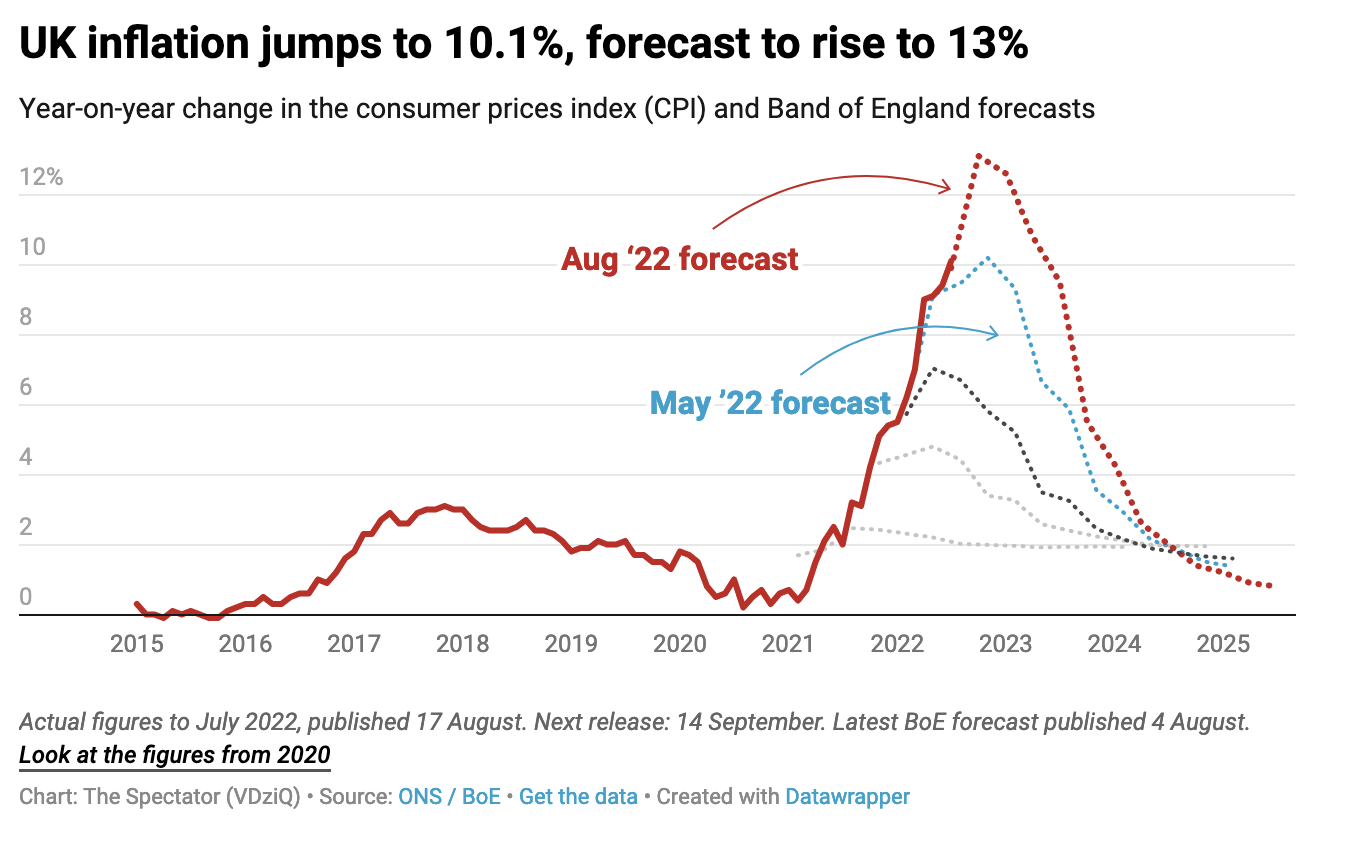

Long gone are the days when politicians and experts dared to claim inflation was simply ‘transitory’. Now it’s hang-on-to-your-hats as prices spiral faster than anyone predicted. This morning the Office for National Statistics reveals that headline CPI inflation hit 10.1 per cent on the year in July. This double-digit figure takes inflation to a 40-year high, outpacing consensus yet again, which was 9.8 per cent.

That figure means all those horrors that have been discussed for months have become more immediate: the instability that comes with spiralling prices, the risk of stagflation, increasing fears of recession as consumers grow more cautious, not to mention the very real fear that people will struggle to afford basic necessities. But two problems stand out this morning as inflation hits double-digits.

