If anyone was expecting markets to be in jubilant mood after Liz Truss’s resignation, they will be feeling a little disappointed. True, the pound has risen and gilt yields have fallen this afternoon – but not by much. They moved far further on Monday when most of Truss and Kwasi Kwarteng’s mini-Budget was ditched, which is perhaps only to be expected.

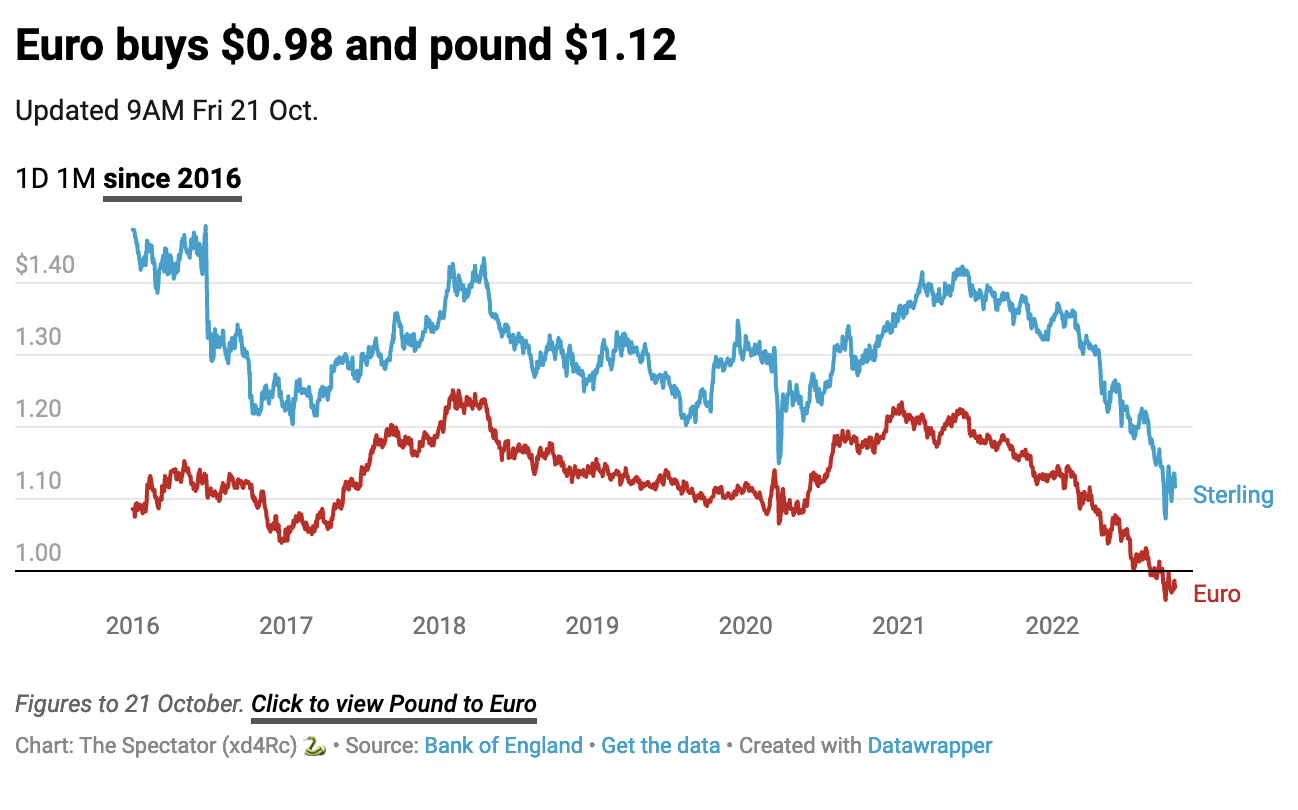

At 3.30 p.m. yields on the UK government’s ten-year gilt stood at 3.85 per cent, down from just below 4 per cent early this morning. This time last week, when Kwarteng was still chancellor, they topped 4.4 per cent. They began Truss’s brief premiership at 3.3 per cent. Rising gilt yields, though, long pre-date Truss. At the beginning of the year, they were at 1 per cent. As with gilts, so with the pound which, roughly an hour after Truss’s resignation speech, stood at $1.13: a rise of nearly 1 per cent on the day. That is back to where it was a week ago. Again, the pound’s big slide against the dollar didn’t begin with Truss’ premiership or with the mini-Budget. It stood at $1.15 on 5 September – the day she took office – but began the year at $1.35. As for stock markets, they are largely unmoved. At 3.30 p.m. the FTSE 100 was up 0.27 per cent on the day and the FTSE250 up 0.97 per cent.

While bond investors may be relieved to see the back of Truss, they are now faced with the uncertainty of her replacement – and whether the new prime minister will be able to command the cross-party support which Truss so lacked. If they can’t, we could be heading for a general election – and markets may not like that either. Much as Keir Starmer might feel up on his luck, Labour has a history of reckless spending and running up large deficits (even if the party has now been thoroughly outdone by the current Conservative government). Labour MPs seem to like to think that markets were rebelling against low taxes. But what really upset them in the mini-Budget, surely, was excessive borrowing and the threat of the UK government being unable to pay its debts. Taxes are only one half of the government’s ledger – the other half being spending.

Either way, international investors are unlikely to rediscover their appetite for UK assets until they can make some sense of the political situation here – which is unlikely to happen in the near future.