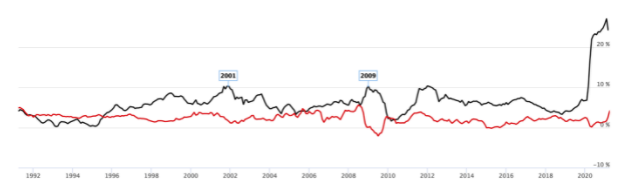

The recent lift in the United States annual inflation rate to 4.2 per cent, the highest in ten years, has caused fears that the massive injection of money into the economy (33 per cent in the latest month) might now be igniting a general lift in prices. Below is the Consumer Price Index (in red) and money growth (in black).

Many will, however, argue that predictions of runaway inflation have not materialised in the recent past.

Views on the relationship between prices, output, government deficits and money supply have gone through major transformations. Until Keynes’s General Theory in 1936, the notion of an unbalanced budget had little following among economists. Even so, deficits became an integral part of the US Roosevelt Administration’s response to the 1930s Great Depression. The US unemployment rate was 25 per cent in 1933 and did not drop below 14 per cent until 1940. In 1938 GDP was barely above its 1930 level.

Britain followed a different policy path under Chancellor (Treasurer) Neville Chamberlain, who like our very own Paul Keating was an excellent Treasurer but an appalling Prime Minister. Chamberlain reined in spending and balanced the budget. The UK’s unemployment rate peaked at 17 per cent but had fallen to 8 per cent by 1937 with a respectable four per cent annual economic growth rate after 1933.

Even so, governments in the 1950s and 1960s, to counter economic downturns, generally applied deficit spending. The “money illusion” was seen as helping to return economies to a growth path. This was always accompanied by inflation and the (Phillips Curve) theory was that we could trade off lower unemployment for higher inflation. However, to combat successive downturns, the required level of inflation increased until in the 1970s we encountered “stagflation” –high inflation and no growth.

Rivalling the Keynesian deficit spending antidote to recessions was monetarism, based on Milton Friedman’s studies of the US 1930’s Great Depression. Friedman’s prescription was to keep the money supply growing by a low but steady rate. Avoiding an abrupt reversal from accommodating monetary policy to a massive reduction in supply would, he argued, mean far less economic volatility.

In fact, an aggressive use of money creation to boost demand is little different from deficit financing. Both depend on providing additional, unearned, incomes to consumers and producers, tricking them into believing this is income from goods and services that have actually been produced and bringing them to gear up for increased output. History shows that if such policies ever work, they certainly do not enjoy sustained success.

Now we are in an era where policy combines both loose money and deficits. Support to prevent economic collapse due to COVID closure policies has been followed by money creation with near-zero interest rates and deficit financing. The economy has seen output restored to its pre-COVID levels.

But the enforced shutdown did not undermine the economy’s productive potential. Shops, factories, farms, energy and communications networks remained in place. Many of their owners faced financial ruin but the assets and labour force were intact. Under these circumstances, it would have been extraordinary had a bounce-back not taken place.

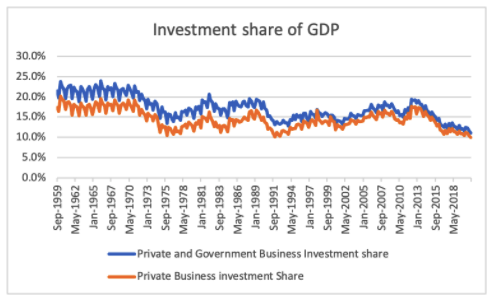

Beyond that, the outlook is less promising. Investment, the building block of living standards, has sharply contracted — and the additional funding of government expenditures must eventually cannibalise other, more productive avenues of spending. From tracking within a range of 15 per cent (during recessions) and 25 per cent (during booms) the share of business investment within GDP is now only 10 per cent with no recovery in sight. This can be seen in the following graphic derived from the national accounts.

Whereas the US money supply is expanding by 33 per cent and its deficit is 10 per cent of GDP, Australia’s money supply increase is a “mere” 10 per cent of GDP and its deficit 8 per cent of GDP. Australian Government policies may impose less harm than those of the US, but harmful they will be.

Alan Moran is with Regulation Economics.