The Big Short is a drama about the American financial collapse of 2008. It talks you through sub-prime mortgages, tranches, credit-default swaps, mortgage-backed securities, collateralized debt obligations …and, yes, I just bored myself to tears typing that list. I had to prop my eyes open with matchsticks typing that list. I would even propose that I was more bored typing that list than I’ve ever been in my whole life, which is saying something, as I saw Monuments Men. And, previously, I would have proposed that there is no way you could ever make any of the above fascinating or compelling or sexy, let alone scathingly funny. But The Big Short is fascinating, sexy, compelling and scathingly funny. It’s a miracle. It’s a lesson to The Revenant; a lesson that says: hey, dude, did you know that in the right hands a bear market can be more exciting than an actual bear? Did you?

It is directed and written by Adam McKay, who has made countless comedies with Will Ferrell (Anchorman, Talladega Nights, etc.) but that’s OK, because I have a fondness for Will Ferrell comedies, which are often more intelligent than they seem. This is an adaptation of the 2010 non-fiction book by Michael Lewis, which followed the handful of Wall Streeters who saw where the American economy was going, and heard the apocalyptic trumpets way before anyone else did. They’re the ones who spotted the sub-prime debt (look!; look how I’m familiar with all these words now!) and bet against the housing market — I think you’ll find this is known as ‘shorting’ — and they’re the ones who made a ton of money. They’re the winners. I suppose. Kind of. If there are any winners. There are certainly no heroes. That is made abundantly clear.

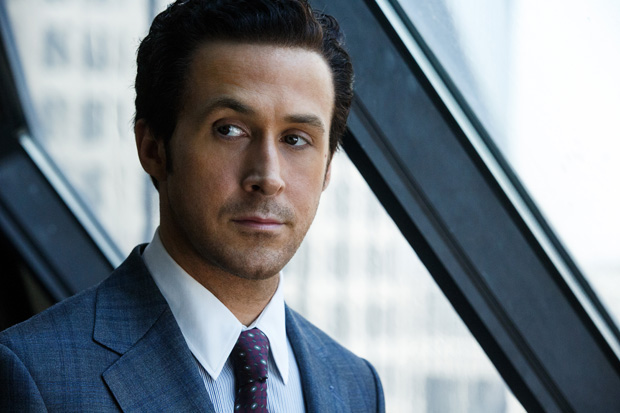

These individuals did not know each other, and never met, so we follow their stories individually. You have to know who they are, so let’s get this over with quickly. There is Michael Burry (Christian Bale), a one-eyed hedge-fund manager who has Asperger’s and is into heavy metal. There is Jared Vennett (Ryan Gosling), an ambitious young gun who can smell money on entering a room and who tips off another hedge-fund manager, Mark Baum (Steve Carell, wearing a wig of Ron Burgundy-level terribleness). And, lastly, it’s two wet-behind-the-ear chaps from Colorado (John Magaro, Finn Wittrock) who are mentored by a retired Wall Street tycoon (Brad Pitt, at his most Robert Refordish; I would even moot that Brad Pitt is better at doing mid-life Robert Redford than Robert Redford ever was).

The Big Short isn’t Wolf of Wall Street. This isn’t about the culture of excess and those cocaine-fuelled parties, although there is some of that. And this isn’t 99 Homes, as it’s not about the human cost, although there is also some of that. Instead, this wants us to understand what happened and why, which is a tall order. It knows it is a tall order. It knows it has to be outrageously entertaining, or die, and it is outrageously entertaining. It is snappy. It uses montage, irony and popular culture references. The script is great. Here is a character’s first impression of a banking conference in Las Vegas: ‘It’s like someone hit a piñata full of white people who suck at golf.’ And one conceit has Jared addressing us directly, with teasing acknowledgments along the lines of ‘Yes, we know you don’t understand it. No one does. So here’s Margot Robbie in a bubble bath to explain’, and, blow me, if we don’t then cut directly to Margot Robbie in a bubble bath, explaining sub-prime lending. So, so clever.

And it doesn’t matter if you don’t understand much — I probably didn’t understand that much — as it works anyhow, and you’ll still get, for instance, why Goldman Sachs thinks Burry is insane for wanting to bet against housing, and why they laugh at him while still being prepared to do business with him. You’ll get, too, Baum’s mounting sense of horror as he begins to realise the rating agencies are in the bank’s pockets. And you’ll get how all these complex financial tools were devised to keep the rich rich while screwing over the little guy, particularly when Baum takes a trip to Florida to check out the sub-prime market for himself, and discovers deserted properties, tenants still paying rent to landlords even though the landlords are no longer paying the mortgages, corrupt realtors signing up immigrants who don’t know what they’re signing for and also (because McKay has a terrific sense of the absurd) an alligator that will take you rather by surprise.

This is one of those films that keeps you interested in a subject you imagined you had no interest in. It is improbably compelling, while the performances (especially Bale and Carell) are smoking hot. Plus, it will fill you with a righteous anger. Although the behaviour of the banks was criminally outrageous, and led to ordinary people’s lives being ruined, only one banker ever went to prison, and now it’s back to business as usual, or so it would appear …oh God, it sounds so boring on paper, but here’s a plan: just go see it. And go see it now.

Got something to add? Join the discussion and comment below.

You might disagree with half of it, but you’ll enjoy reading all of it. Try your first month for free, then just $2 a week for the remainder of your first year.