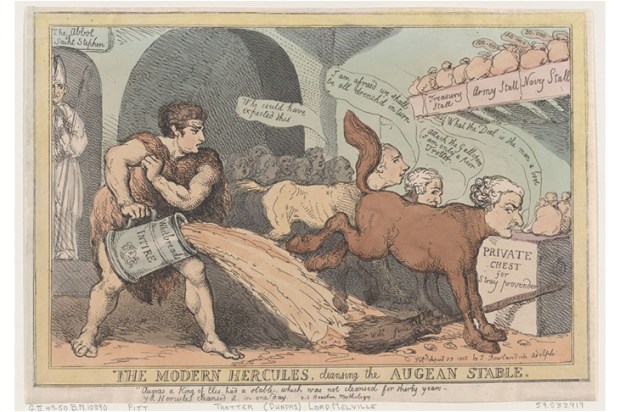

At the start of 1962, inflation threatened the US economy. President John Kennedy thought the key to controlling the menace was to prevent steel companies from lifting prices. To help steel mills contain costs, Kennedy blocked union-led wage pushes. But Big Steel in April that year raised prices anyway.

Kennedy was furious. Still diminished by the Bay of Pigs fiasco, JFK thought steel executives made him look weak ahead of more talks with Moscow. So he set out to reverse the increases in steel prices. The White House leaked that JFK regarded steel executives as ‘sons of bitches’ and he marshalled public opinion against steel companies. But Kennedy knew that wouldn’t be enough. So he did more.

What did Kennedy do? Offer subsidies? Tax breaks? Higher tariffs? No, no and no again. He unleashed his brother Robert, his attorney general. RFK instructed the FBI to interrogate steel executives about price fixing, let the media know about these grillings, and ordered the agency to subpoena company and personal records. To maximise the pressure, Robert sicced the tax department onto steel bosses. JFK joked about their hotel bills and night-club expenses becoming known to the ‘weekly wives bridge group’, one biographer recounts. Lo and behold, the steel companies cancelled their price increases.

Kennedy’s police-state tactics to fix prices in a key industry, however, came with costs. The backlash against government encroachment on free enterprise triggered in May the biggest one-day fall (6.5 per cent) on Wall Street since 1929.

It could be argued Kennedy’s actions fall under ‘industry policy’, which is defined as state action to direct business to achieve state economic and political goals. Industry policy was a common tool in Kennedy’s day and the term describes much official policy nowadays. Western governments, especially Washington, are reversing four decades of non-intervention for two reasons.

One is to combat China. Security concerns justify subsidies and tariffs to nurture domestic capabilities. They validate export and investment controls to hinder rivals. Amid all the efforts to impede China, the standout is Washington’s US$52 billion CHIPS and Science Act of 2022. The law is designed to boost US self-sufficiency in microchips while slowing China’s progress in key technologies. Hobble-China efforts include Western government pressure on their companies to reduce relying on China for supplies, an economic efficiency the pandemic exposed as a security flaw.

The other reason for the revival of industry policy is to promote renewables. Of government efforts to boost green industries, the most ambitious is the US’s misnamed Inflation Reduction Act of 2022. This law is officially a US$369-billion green-energy bonanza based around subsidies and tax credits that purports to reduce US emissions about 40 per cent from 2005 levels by 2030. Prime Minister Anthony Albanese’s recent claim of achievement, Australia’s just-announced clean-energy compact with the US, covers these two reasons.

Officials hope that today’s industry policies will be as successful as hailed ones of the past. But industry policy always comes with challenges. A big handicap is that government intervention distorts the allocation of resources. To Europe’s ire, US subsidies are diverting green investment to the US. Another problem is industry policy ferments ‘crony capitalism’ – renewables are the new vested interests. Then there’s retaliation. Beijing regards US export controls as ‘economic war’. No surprise that China in May banned the purchase of semiconductors made by Micron Technologies of the US.

Another weakness of industry policy is that governments are reluctant to admit they have backed losers. Official support for wind and solar power makes it harder for policymakers to turn to better options – say, nuclear. A further limitation is that industry policies fail if all countries adopt them.

These are standard flaws with industry policy. What’s intriguing is that industry policy these days has four additional challenges that argue against success. One is the administration of President Joe Biden is using industry policy to pursue agendas unrelated to containing China or boosting renewables. Conditions tied to the CHIPS Act include limits on stock buybacks, using unionised workers and providing affordable childcare. Such tangential conditions stir cynicism and boost business costs.

Another challenge is the cost of industry policies are another strain on stretched government finances. That casts doubt on the sustainability of these programs, which inhibits business investment. That the cost of Biden’s green Act could triple to US$1.2 trillion because the tax credits are uncapped highlights this risk.

Another challenge is the politics of climate change are unsettled. Doubts about whether an industry policy will last beyond the next election undermine business confidence to invest longer time while encouraging them to milk incentives shorter term. It’s of note that Republicans tried to denude Biden’s green agenda during the US debt-ceiling negotiations.

The final extraordinary challenge is that the two reasons driving the revival of industry policies are in conflict. To achieve renewable targets, Western countries need Beijing to join global accords and require China’s processed green minerals and manufactured green products such as solar panels. But the West is hobbling China’s industrialisation while stirring Beijing’s resentment. Sitting here too is the conundrum that Australia’s biggest export market is the country’s most likely wartime foe. Yet Australian prosperity demands the unhindered sale of commodities that help China militarise. Something must give.

In a world where China, long a practitioner of industry policy, has morphed from a competitor into a rival, it was inevitable the West would respond in the same way. But today’s extraordinary challenges on top of the standard flaws mean it will be hard for the West’s industry policies to succeed as hoped.

To be sure, governments have never been divorced from industry, their intervention is a matter of degree. For all the challenges facing industry policy, policymakers will have some success. Applied Materials, for example, in May said it would invest US$4 billion in a semiconductor research facility in California.

If officials want greater success on China and climate, perhaps they should study how Kennedy froze steel prices. First, JFK set a specific goal. Second, he used affordable and effective means. Third, he calculated the benefits exceeded the cost. Today’s industry policies fail on the first two criteria.

Thus the third is in doubt.

Got something to add? Join the discussion and comment below.

You might disagree with half of it, but you’ll enjoy reading all of it. Try your first month for free, then just $2 a week for the remainder of your first year.