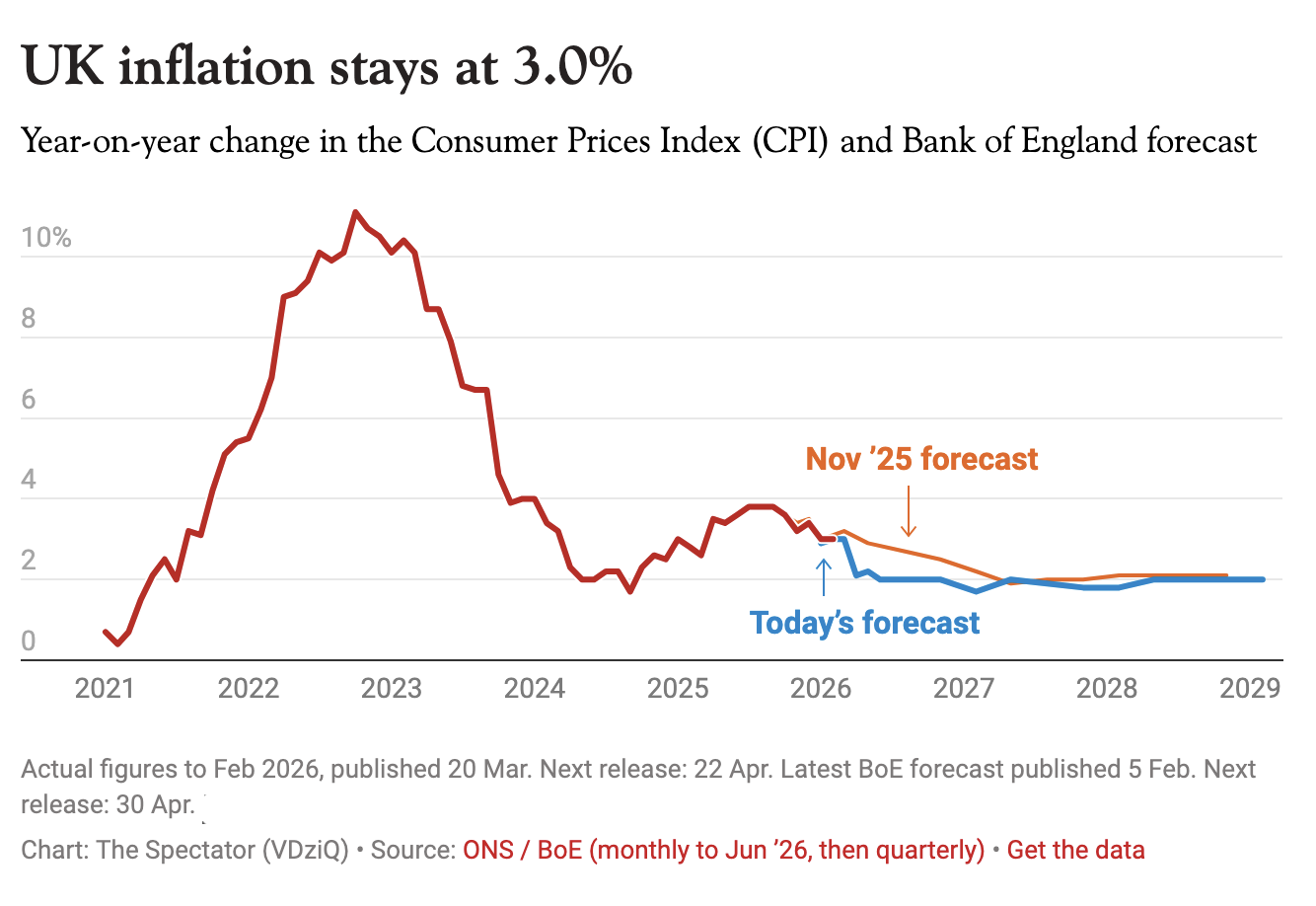

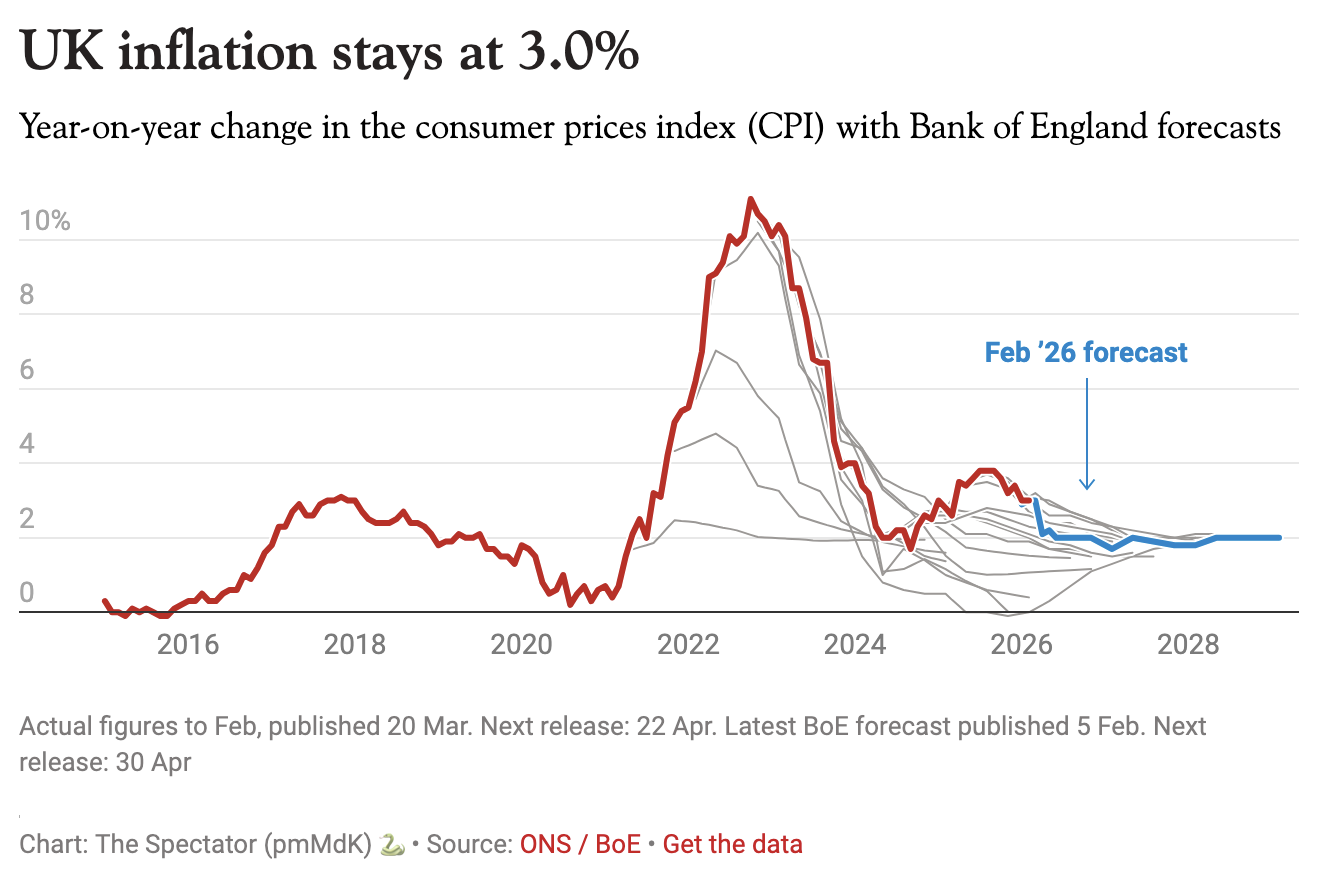

Prices rose by 3 per cent last month – the same rate as the month before. Figures just released by the Office for National Statistics (ONS) show that – ironically – falling petrol costs were one of the main things keeping the Consumer Prices Index (CPI) from climbing. This data was, of course, collected before the latest conflict in the Middle East – and we can soon expect the numbers to start heading in the wrong direction.

Figures from 2020

Figures from 2015

Elsewhere, clothing costs were the largest upward driver of inflation, while food inflation remained broadly flat. In good news for drinkers, the cost of alcohol came down thanks to increased promotional activity in February.

In a different world, the government would be cautiously welcoming today’s figures. But in the one we live in, they are, unfortunately, already outdated.

Since they were recorded, America and Israel’s war against Iran has sent global energy prices skywards, meaning increased UK inflation is unavoidable. As things stand, some economists are predicting inflation will head north of 5 per cent this year.

Worse still, we will be entering this crisis with the highest inflation of the developed G7 countries. Core inflation – which strips out more volatile prices – climbed to 3.2 per cent as well. The Chancellor bears a lot of the responsibility for that, given her employment policies and National Insurance tax raid have clearly been passed on to prices.

