It was a year ago this weekend that Liz Truss sacked her chancellor, Kwasi Kwarteng, over the fallout of their ‘growth plan’. This marked the beginning of the end of Truss’s premiership: she then appointed Jeremy Hunt to the role, and he swiftly dismantled almost every part of her infamous mini-Budget.

Since leaving No. 10, Truss has been quick to return to the political spotlight, writing comment pieces for national papers, giving interviews, making speeches and interventions – and launching a Growth Commission through which she continues to take the Office for Budget Responsibility to task. But just as Truss continues to make her views known, so do her critics.

One of those critics is Andrew Bailey, the Bank of England’s Governor. Speaking at the International Monetary Fund and the World Bank’s annual meeting in Marrakesh this morning, Bailey was keen to draw comparisons between the economic landscape this time last year and today. The IMF has downgraded its forecasts for economic growth in the UK next year (which I look at, and question, here), but Bailey couldn’t help but to compare the circumstances to the Truss era, saying: ‘I’m probably the one person that can come in here and say things really do look better today than they did on this day last year.’ He then doubled down on his comments to the audience, adding: ‘I can say that with some confidence.’

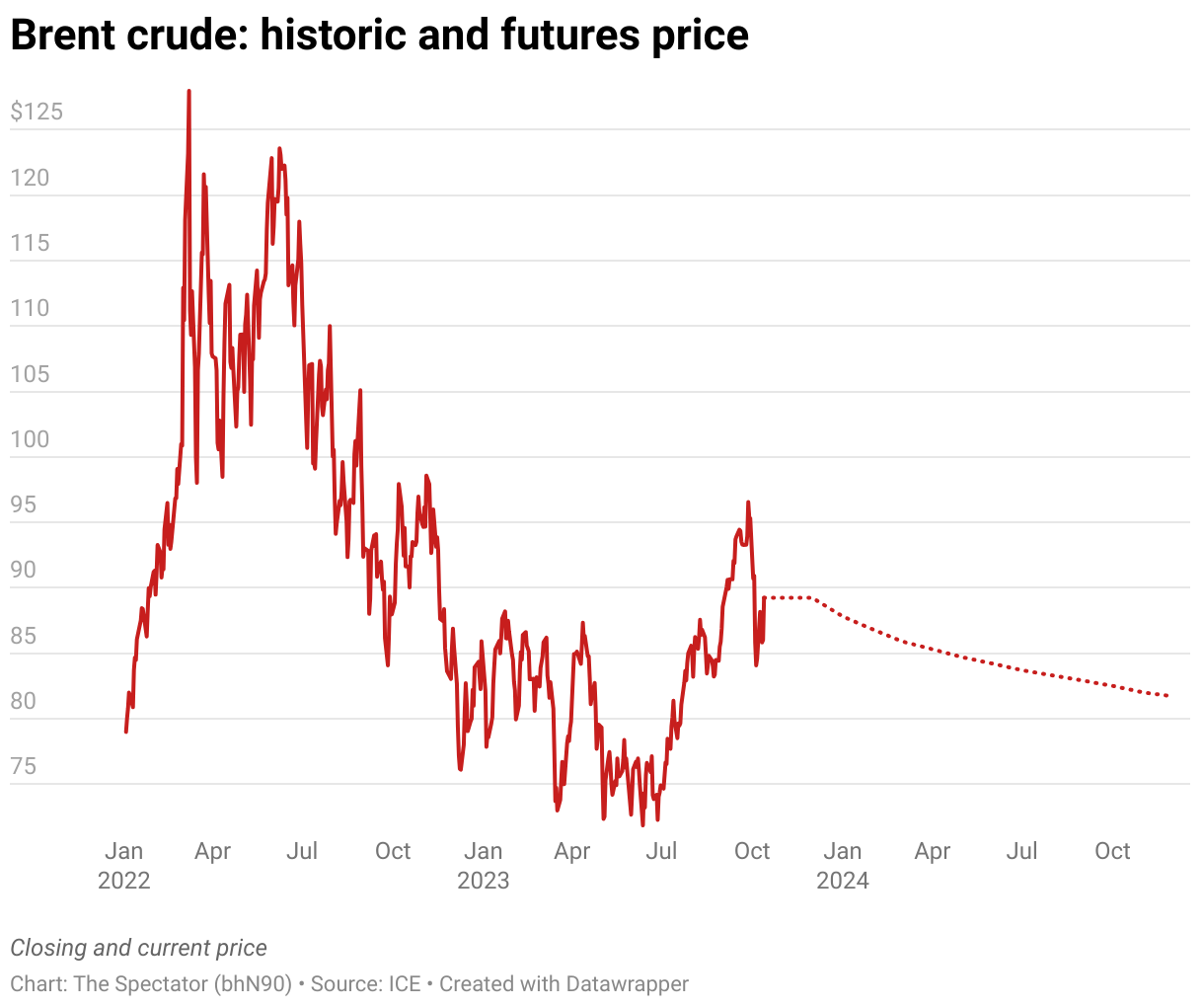

But markets weren’t tuning in for Bailey’s take on Truss – they were listening closely to the Governor’s comments on the future of rate hikes, at a time of increasing uncertainty. The cost of petrol rose in October for the fourth consecutive month, while the brutal attacks carried out by Hamas in Israel have triggered a spike in oil futures. So far, the FTSE seems to be holding up slightly better than its peers, mostly thanks to BP and Shell’s strong performances, which have been balancing out other dips.

Bailey didn’t stray far from the Monetary Policy Committee’s last report, insisting that bank policy would remain ‘restrictive’ and that there was ‘an awful lot still to do’ to tackle inflation. Market expectation is for the bank rate, currently at 5.25 per cent, to peak at around 5.5 per cent. This is down from an expected high of around 6 per cent just months ago.

Bailey’s comments emphasised that these decisions remain far from certain, as future rate votes are ‘going to go on being tight ones’ (he was referencing the last vote, which came in at 5-4 to hold rates). He did, however, note the ‘subdued outlook’ for the economy. The Bank is not predicting a recession (as Ross Clark points out on Coffee House, the UK is now safe from meeting the technical definition of recession this year), but the consensus among major forecasters remains that growth prospects for the next few years remain stagnant.

Hunt has also been speaking in Marrakesh this morning, talking about what those higher rates have done to the public finances. Hunt, like Bailey, stuck to the script that we’ve heard before. The Chancellor insisted that now was not the time to talk about tax cuts, not least because rising rates will add up to an additional £30 billion to the government’s debt servicing costs in the Autumn Statement. The prospect of energy costs rising once again – and driving inflation back up – will also be weighing heavily on the Chancellor’s mind, as conflict in the Middle East looks set to escalate. The permacrisis continues.

This was originally published in Kate’s weekly Economics newsletter. Sign up here.