After every Budget, big or small, Tory backbenchers usually meet with the Chancellor. But on the evening of Rishi Sunak’s mini-Budget this week, they had already scheduled in a meeting with Andrew Bailey, the new governor of the Bank of England. This was extraordinary. Since when does the governor talk to MPs? Or risk upstaging the Chancellor? Worse still, the Treasury had not been told about the governor’s new gig. When the news was broken (by Katy Balls on The Spectator’s website), phone calls were made and the Bailey address was rescheduled. Natural order was restored — for the time being, at least.

But had the governor appeared, the Tories would have had plenty to ask. It has not escaped their attention that the UK government is being kept financially afloat through money printed by the Bank of England. The sums are vast: a deficit of £300 billion this year, made possible by £200 billion of quantitative easing. To put that in perspective, another £5 million will have been borrowed by the time you finish reading this article. In Wednesday’s summer statement, Sunak added another £30 billion, suggesting in the ‘medium term’ the Treasury would figure out how to pay for his jobs and stimulus schemes – but there was no real indication as to when that might be. Right now the pressure is off. The Bank is facilitating a money circle for the government: printing the money it wants to spend, then mopping up the debt it leaves behind. This creates an artificial market, keeping borrowing rates deceptively low. But how long will it last? When might Bailey cut off this supply of cash? How long can we keep getting something for nothing?

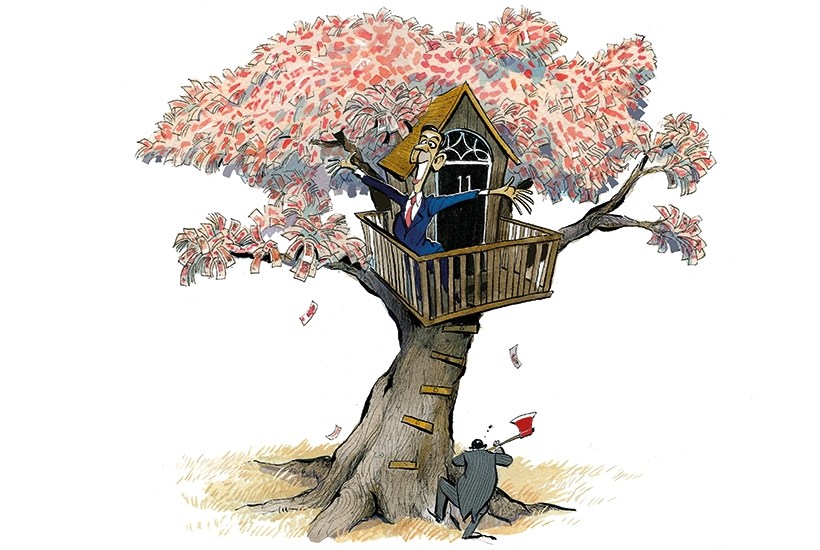

Boris Johnson was elected after saying that the austerity of the David Cameron years had been a mistake. True to his word, he has seen spending as the solution to most of the problems he has encountered, since long before Covid turned our world upside down. The last Budget, in March, showed a huge rise in spending and debt: mostly for non-virus-related projects including state infrastructure (the ‘build, build, build’ agenda), broadband and other costly government interventions. Then, as now, the government was able to borrow money at record low rates. The seeds of a magic money tree were being planted long before the virus struck.

‘We fought the last election saying there was no money tree,’ says one senior Tory MP. ‘Now we say there is one, and it’s in the garden of the Bank of England.’

But there is a problem with the gardener. Bailey is not particularly close to the Prime Minister. Indeed, No. 10 tried to stop his appointment and put in Andy Haldane, the Bank’s chief economist, instead. The then chancellor, Sajid Javid, pushed him through. When Bailey took the job at Thread-needle Street, a position guaranteed for eight years, he knew that he was there in spite of Boris Johnson, not because of him.

After just three months in the job, Bailey had found ways of making it clear where he will draw the line, especially against a No. 10 that is now so keen on high spending. It’s the Bank’s job to stabilise the UK economy, Bailey says, but not to pay the bills of the UK government. Speaking on Javid’s podcast, he said: ‘At no point have we thought that our job was just to finance whatever debts the government issue… that’s not part of our objectives. I’ll be absolutely blunt about that.’ He does not see it as his job to prop up the Tories’ ‘levelling up’ agenda or the net-zero target, which have so far been framed by the government as being essential to economic recovery. The implication that the Bank may turn off the taps terrifies many Tories.

