You’d struggle to describe the start of 2023 as anything like ‘good economic times’. But according to the OECD’s economic outlook interim report, it’s better than what’s to come. The report, published this morning, expects rising rates around the world to take their toll on economic growth. Global growth has been downgraded for next year – from 2.9 per cent in 2024 to 2.7 per cent – which is lower than the 3 per cent growth expected this year.

The report notes that a ‘stronger-than-expected’ start to the year makes it all but impossible for growth to keep pace: the fall in energy prices coupled with China’s comeback post-pandemic gave global growth rates their boost. But despite economies proving resilient to rate hikes, there is growing evidence that they are now being felt. This, combined with ‘weaker-than-expected recovery in China’ over the next year has led the OECD to downgrade their global expectations for economic growth.

The worst news lands on Germany, which has now become the outlier amongst developed countries, having fallen into recession earlier this year. It is now the only major economy predicted to contract this year – by 0.2 per cent – with an expected recovery next year of 0.9 per cent growth.

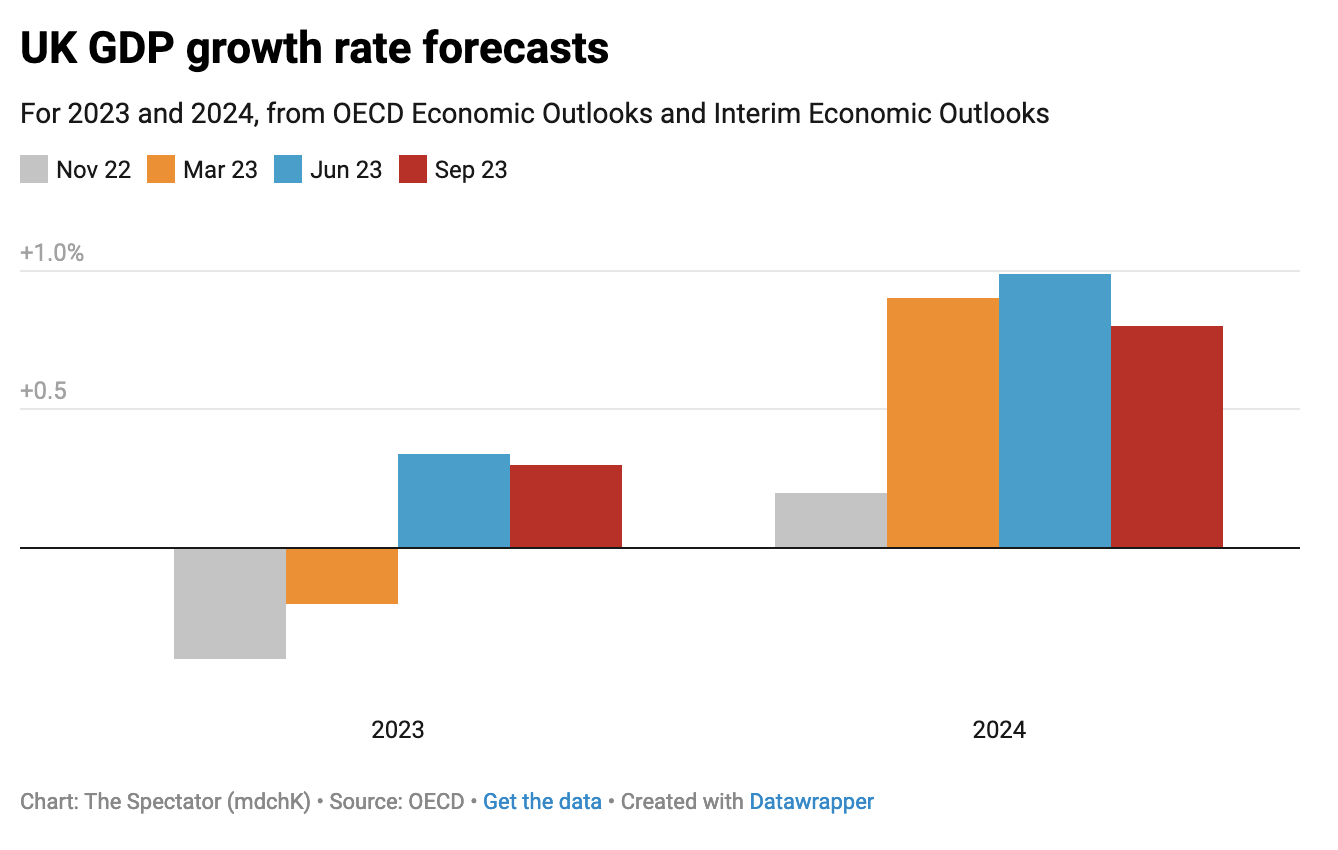

By comparison, the UK looks to be in a better position – but not drastically so. The OECD still predicts 0.3 per cent growth in the UK this year, but it has downgraded its forecast for 2024 from its report in June: from 1 per cent growth down to 0.8 per cent growth.