First, concerns are rising that the Bank of England has, yet again, been too optimistic about when and at what figure inflation might peak. This has been a trend throughout the inflation crisis: the BoE’s forecasts have only been revised upwards so far, as it becomes clear that prices go beyond their expectations. This time last year, most of Whitehall was still in complete denial about the price hikes that were about to shake the UK. Since then it’s been a game of catch-up and a fairly unsuccessful one at that. Capital Economics predicts that today’s 10.1 per cent will put pressure on the Bank to go for another 0.5 percentage point interest rate rise in September, as the need to curb these price hikes intensifies. Market expectations (tracked on The Spectator data hub) are currently that rates will peak around 3.25 per cent, but staying above 2 per cent for the foreseeable future.

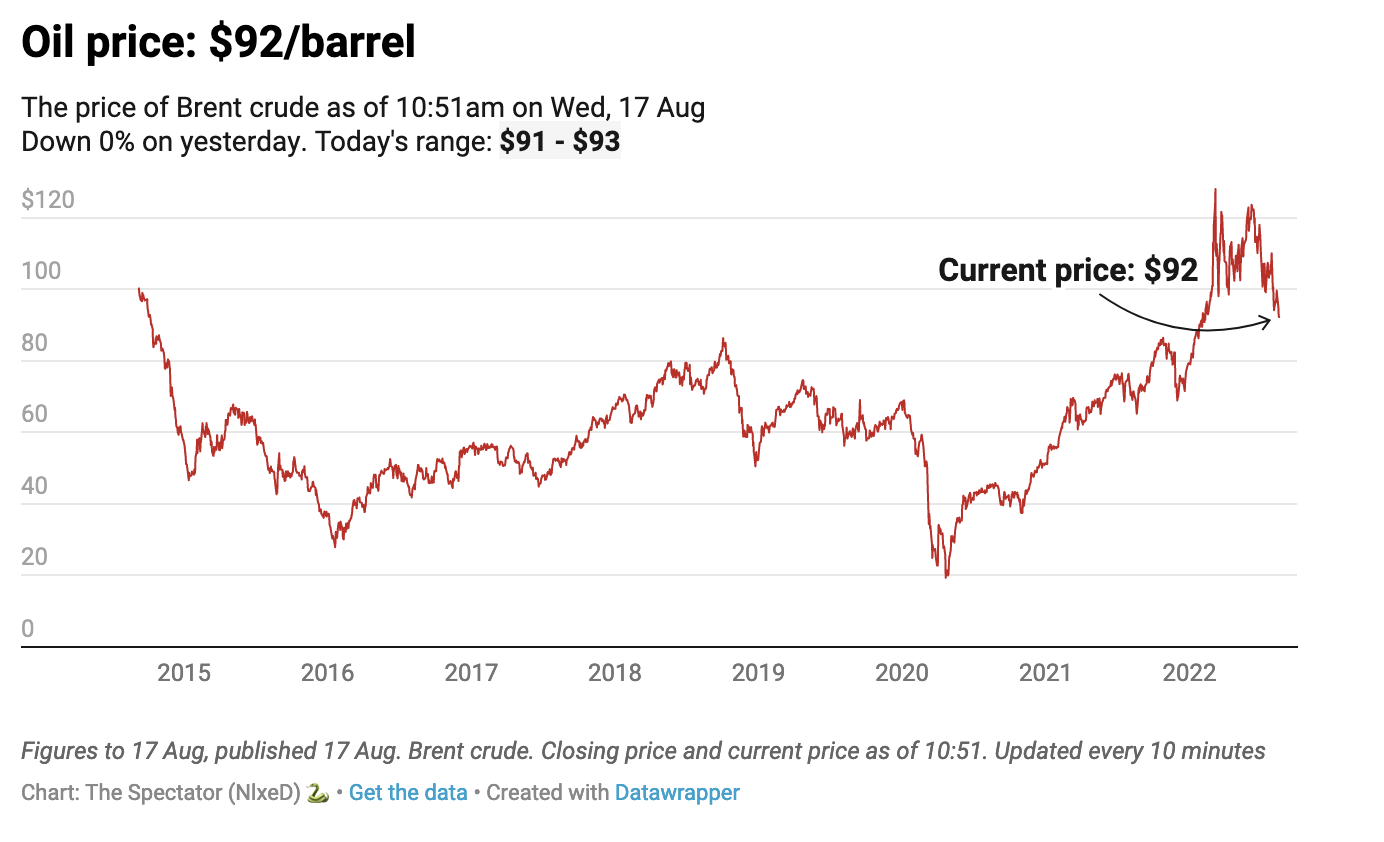

The other major red flag in this morning’s update is the source of these price hikes. Fuel prices rose by 2.9 per cent from June to July, taking prices to ‘highest rate since before the start of the constructed historical series in January 1989.’ But the rate at which weekly forecourt prices increased started slowing in July – a positive early sign that the downward trajectory of oil prices may soon benefit consumers.

