Ever had the experience of a service provider sending you an email with the message:

‘Our records show your invoice payment is overdue – please disregard this if payment has been made or make immediate arrangements for settling the account.’

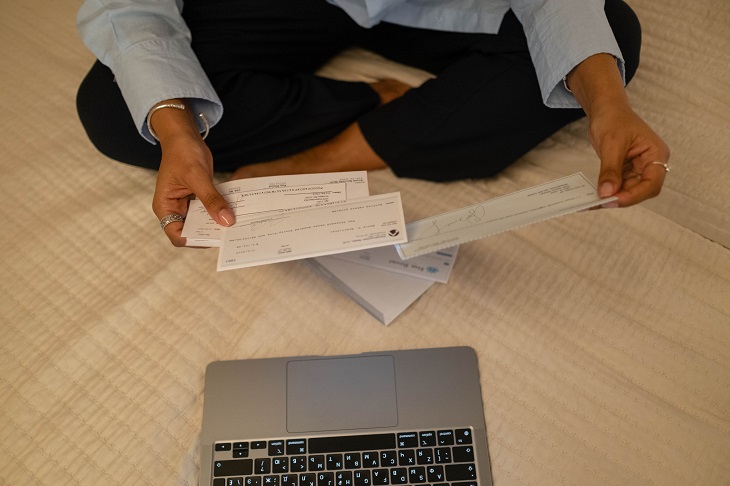

Maybe the wording varies slightly, but we received three with the same theme in as many weeks, and my response has been, ‘We have sent you a cheque…’ Which is the same as the old cliche, ‘Your cheque is in the mail.’

That may be a time-honoured way of delaying a debt payment, but in our case it was true and in each example, we received a receipt within a matter of days.

But that’s all about to end, as I found out recently when we were down to the last form in our cheque book. I remembered receiving a message from our bank stating that cheque books would no longer be issued automatically and we would have to contact them or visit a branch to order a new one.

So I get on the phone to our local branch only to hear a recorded message, ‘We are unable to take your call so please leave a brief message stating the nature of your enquiry and we will get back to you.’ I tell them we want to order a new cheque book and leave a contact number.

No need to state ‘Which Bank’ – suffice to say they recently reported a huge multi-billion dollar profit.

Obviously, they can’t afford enough staff to answer phone calls, but several hours later I receive a call from a woman who tells me our joint account is no longer eligible for another cheque book. Some were, such as business accounts, but not ours.

What the…? We have been loyal customers for many years, buying and selling various homes including investment properties, never missing a loan repayment, and now enjoying a mortgage-free retirement. But as a small cog in a giant wheel, none of that counts when I tell her we may have to look at changing banks.

‘Well, okay.’

I then looked up the terms and conditions of several other major banks whose websites seemed to indicate they still handled cheque accounts. The first two were also recorded messages asking me to press buttons and tell an AI bot the reason for my call. When I finally got through to a woman with a foreign accent, she had difficulty understanding my inquiry and kept asking, ‘Do you have a cheque account?’

‘Yes, but with another bank.’ That finally got through: ‘Oh, well we can’t issue you with a new cheque account.’

Thanks, but no thanks. Finally, one of the smaller banks on my list answered my call immediately and the helpful young woman confirmed that yes, I could open a new cheque account now, but that option would end and no further cheque books would be issued later in the year.

She continued, ‘That’s because of the Labor government policy announced recently that cheques would be phased out.’

So that explains it. I must have missed that one when I was listening to Treasurer Jim Chalmers spruiking about how his great ‘Wellbeing Budget’ was making life easier for Aussies, when we all know the cost of living is going through the roof, led by power price hikes, mortgage and rent increases along with food and transport.

An official statement from Chalmers confirmed that the bank’s advice was correct:

‘The cheque system in Australia will wind down no later than 2030.

‘As part of the Strategic Plan for Australia’s Payments System released today, the government has announced it will remove legislative and other requirements that entrench payment by cheques. We will also phase out government usage of cheques by the end of 2028.

‘As the use of cheques plummets and many banks and financial institutions stop issuing cheque books to new customers, it is important to manage this transition in an orderly and planned way.

‘The government will work with industry to minimise adverse impacts to consumers and businesses and ensure vulnerable Australians have the assistance they need to switch to other payment methods…’

In other words, the Labor government wants us all to switch to online banking, direct debits, or any other emerging digital banking format, and the banks are already hell-bent on forcing the changes on customers – whether we like it or not.

Well, I don’t. Millions of Australians have been notified some of their personal details may have been compromised during hacks on Medibank Private, Optus, and Latitude Financial. Bank scams are rife, so why make life easier for low-life scammers?

According to accounting firm LDB, The latest Targeting scams report by the ACCC has revealed Australians lost a record $3.1 billion to scams in 2022, with investment scams the highest loss category.

The report compiled data from a number of government agencies and marked an 80 per cent increase in losses from 2021.

‘Investment scams comprised $1.5 billion of the total losses and there were more than 9,360 reports to Scamwatch regarding investment scams. …Scammers are now much more sophisticated and more difficult to identify. Impersonating official phone numbers, email addresses and websites of legitimate organisations are common tactics, as well as scam texts that can appear in the same conversation thread as genuine messages. This means that now more than ever, anyone can fall victim to a scam…’

However, some good news for British residents, the UK government has introduced a world-first law to compel banks to compensate scam victims starting from next year, and our Finance Minister, Stephen Jones is reportedly looking at similar legislation here. Naturally, our banks are strongly opposed to such a move but Jones told the ABC, ‘We’re definitely going to lift the bar and we’re definitely going to ensure the banks are accountable for much, much more.’ Let’s hope so!

Meanwhile, I’m sure I’m not the only one shaking my head and wondering where we are headed with this techno talk from Banking Day:

‘The government will provide A$26.9 million in 2023-24 for the Department of Finance and the Digital Transformation Agency to “design the policy and legislative foundations to transition to an economy-wide digital ID ecosystem”.

‘In September last year, the big banks agreed to work on a ConnectID trial, acting as identity providers. ConnectID will act as a digital identity exchange, connecting merchants with identity providers. In trial applications, the digital identification will replace the 100-point check and other ID requirements…’

So what’s it all about, really? Are we steadily falling in step with pronouncements from powerful international agencies which some see as seeking a new far-reaching framework of domination?

WHO Director General Dr Tedros, recently announced a partnership with the EU to establish a Digital Health Certification Network ‘to deliver better health for all’. I think he omitted the word ‘control’.

And the UN Secretary General, Antonio Guterres, has given up ruining suits by wading into the sea to convince us we’ll all be submerged by melting ice, now telling us ‘it’s an era of global boiling’. Right, better get our global Digital IDs to mark our social credits down if we don’t stop using fossil fuels while we still eat meat rather than crickets and grasshoppers!

But back to the banks. My wife visited ‘Which Bank’ the other day and withdrew a sum of cash. The teller asked, ‘What do you plan to do with it?’ (Yes, they have limits and conditions.)

‘Spend it.’

John Mikkelsen is a former editor of three Queensland regional newspapers, columnist, freelance writer, and author of the Amazon Books Memoir, Don’t Call Me Nev.