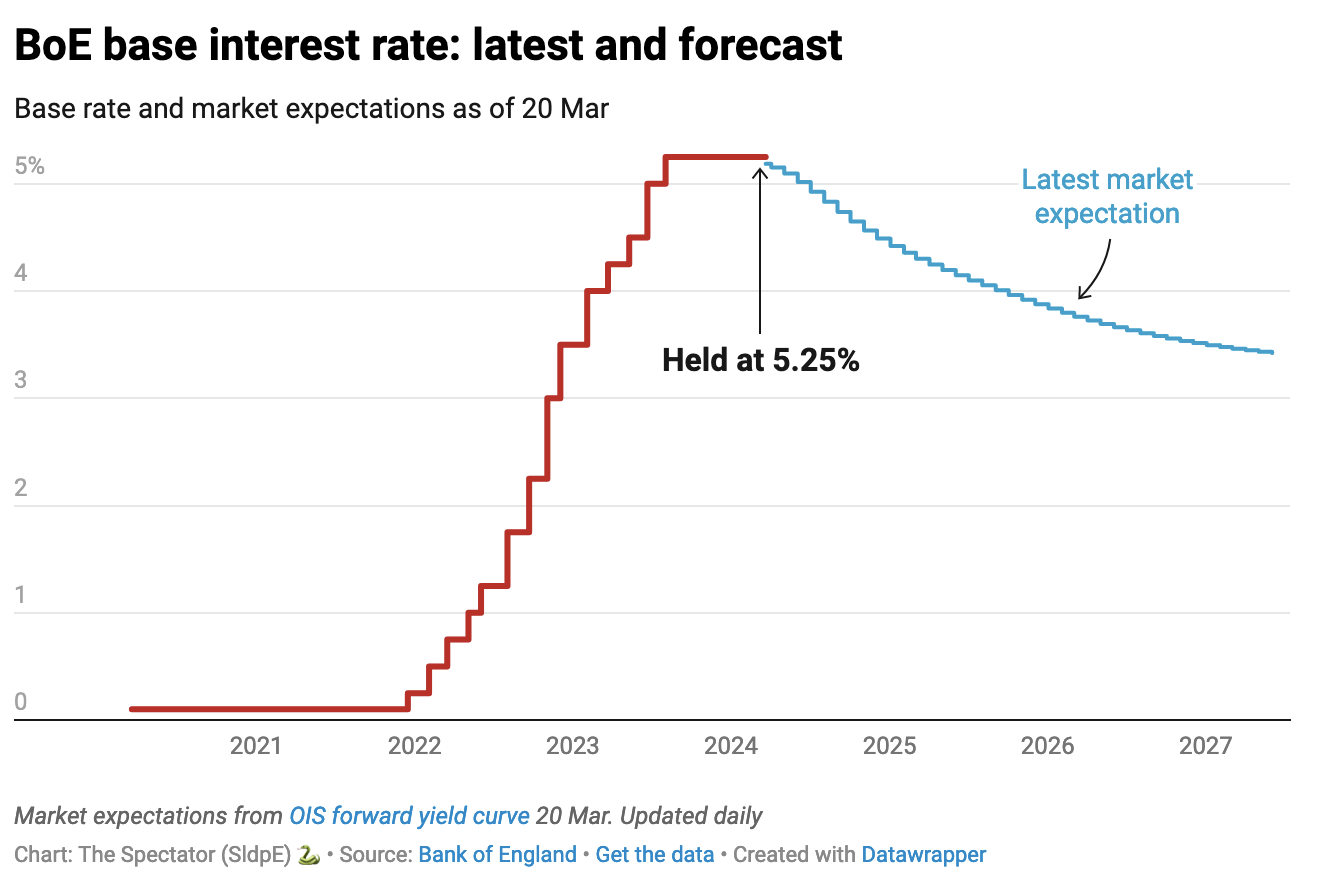

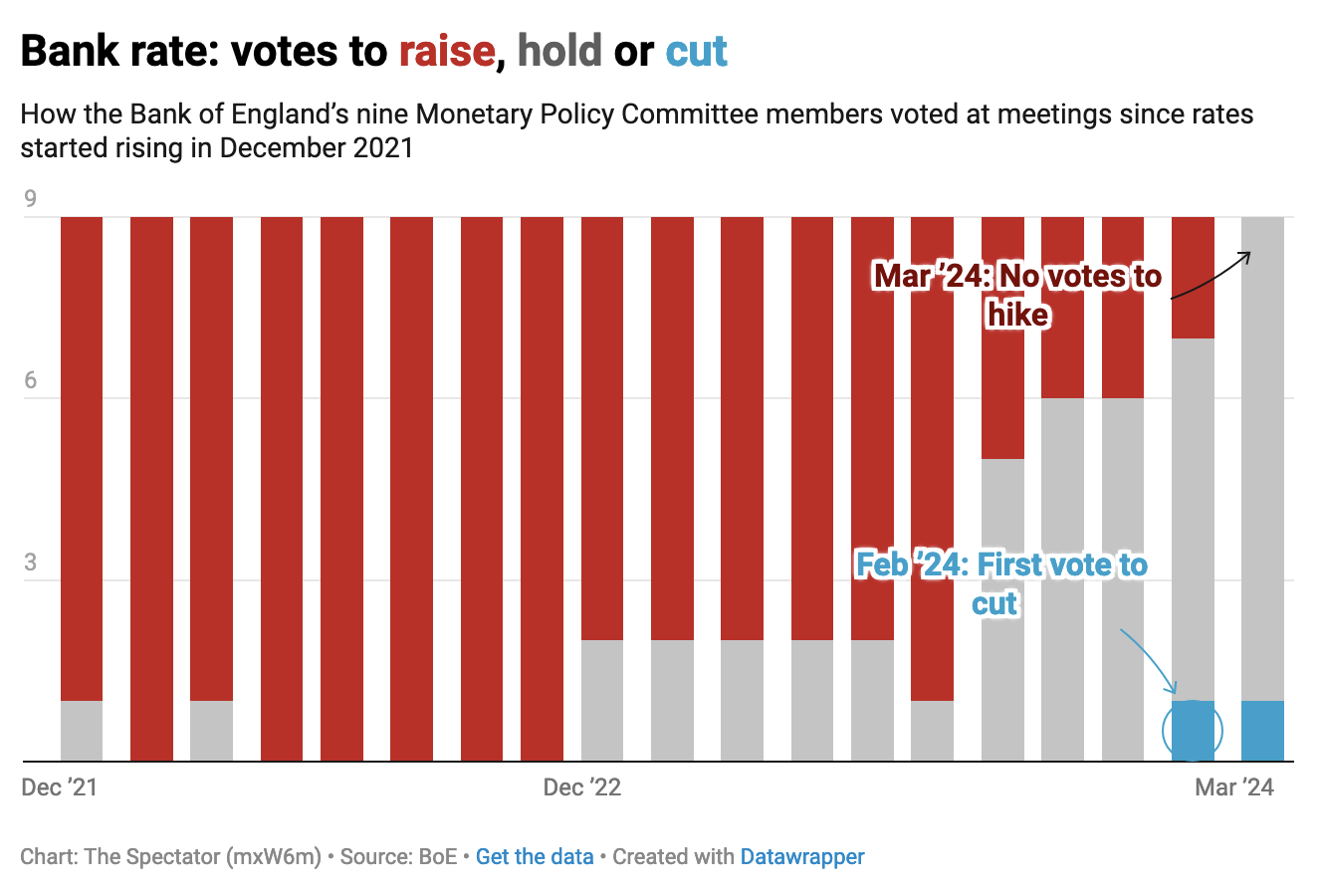

The Bank of England has voted to keep rates at 5.25 per cent – but there are signs that a rate cut may not be far off. The Monetary Policy Committee (MPC) voted 8-1 to hold the base rate. Yet there was a dovish shift in direction compared to the last meeting. In February, the MPC voted 6-3 to maintain rates, with two members voting to raise rates by 0.25 percentage points. Today, no one voted to raise rates – the first time this has happened since 2021. Instead, eight members voted to hold the base rate, while one member voted to reduce rates by 0.25 percentage points.

It was widely expected that the Bank would vote to hold the rate. News earlier this week that inflation slowed again in February, to 3.4 per cent on the year, was certainly a necessary condition for the BoE to consider a rate cut. But Threadneedle Street has been clear for months now that it needs to see evidence that once inflation returns to its target of 2 per cent – which is expected to happen this spring – this can be sustained in the medium term. Today it has stuck to that language, insisting rates must ‘remain restrictive for sufficiently long to return inflation to the 2 per cent target sustainably in the medium term in line with the MPC’s remit’.

But while the MPC waits for more evidence that the fall in the inflation rate is ‘sustainable’, the Bank of England’s governor struck a slightly more optimistic note. ‘We’re not yet at the point where we can cut interest rates,’ Andrew Bailey said in light of the MPC’s decision to hold rates, but he added that ‘things are moving in the right direction’.

What more will the Bank need to see to start cutting rates? Today’s meeting minutes forecast that the headline inflation rate could fall ‘slightly below’ the Bank’s 2 per cent target in Q2 this year, then rise closer to 3 per cent in the second half of the year. Ongoing risks to another inflation bump (albeit nothing like what we saw last time) have the MPC judging that inflation risks are ‘skewed to the upside over the first half of the forecast period’.

