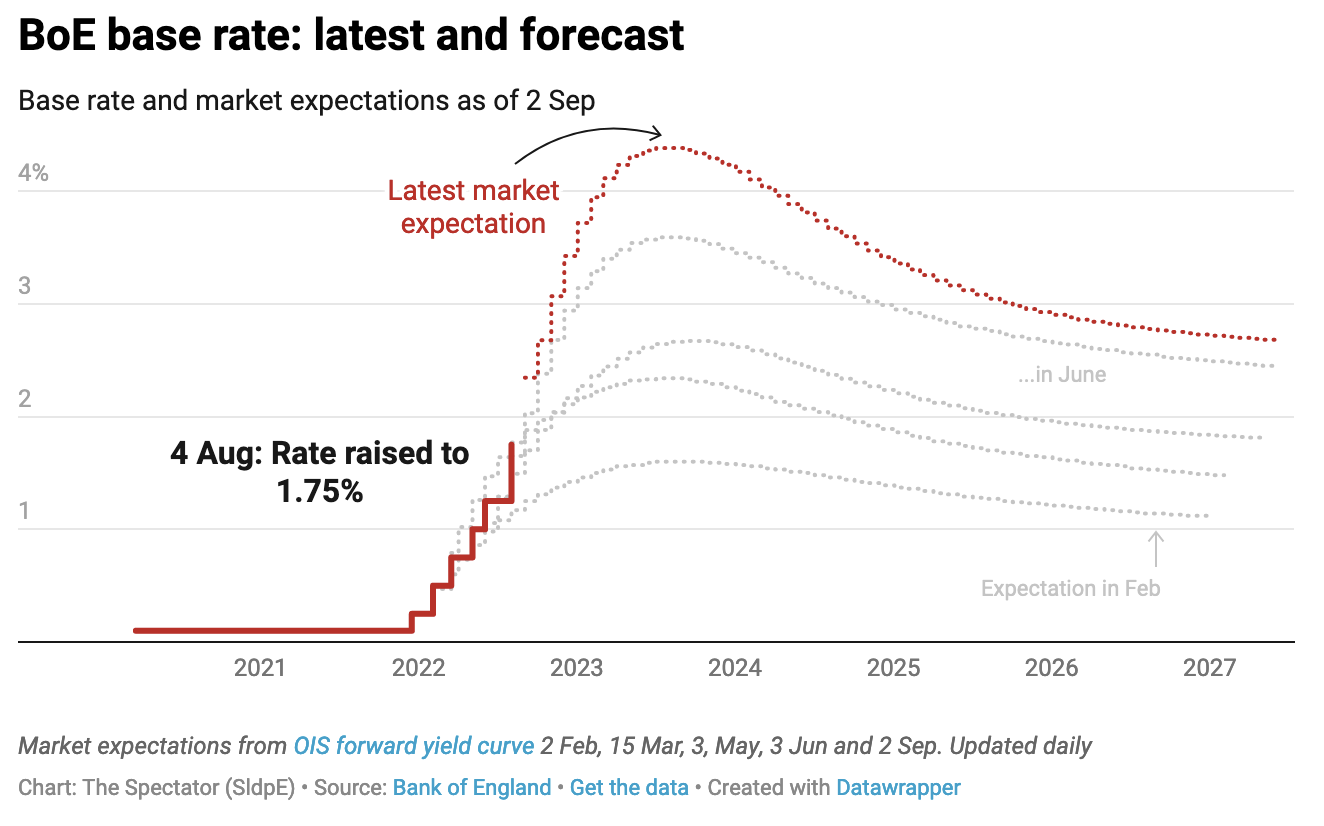

Look at the chart for interest rate expectations in isolation, and you might come to the conclusion that Rishi Sunak is right about Liz Truss’s fiscal policies. In June, markets were expecting rates to peak at around 3.5 per cent next year; now they are expecting them to reach close to 4.5 per cent. Moreover, as Truss’s victory came to be seen as inevitable, the FTSE 100 plunged from 7,550 on 19 August to 7,230 this morning – a fall of 4.2 per cent. The pound has fallen from $1.22 on 10 August to $1.15 now.

But hang on a minute. Markets have been revising their interest rate expectations all year. In February, long before anyone was talking about the possibility of a Truss government, markets were expecting rates to peak at 1.5 per cent. As for stock markets, they have been plunging around the world in the past fortnight. The S&P 500 has fallen 8.5 per cent since mid-August and Germany’s DAX 6 per cent. So, on that score, you could argue that the prospect of a Truss government is seen as relatively good for company valuations – which it ought to be, considering that she has promised to cancel corporation tax rises. Then again, the FTSE has been outperforming other indices all year, not least because it has a much higher element of oil stocks.

