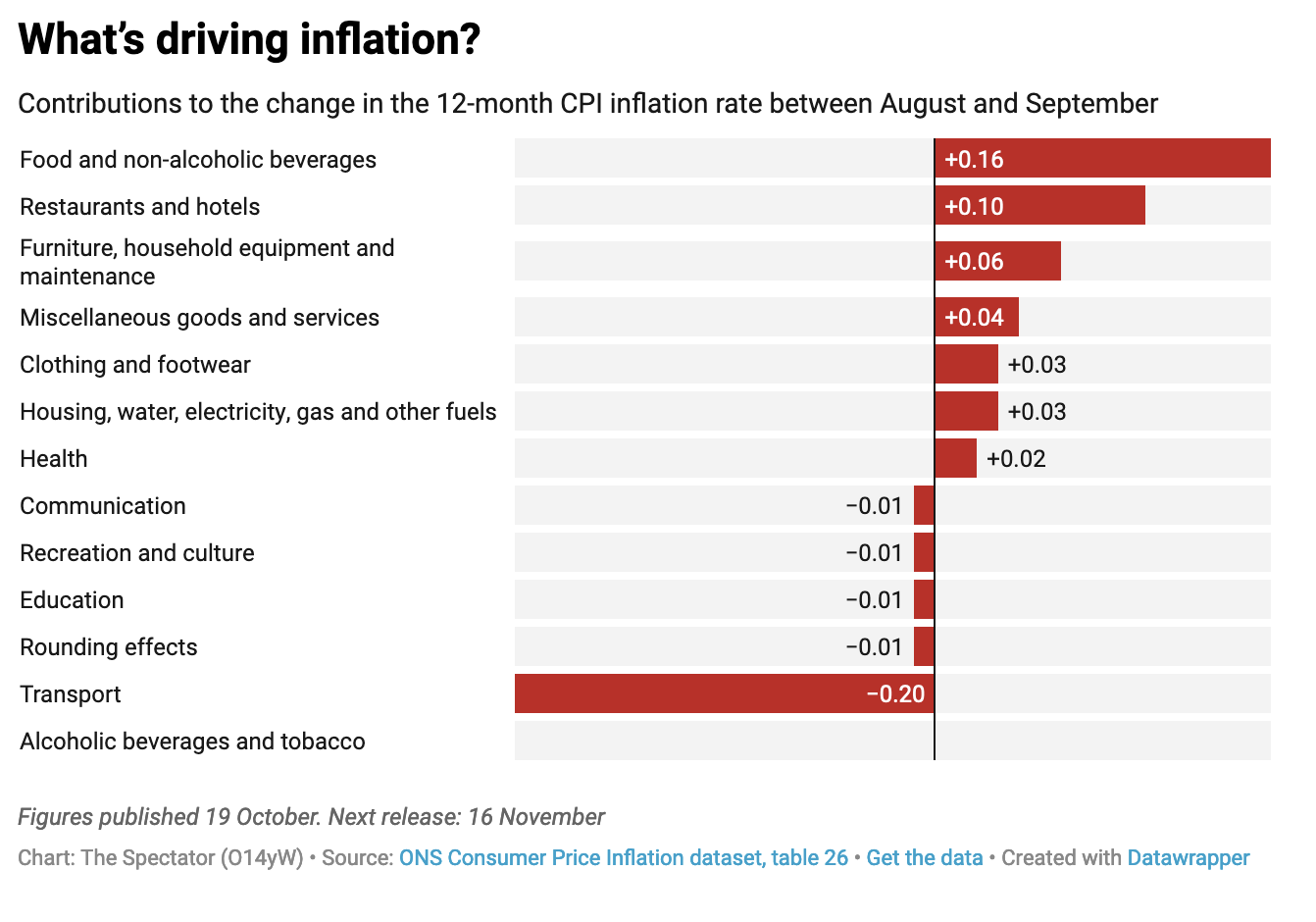

Another uplift was expected, but inflation has still risen higher than the broad consensus of 10 per cent. A weak pound hasn’t helped: sterling’s plunge against the dollar over the past few months has increased the costs of importing goods, especially food, which according to the ONS made the ‘largest upward contribution’ to headline inflation figures last month.

It’s a reminder that energy costs – while a huge part of this story – are not the only factor contributing to higher prices. This casts doubts on the more optimistic forecasts for inflation, that we have roughly reached the peak for price hikes, as the government’s energy price guarantee kicks in from October, capping average household energy bills at around £2,500. But the fall in energy costs last month – mainly the price of motor fuels – was not enough to offset the rise in housing costs, household services, food and non-alcoholic beverages: necessary goods which do not have a scheme in place this winter to stop prices from rising.

