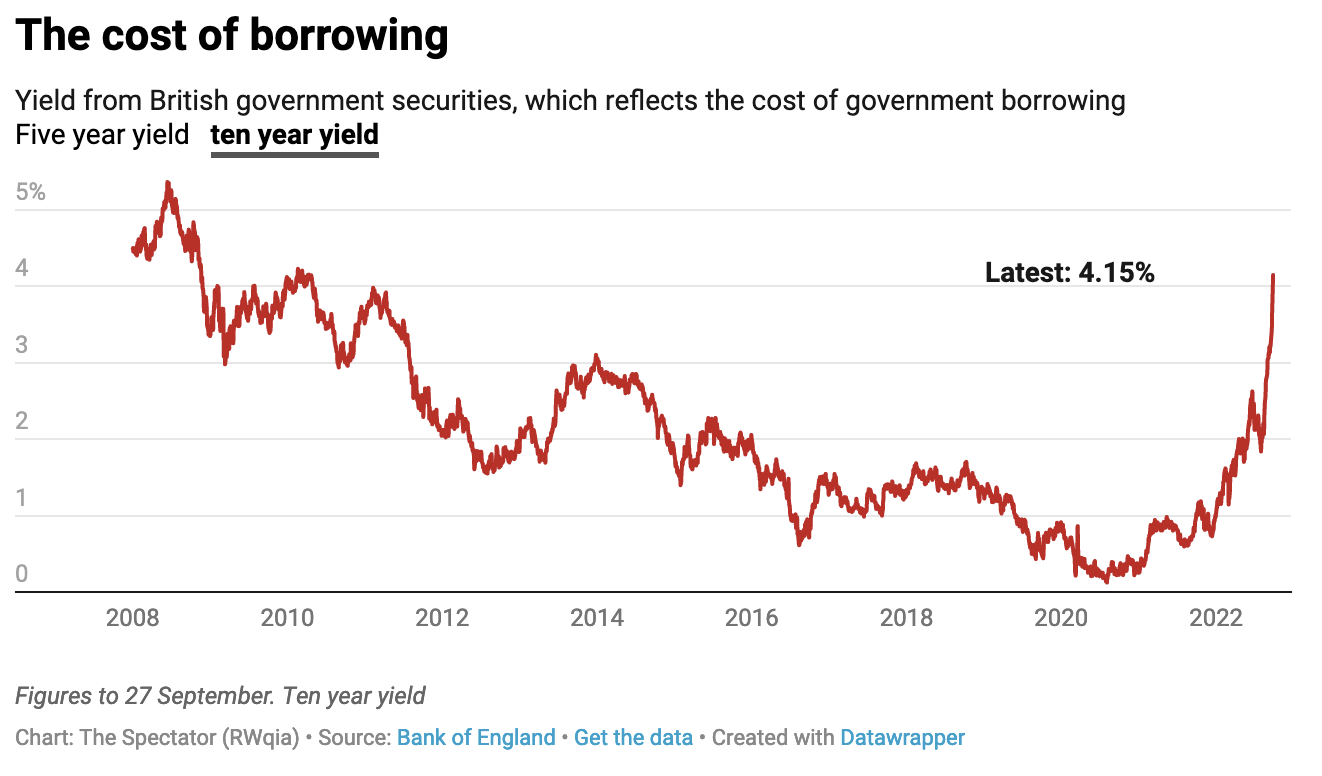

It has dawned on the government that last week’s mini-Budget might have been a bit too one-sided: £70 billion worth of extra borrowing and not a single mention of spending cuts or efficiency gains has seen borrowing costs spike (up by 0.3 per cent just today).

As James Forsyth reports on Coffee House, this afternoon’s announcement that a ‘medium term fiscal plan’ will be announced next month is an attempt by the Treasury to reassure markets – and convince them that fiscal responsibility has not totally disappeared from this government’s agenda. Emphasis is being placed on previous promises to make sure debt falls as a percentage of GDP in the coming years.

But what about the other side of the coin? The Bank of England should (in theory) have a lot of power to settle market concerns by indicating its thinking on interest rates. It also issued a statement this afternoon, stating in no uncertain terms that it ‘will not hesitate to change interest rates as necessary to return inflation to the 2 per cent target sustainably in the medium term, in line with its remit.’

A clear, confident statement. But will markets take it seriously? For months now, the Bank’s Governor Andrew Bailey, alongside the Monetary Policy Committee, has been playing catch-up to curb inflation, after having insisted for months (watching prices rise) that inflation was just ‘transitory.’ Bailey was doubling down on this narrative even when inflation was twice the Bank’s target. His excuses for not seeing it coming were methodically exposed during a Treasury Select Committee back in the spring, further undermining confidence in the governor’s ability to get inflation under control.

Has the Bank redeemed itself enough that today’s statement will have a meaningful impact on the gilt market? The MPC’s more cautious approach to rate rises (compared to the Federal Reserve) already has many doubting that the Bank can command reassurance to the extent it needs to. Capital Economics suggested this morning that we’re at the stage in the cycle where ‘psychology takes over’ and rather than believe the Bank, markets might test the Bank instead.

So the Bank’s intervention may have been necessary – but it may not prove sufficient. You can follow the movement of the pound and the gilt markets live over on The Spectator’s data hub.