To become Prime Minister at a time of economic turmoil is unenviable in many respects, but there is one advantage: it becomes impossible to dissociate your own personal effect on the markets from other factors. That might be useful for Truss when it comes to indicators that are less easily explained away.

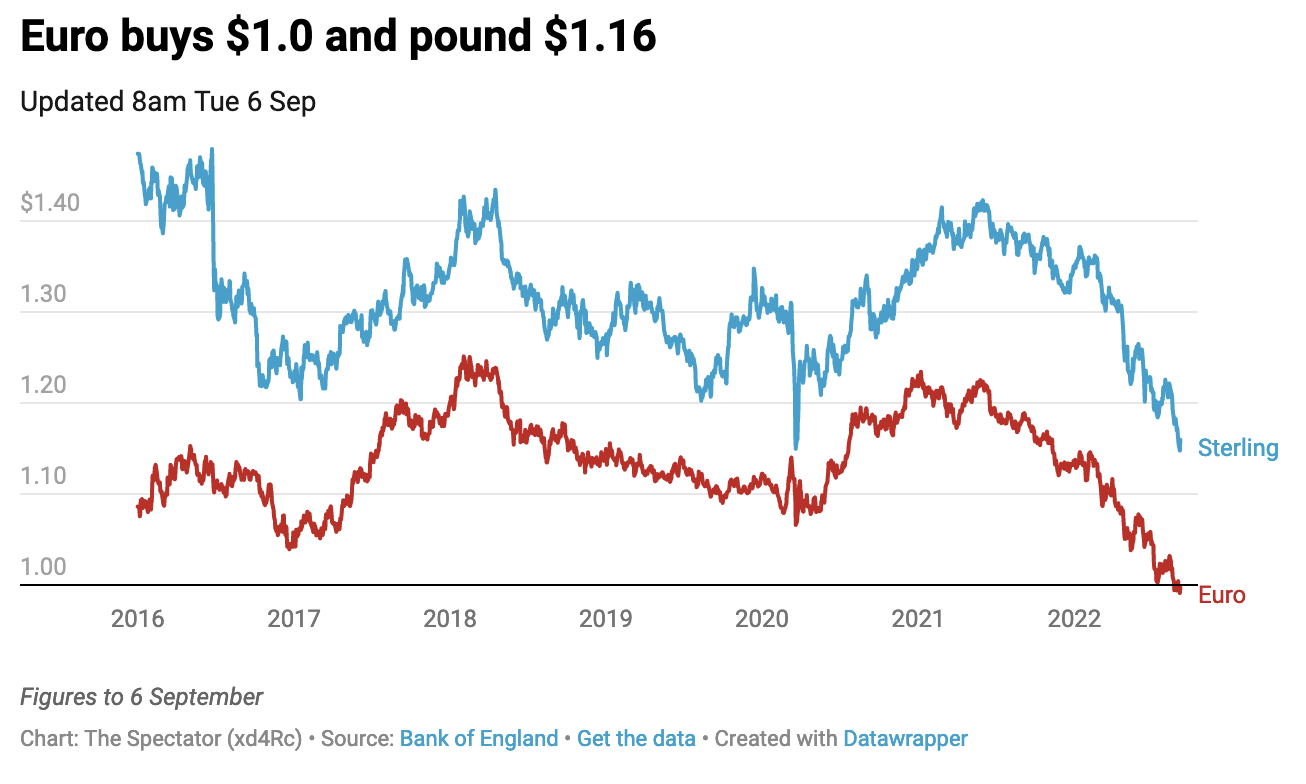

The most worrying of these is the falling value of the pound. It is true that the euro has been falling against sterling too – or alternatively you could say that the dollar has been appreciating against both currencies. But the pound has had the worse time in recent weeks, as it has been falling against the euro – down from €1.19 on 10 August to €1.15 now. That doesn’t suggest a huge amount of faith in the new regime’s ability to grow the economy.

Liz Truss is unlikely to be fretting over any of these market gyrations, however. She has positioned herself as a disruptor who will do away with Treasury orthodoxy and replace it with fiscal policy designed to spur growth. Monetary policy could also have a role: while Truss is not proposing to reverse the Bank of England’s independence, she – or rather her Chancellor – could always reset the Bank of England’s inflation target, or even eliminate inflation targeting altogether.

Markets could be forgiven some apprehension at the prospect of significant and unknown changes. But Truss may well feel happy with low expectations. At the first sign of an uptick in fortunes, she can claim success. Whether voters will believe her is another matter.