It’s a reminder that energy costs – while a huge part of this story – are not the only factor contributing to higher prices. This casts doubts on the more optimistic forecasts for inflation, that we have roughly reached the peak for price hikes, as the government’s energy price guarantee kicks in from October, capping average household energy bills at around £2,500. But the fall in energy costs last month – mainly the price of motor fuels – was not enough to offset the rise in housing costs, household services, food and non-alcoholic beverages: necessary goods which do not have a scheme in place this winter to stop prices from rising.

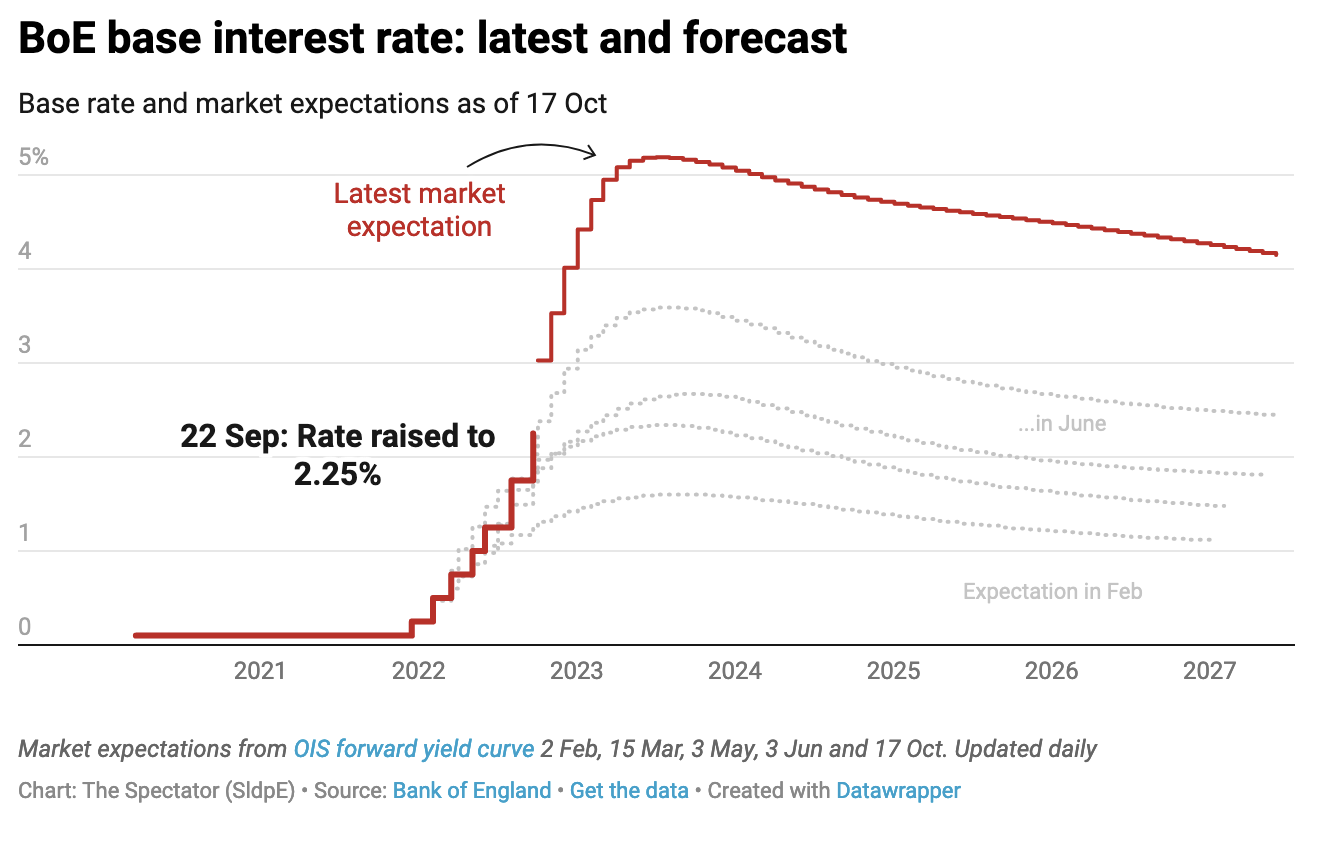

It’s becoming increasingly difficult to chart how high prices might go, as the mechanisms for controlling them – mainly the Bank of England raising interest rates – have become muddled in the recent economic crises created in parliament. Up until the end of last month, the goal had been to loosen fiscal policy in a bid to give the Bank space to tighten monetary policy and raise rates further. But the blow-up from the mini-Budget and rapid rise of market expectations for interest rates now see the new Chancellor Jeremy Hunt rolling back as much of that loosening as he can; over-correcting with very tight policy (i.e. tax increases and soon-to-be-announced spending cuts) in a hope that the Bank can keep rates lower (a bid to salvage people’s mortgage payments). Hunt is also trying to make sure the Bank does not have to move so quickly (the next rate decision is in early November) that any rate rise outpaces what the markets expect.