This explains their hesitation to start cutting rates just now – especially as many of those inflation risks are geopolitical factors that could be largely out of the UK’s control. However, today’s minutes did note that ongoing Red Sea disruption has not led to any major energy price updates since the Bank’s last meeting in February.

But the real sticking point for the MPC continues to be wages – and fear of a wage-price spiral triggering a second round of price hikes. It’s disputed how much wage increases really play a role in pushing up inflation, but nevertheless it’s a factor the Bank takes seriously and is using to judge when it can start to cut rates. Today’s minutes show how the Bank is dealing with somewhat conflicting evidence, including the fact that nominal wage growth is ‘still elevated’ but also has ‘moderated across a number of measures’.

As Michael Simmons reported earlier this month when the latest labour market data was released, ‘working Britons have now seen 16 consecutive months of average pay rises above 6 per cent – on the year that’s 1.8 per cent wage growth in real terms’, but the latest ‘figures showed a slowdown in pay rises’. It’s this balance that the MPC is trying to gauge, noting in today’s minutes that the ‘labour market has continued to loosen but remains relatively tight by historical standards’. It doesn’t help that there are still big questions around what the Labour Force Survey data has been able to measure, creating a series of ‘uncertainties’ that make it harder for the Bank to feel confident about the trends it’s seeing.

But there is growing evidence that the Bank is now looking for arguments to start cutting rates. While the MPC once again emphasised the importance of keeping monetary policy ‘restrictive’, there was also indication of flexibility, as ‘the Committee recognised that the stance of monetary policy could remain restrictive even if Bank rate were to be reduced, given that it was starting from an already restrictive level’. Put simply: the MPC is hinting that a lower base rate could still be considered restrictive – satisfying the Bank’s requirement to keep the reins on inflation while also easing up, slightly, on rates.

This should give the doves some hope that a rate cut is coming – just not yet. The Bank’s comments today will create a lot of speculation about what the MPC might do in their upcoming meetings in May and June.