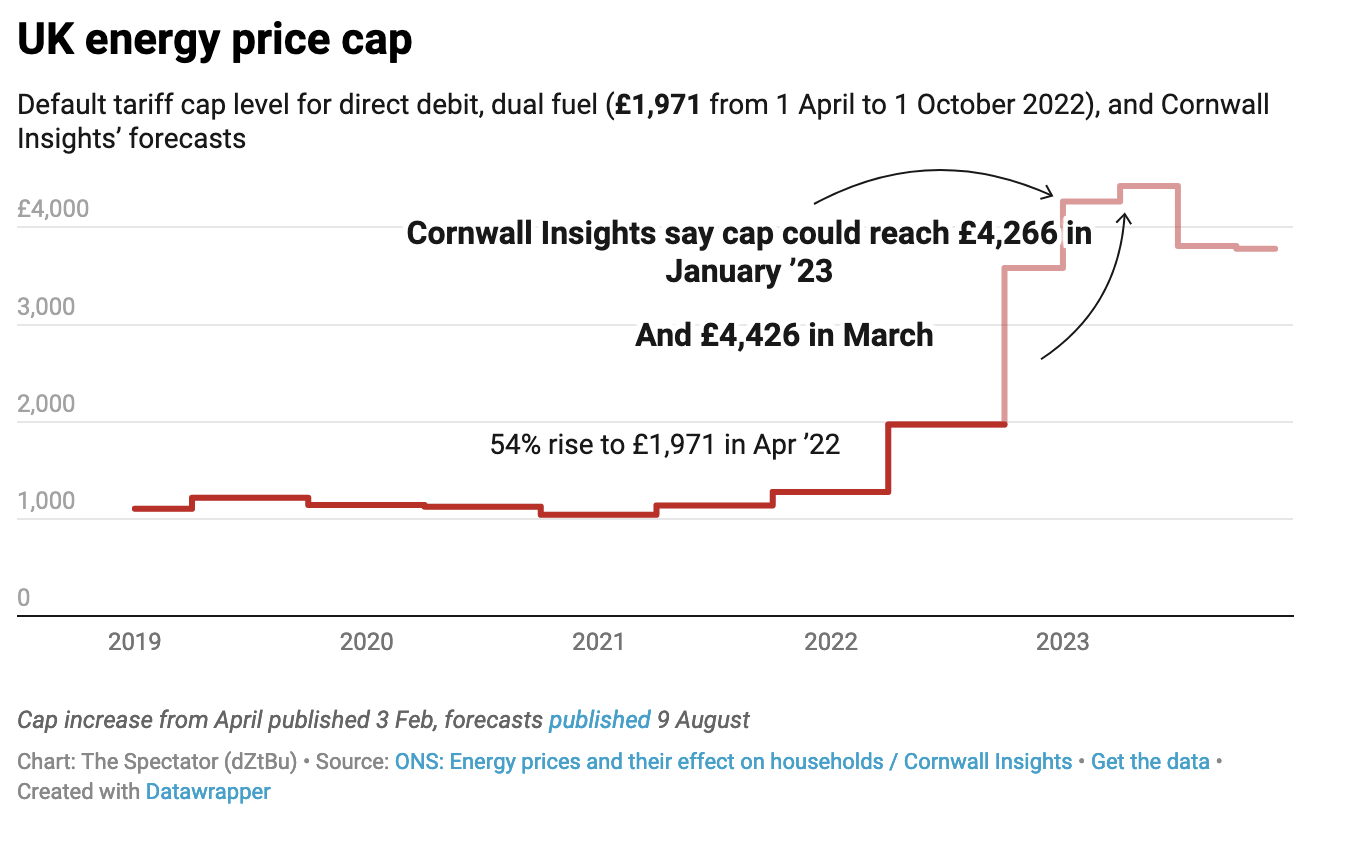

But it was not energy prices that were running away in this monthly update. It was food, which rose to 12.6 per cent, from 9.8 per cent. The services index also hit a 30-year high, rising by 5.7 per cent on the year, up from 5.2 per cent last month. All this challenges the (again) optimistic and popular theory that its energy prices alone that are causing inflation to soar. When the energy price cap rises again in October, estimated to take average household energy bills over £3,000 a year, these financial burdens will be made worse by the rising costs of food and domestic services.

No doubt Liz Truss and Rishi Sunak will be under pressure today to be clearer about what they plan to do to help households deal with rising costs. But it will be an especially difficult day for the Bank of England, which got its inflation forecasts so wrong last year and failed to tackle price hikes when it was much more manageable to do so. As always, it’s consumers who will suffer most for these mistakes.