Meanwhile, the decision to reduce the timeline of the energy price guarantee from two years to six months – expected to be replaced with a more targeted scheme for vulnerable households – is likely to save the taxpayer quite a bit of money but casts further doubt on the hopes that inflation has peaked. The guarantee was estimated by government to have reduced peak inflation by four to five percentage points.

Meanwhile, the decision to reduce the timeline of the energy price guarantee from two years to six months – expected to be replaced with a more targeted scheme for vulnerable households – is likely to save the taxpayer quite a bit of money but casts further doubt on the hopes that inflation has peaked. The guarantee was estimated by government to have reduced peak inflation by four to five percentage points.

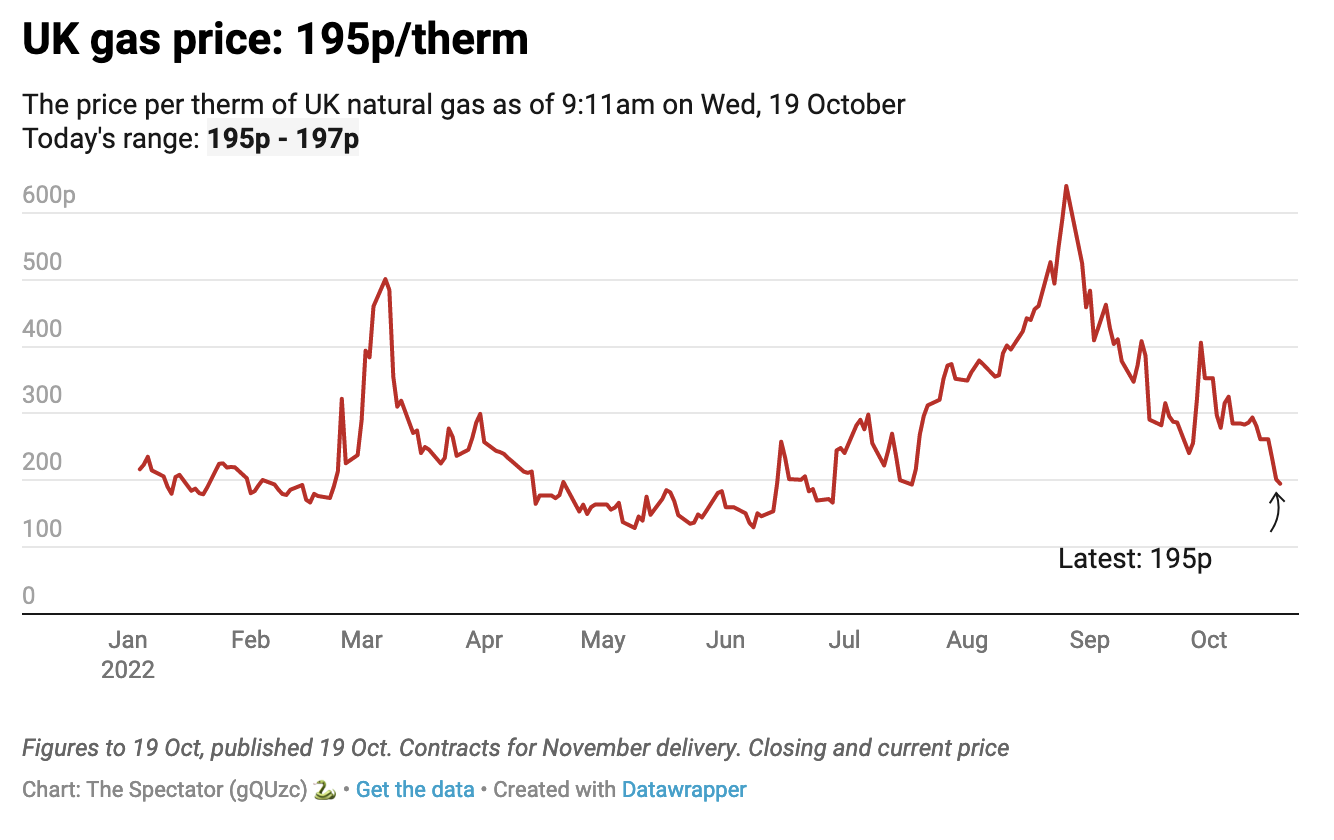

While gas prices in the UK have now fallen to a three-month low, it is difficult to say how quickly those prices will filter through to energy bills. If these lower prices stick, they may offset price rises come April; but it’s also possible the removal of the guarantee will push prices up again next spring.

Or even, perhaps, before then. October’s figures will show the cost of energy for households rising from £1,971 (Ofgem’s last price cap) to the £2,500 cap now set by government ministers. Capital Economics already forecasts the headline rate to rise to 10.5 per cent next month. The inflation saga is far from over.

Or even, perhaps, before then. October’s figures will show the cost of energy for households rising from £1,971 (Ofgem’s last price cap) to the £2,500 cap now set by government ministers. Capital Economics already forecasts the headline rate to rise to 10.5 per cent next month. The inflation saga is far from over.