And the drought may come soon, as the government redirects its focus from emergency measures — such as the furloughing scheme and business loans — to policy ideas that are not central to tackling the virus. The infrastructure package announced by the Chancellor in his summer statement this week, along with the Green Homes Grant, strike remarkable resemblance to ideas floated in the party’s 2019 manifesto. The decisions to press on with HS2 and to offer guaranteed apprenticeships are unlikely to be categorised as one-off spending after the Covid crisis, but rather as components of an increasing structural deficit. Now that the government has agreed to provide free school meals over the summer, it’s difficult to see how that scheme could be rolled back next year, or anytime soon. But this is a welfare policy, not a Covid one — and the Bank does not think it should be responsible for delivering it.

Britain is not alone as it ramps up spending. The world over, central banks are printing money to bankroll governments during the Covid crisis. When this stops, perhaps in the autumn, it will be a test of countries’ credibility. Britain is paying just 0.25 per cent annual interest on money it borrows now, amounting to tens of billions of pounds paid to service the debt. Few economists expect to see a rise in interest anytime soon, but the margin of error is slim; if rates spiked to just 1 per cent, the effect could be crippling.

What happens if the Bank cuts off the credit when Downing Street wants it to continue? A decision made by the Bank could bring Boris’s spending spree to a close, which the governor is ‘bluntly’ saying he’d be quite prepared to do. ‘If that happens, I think it’s 50/50 that No. 10 tries to renationalise the Bank of England,’ says one senior Tory. A radical idea, and one that would terrify the Treasury, which believes that ending the Bank’s independence would risk bringing the whole system crashing down.

The sums being borrowed now may be akin to wartime spending, but this is no normal wartime. Sunak argues that the absolute levels of debt matter less than the cost of servicing it — a more favourable metric for the government, since interest rates have been rock-bottom for some time. In the eurozone, Japan, America, even Sweden, central banks are printing money to lend to governments: the global supply of cash is rising at levels that in any other period of history would have predicted a surge of inflation. To get through the Covid-19 crisis, Britain has had to borrow more than almost any other developed country. Its debt-financed spending is higher than Italy’s, Greece’s or Spain’s. In an ugly baby contest, the UK may look even worse than the rest. If there’s a crash in Asia or a boom in Africa, Britain’s interest rates may have nowhere to go but up, especially if the institution pulling the levers shifts its position even slightly.

Britain is not plunging itself into more debt from a position of strength. The country has not come close to balancing its books for nearly two decades now. The Office for Budget Responsibility has been warning of the UK’s overspending for years, projecting that in the next half-century, the debt to GDP ratio will approach a staggering 275 per cent. Now that a crisis has hit, its lack of preparedness means Britain must focus on rebounding from this economic contraction. Decades worth of bad financial planning make this difficult. The issue of the day — how we pay for Covid — is not actually the biggest concern: that the country has never meaningfully come up with a plan to pay for healthcare, pensions and public liabilities in the medium-term is the real weakness, and could cripple recovery in the years to come.

The Chancellor has set out an expansionary phase of government, producing an economic spending plan that was always going to be difficult to finance. Sunak, a former Goldman Sachs banker, will be acutely aware of that. Even if the UK gets a V-shaped recovery — and returns to an economy that looks similar to how it did in January — spending is now completely out of kilter with revenue. If the Bank of England stops its money-printing and it becomes harder to borrow, the government will be in the difficult spot of having to make trade-offs. Tax rises, perhaps even a return to austerity. Exactly what it wanted to avoid.

Perhaps it will all be fine. Perhaps the Tories can settle into a bigger debt and high budget deficits, and the markets — still worried about a post-Covid world — will keep lending. And the Prime Minister can keep splashing the cash, crossing his fingers each night that tomorrow isn’t the day it all goes wrong. He never needed much encouragement to rip off the fiscal straitjacket, but now it lies in tatters on the ground and a magic money tree has sprung up next to it. But like any other resource, its value is subjective. If history has taught us anything about money trees, it’s that the more they’re used, the more worthless they become.

Got something to add? Join the discussion and comment below.

SPECTATOR.CO.UK/PODCAST - Kate Andrews and the economist Miatta Fahnbulleh on the magic money tree.

You might disagree with half of it, but you’ll enjoy reading all of it. Try your first month for free, then just $2 a week for the remainder of your first year.