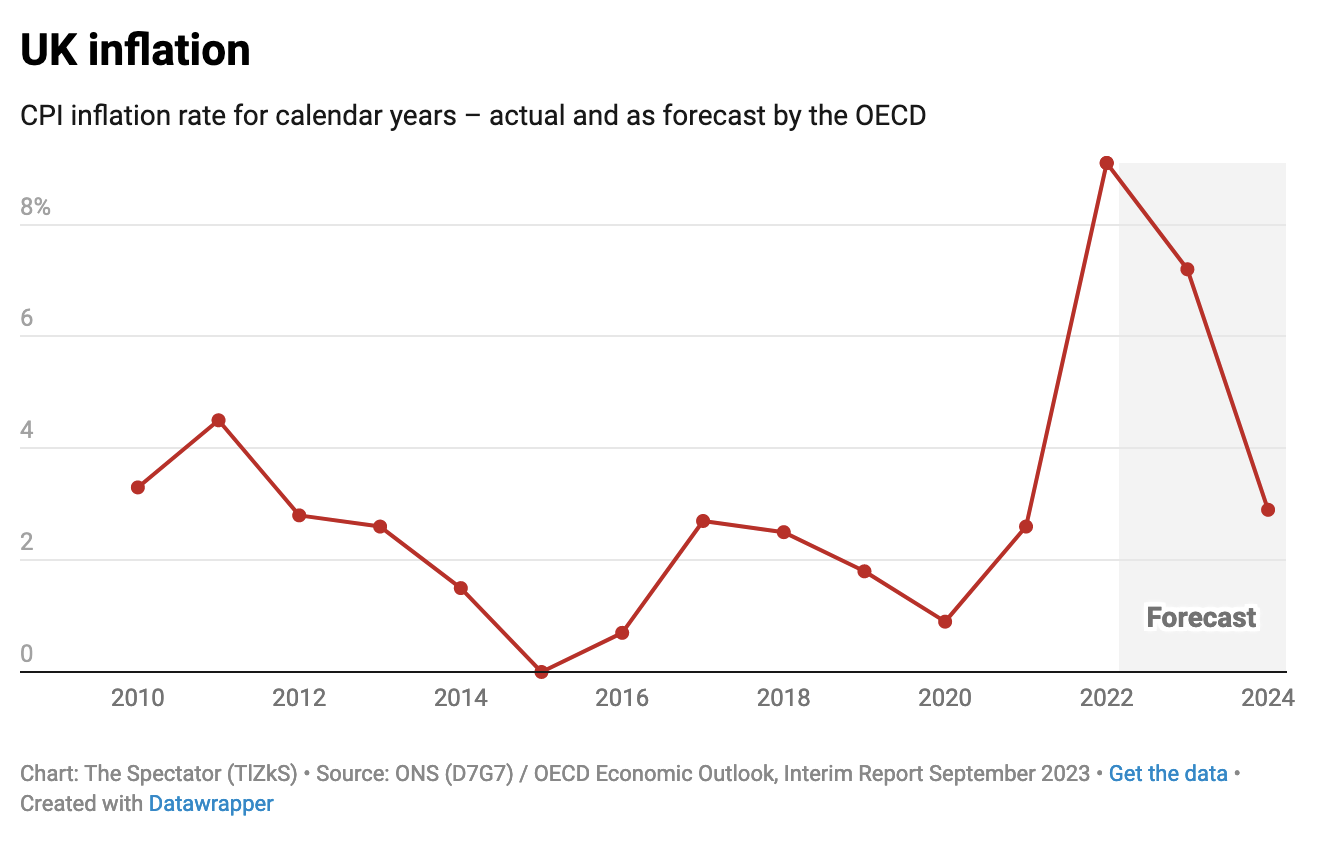

More worrying, however, is that the UK is projected to have the highest inflation of any G7 country this year – at a rate of 7.2 per cent – as well as the highest core inflation (which excludes food and energy prices) at 6.3 per cent. This is expected to fall substantially next year to 2.9 per cent, closer to the predicted average in 2024. The report also cites uncertainty in the UK housing market, as well as the growing effect of interest rate hikes as two reasons it expects some economic slowdown in the second half of the year.

Today’s news once again confirms just how difficult it is going to be for the government to make good on its pledges to get the economy growing and to halve inflation by the end of the year. The first looks set to be met on a technicality; the latter has been looking back on track over the past few months, but will be very difficult to meet so long as core inflation remains so high. Moreover, the chancellor has been laying the groundwork for tomorrow’s inflation update for August to show a temporary rise in the headline rate. This will have to fall again quickly for plans to halve inflation to remain on track.

Of course these are predictions, which not only fluctuate but can often be wide off the mark. Already we’ve seen upgrades for the UK compared to last autumn, when, in November, the economic outlook predicted a 0.4 per cent contraction for the UK this year and only 0.2 per cent growth next year.

The OECD’s estimates today are notably better – though still far off meaningful growth. They mirror what other economic indicators suggest: that between stubborn inflation, a tighter labour market and a stagnant economy, the UK economy’s current trajectory is to stay on the right side of a recession, but only just.