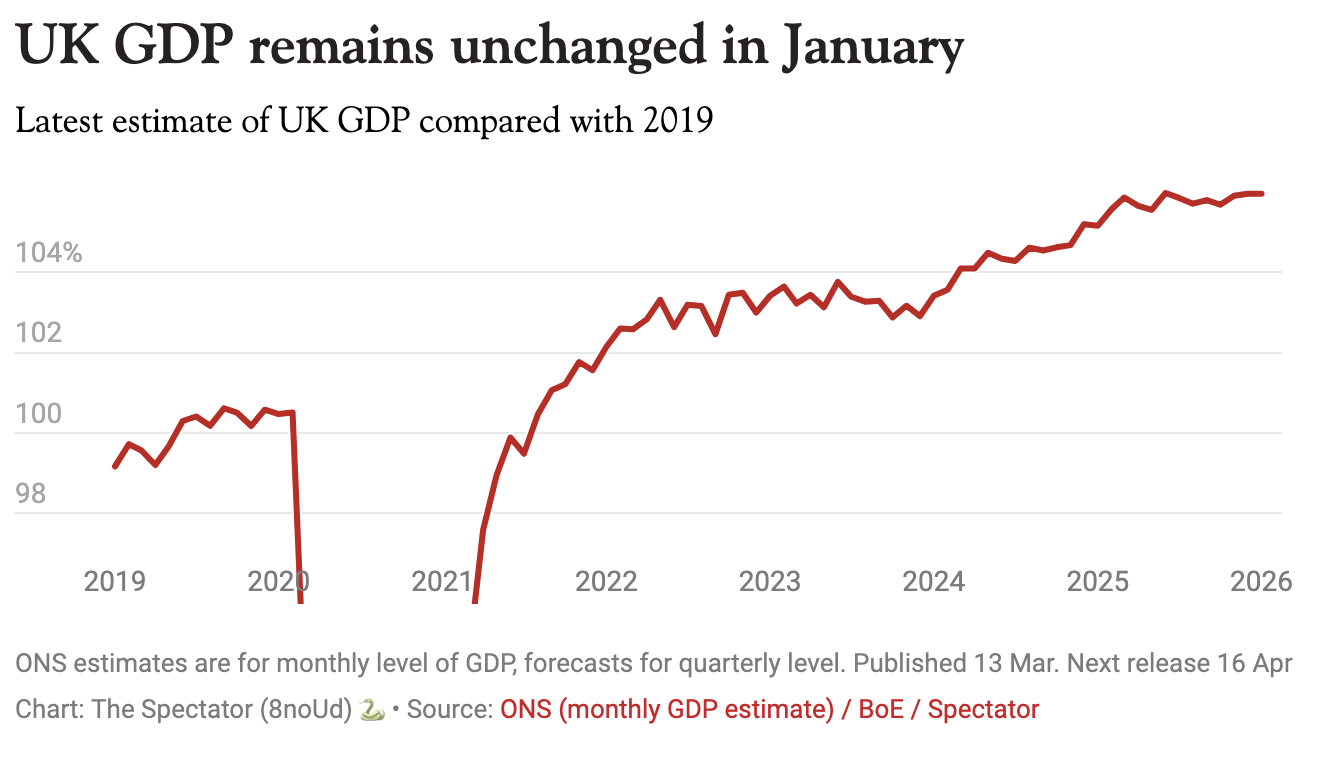

Figures just released by the Office for National Statistics (ONS) show the economy ground to a halt in January, with no growth recorded. That was despite economists and businesses reporting a brighter start to the year. Economists had expected January to see growth of 0.2 per cent.

Over the three months to January we did see some growth, though just 0.2 per cent. Within that figure, services expanded 0.2 per cent while production grew 1.3 per cent. The positive numbers end there, however, with the construction sector contracting by 2 per cent.

It’s unlikely things are going to get much better as the year goes on. Pretty much everyone is now factoring in higher inflation thanks to the oil price shock caused by disruption in the Strait of Hormuz and the wider war in the Middle East. That won’t just mean higher prices, it means interest rates higher than they otherwise would have been too. The knock-on effect will be reduced household spending power and consumption and even more lacklustre growth.

We have all become more attuned to inflation

That painful year will be set in motion at the Bank of England’s Monetary Policy Committee (MPC) meeting next week. A cut is certainly off the cards. But so too, I think, is a hike. Committee members don’t want to be wrong and so the risks of slamming the brakes on an already languid economy will weigh heavily on their minds. Holding rates at 3.75 per cent therefore seems to be the cautious option.

This is already creating havoc in the mortgage industry. The average mortgage rate has jumped above 5 per cent and this week has seen the most withdrawals of products from the market since the aftermath of the mini-Budget in 2022 – though still on a much smaller scale. Whether that gets worse or better later this year really depends on how long things drag out in the Middle East.

Now, having said all that, there’s some old-school thought that my analysis is all wrong – that the Bank has a track record of looking through shocks and refusing to let them make it change course. Anyone remember ‘transitory’ inflation, for example?

But something in British households and businesses has changed. We have all become more attuned to inflation – having experienced more of it – and our expectations for where prices will go in the future have heightened. That makes second-order effects of shocks such as the current one far more likely. It is this new feature of Britain’s economy that means caution when it comes to monetary policy will win the day.