Retirement may seem a long way off, but by the time you are 50 you could have only 180 monthly paydays left to make your financial preparations for your later years (and that’s assuming you continue working to 65 – your working life could end sooner).

Think of yourself as being on a runway to retirement: in your 20s and 30s you are starting on the runway, by your 40s you are already half way to take-off – retirement – and by your early 50s the end of the runway is fast approaching.

When was the last time you took a close look at your pension savings? Not just glanced at your annual pension statement, but clarified what you want your pension to achieve and whether you are on course to reach your retirement goals.

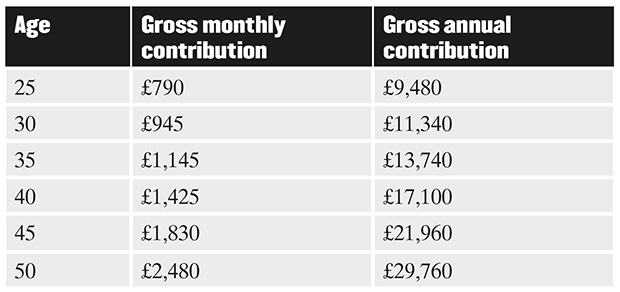

A few years’ delay in starting a pension can have a dramatic effect on the size of your pension pot and the retirement income that you are able to draw from it. A 40-year old who wants to retire at 68 on £20,000 a year in real terms could achieve this by saving £1,425 a month gross. Wait until 50 to start saving into a pension and you would have to save £2,480 a month to achieve the same objective.¹

Even if you have been saving into a pension for many years there is no room for complacency. As long as you are unsure what you want your pension to achieve and whether it is on course to deliver at retirement there is always the danger that it could disappoint. Establishing when you would like to retire, how much money you will need to live on and whether your savings are on target gives you the basis around which to create your retirement plan.

Your 40s is often a good time to build on your existing savings. You may be hitting your peak earnings years and can potentially benefit from higher tax relief of 40% or even 45% on your pension contributions. Another reason to take advantage of pension tax allowances as soon as you can is that there is no guarantee they will be there in the future.

Target £20,000 a year net pension in real terms at age 68 (excluding State pension)

Source: Brewin Dolphin.

Figures assume a yearly investment growth of 2.5%, inflation of 2.5% and fund charges of 1% a year. Contributions assumed to increase by 4% annually and to continue until age 68. These figures are illustrative and to achieve the target you may have to contribute more than this. You should remember that the value of investments can fall and you may get back less than you invested.

The government could decide to reform pension tax, so it makes sense to make the most of what is on offer now.

There have been substantial changes to the pension system recently and there could be further changes ahead. Last year a government consultation on pensions tax relief included a proposal to switch to a single flat rate of relief on contributions, potentially at a level between 25% and 33%. This would have meant reduced tax breaks for people on higher incomes, while giving additional benefits to basic rate taxpayers. And while the former Chancellor George Osborne concluded that there was “no consensus” for reform, this may be only a stay of execution for higher-rate tax relief on pension savings. If a flat rate were introduced in future, higher- and additional rate taxpayers could receive thousands of pounds less in tax relief.

We don’t know what the new government’s tax priorities will be in the wake of the EU referendum nor what the next Budget may hold. But it makes sense to expect turbulence on your retirement runway. Your situation will change over time so you need to check whether your pension is on track on a regular basis. Pension contributions are typically paid into investment funds, which need to be monitored at least annually to ensure that they are performing as they should be. If they are not faring well, it could be worth getting specialist advice about improving the performance of your savings.

As you get older, your attitude to risk may also change. This can be a complex area and it is sensible to get expert advice on ensuring that your pension savings are appropriately invested over time.

A good financial planner can help you with ‘cashflow analysis’ for your retirement. This will analyse your future cashflow position and identify areas where you are potentially at risk of a shortfall. They will also be able to ‘stress test’ how different financial decisions, growth rate assumptions, inflation and other economic events might impact on your ability to meet your financial goals in retirement. This can be used to answer questions such as how much money you will need to retire and how much it will cost you now to achieve this. If you make the right decisions, meeting your retirement goals need not be hard work. But it is not something that can be left to chance.

¹Assumes that the income is taken from a flexible drawdown pension product. Please note that this document was prepared as a general guide only and does not constitute tax or legal advice. While we believe it to be correct at the time of writing, Brewin Dolphin is not a tax adviser and tax law is subject to frequent change. Tax treatment depends on your individual circumstances; therefore you should not rely on this information without seeking professional advice from a qualified tax adviser.

The figures in this document are based on tax rates and thresholds prevailing as at 6 April, 2016 and will be subject to future change. The amount of savings that need to be made assume the saver uses a flexible drawdown pension product at retirement.

The value of investments can fall and you may get back less than you invested. No investment is suitable in all cases and if you have any doubts as to an investment’s suitability then you should contact us.

The information contained in this document is believed to be reliable and accurate, but without further investigation cannot be warranted as to accuracy or completeness.

The post Don’t run out of runway to retirement appeared first on The Spectator.