As for what happens next, the outlook is pretty bleak. The slowdown in oil supply, for example, has not actually spread to much of the West yet, meaning that the worst effects of the energy shock have not yet reached our shores. ‘With energy facilities severely damaged and production grinding to a halt across the Middle East, there is now a long-term, structural supply-side issue in the energy market. Even if the war was to stop today, the damage has been done and long-term implications are inevitable,’ said Joe Nellis, economic adviser at MHA.

All eyes are now on Threadneedle Street, where the Bank of England’s Monetary Policy Committee shocked markets last week with a unanimous nine–zero vote to hold interest rates at 3.75 per cent. Usually, the MPC doesn’t respond to energy price shocks, so bank watchers were surprised when every committee member turned hawkish – a vibe shift that was more extreme than in other central banks.

The MPC’s move sent gilt yields soaring on Friday and saw swap markets pricing in four interest rate cuts. Since then, we have had trickled-out briefings from the Bank suggesting that the market has misread its signals, with some traders critical of its communication strategy. It may be that they were signalling a year of interest rate holds rather than hikes, but that will come as little comfort for most. Certainly, if the predictions of 5 per cent-plus inflation hold true, then the Bank has made it clear it will do what is necessary – i.e. hike rates – to keep on top of it.

The net effect of all this – even higher borrowing costs for Britain – underscores why the Chancellor was right yesterday to make clear any energy bills bailout will be ‘targeted’ and ‘funded’. It was Liz Truss’s energy price guarantee that sent markets berserk and brought down her government, as Ross Clark explained to me on this week’s Reality Check. Reeves might be responsible for how unprepared we are going into this next crisis, but she is taking the right approach now.